Top Reasons for a Weak Start to 2025 in the Markets

In this video I’m going to quickly cover why the first 2 weeks have started off on a down note for most equity markets. I am also going to cover why it is not yet overly worrisome from a historical perspective when the economy is in the 2nd or third year of a “soft landing” after experiencing 1-2 years of significant gains.

Before I get into this week’s topic, I hope that you join us on January 23rd, at 630 PM central via YouTube as OHFG is hosting our first half market outlook and will be livestreaming a good deal of the evening. I’ll drop a link for registration in the description below and please feel free to submit any questions you might have that you would like the team to touch on in the comment section of this week’s video.

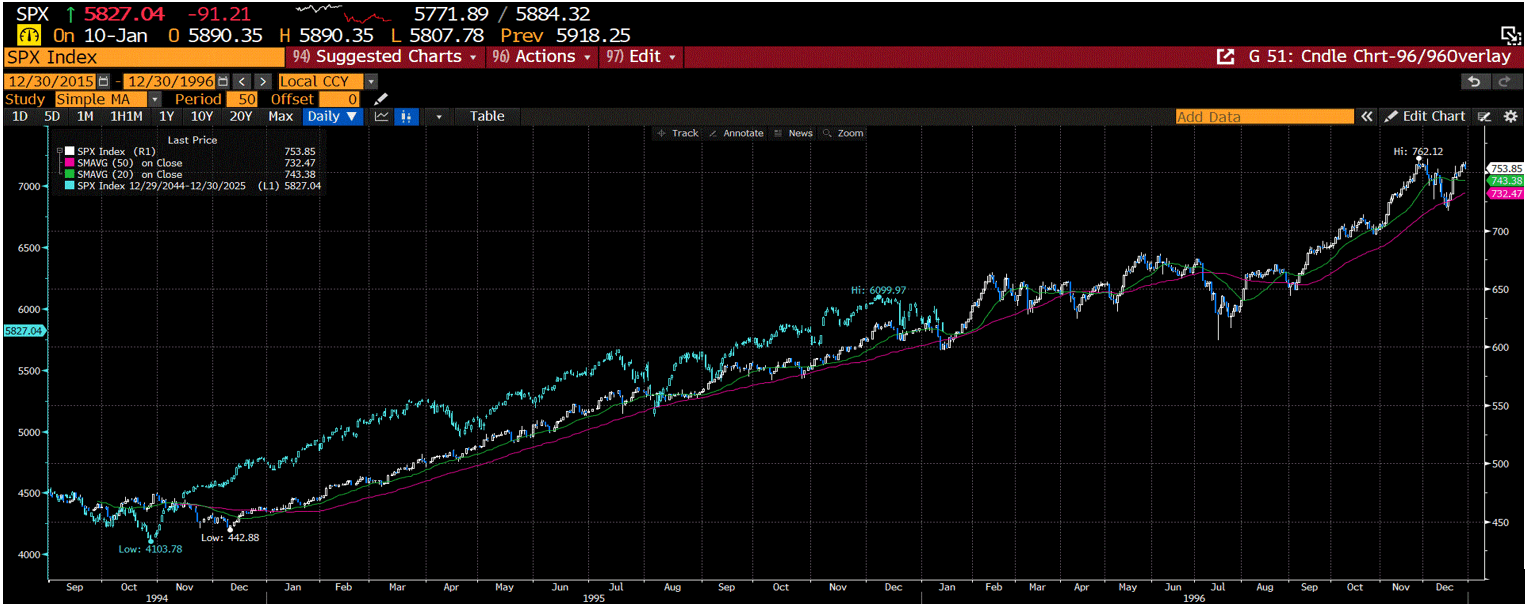

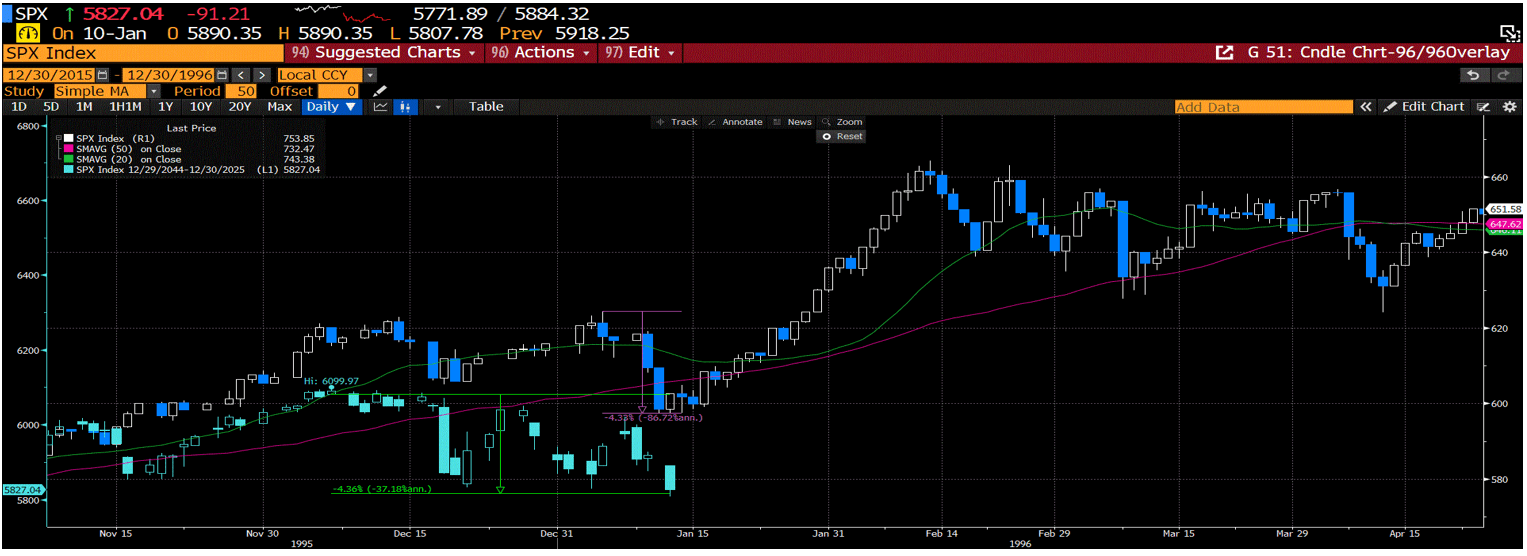

The US stock markets represented by the SP500 have started out 2025 on a down note. After gaining over +23% in 2024 in price and about +25% in total return including dividends, the S&P 500 is down about -1% year to date, However investors, since reaching its absolute intraday peak near 6100 on Friday, December 6th, my 59th Birthday, the S&P 500 has declined about -4.36% from its closing high that day to this writing.

And with that, many of the usual suspects have come out of the woodwork with their annual “crash cart” calls. Whether they will finally be proven correct after 10-15 years of the same call, I don’t know. What I do know, is our next has discussed this kind of possible downward action to start 2025 since early December. Why? Because soft landing economic scenarios do NOT guarantee constant upward trending stock markets with low volatility. How do we know this? History. As we have discussed for the better part of 15 months, the last time the Fed was able to commandeer a true soft landing for the economy and stocks was 1994-97 under Alan Greenspan. Greenspan raised rates in 94, cut rates by 75 basis points in the 2h95, and subsequently paused rate moves for almost all of 1996.

To jog investors memory, here’s the same overlay we’ve presented for quite some time overlay the last soft-landing with our current one. The one that started in late 2023, ran throughout 2024 and currently continues with the help of the Fed previously cutting the Fed Funds rate by 100 bps in the 2h24, pre-presidential election.

What happened during the previous Greenspan induced soft-landing?

After experiencing a +30% up move in 1995, the S&P 500 came out of the gate in 1996 and did what? Yeap, you guessed it, it dropped near the exact same % high to low as it has the last 4-6 weeks, -4.33% by my calculation with the Bberg data.

While history doesn’t often repeat exactly, it does often rhyme. Why? Because humans are creatures of habits. And I like to say, it’s many of the same people, managing the same money, making the same decisions, getting very similar outcomes.

So, let’s talk about a few of the potential reasons that we’ve come out of the gate weakly in 2025, even if the economy seems on good footing.

First, the supply and demand for equities is out of balance to start the year with more sellers than buyers to start the year putting downward pressure on stocks, particularly last year’s winners. 2 factors on the supply demand side? First, with the market’s strength in 2024, many investors pushed their stock sales and tax events out into early 2025. Why sell late in 2024 and have to pay taxes in the next few months in 2025 when you can wait a couple of weeks and sell stocks in early 2025 and push the cash tax event out into late 2025 or even later. Second on the supply demand side, favoring stocks sales in early 2025 is the pretty high likelihood that while Trump 2.0 will extend the initial Trump tax brackets beyond 2026, it will be harder for the new administration to drop tax rates, both income and cap gains dramatically lower as they did in Trump 1.0. If an investor thinks that Trump winning and current tax bracket extensions is “good enough” vs. a Harris/Biden win and higher tax brackets in 2026 forward, that’s probably a good reason for many rich investors or highly concentrated investors to sell now and take the sure thing.

Finally, on the supply demand front, we are in peak season for the blackout window for corporate stock buybacks. What does that mean? It means that the vast vast majority of companies that have announced stock buybacks CANNOT legally and actively be in the market bidding for their own stocks on down days as we’ve been experiencing year to date. The data I’ve seen says that upwards of 90% of all corporate stock buybacks are on hold this week, near the maximum level in the quarter and near peak for the year. As companies start reporting, like the banks and financial companies in the last few days, their buyback windows open as a wave of additional active buyers. However, remember that most companies must wait 48 hours after they report earnings to get into the market transacting in their own shares. Because of this, you might have heard several traders on TV saying they personally have 2-3 days waiting to trade rules after a bad earnings report if they are interested in buying a stock. What they are saying is they are ok with waiting for the initial selling smoke to clear before establishing a long position buying the stock.

Additional macro-economic reasons for the weak start to 2025 include the recent strong jobs number which pushed longer term interest rates higher on the back of 1- fear of a slow Fed in 2025 and 2- stronger wage markets and higher inflation. Both valid reasons for traders to sell short term and stocks to drop lower as higher long-term rates does marginally hurt consumers looking to borrow and spend, as well as hurting more highly leveraged companies. Higher trending rates also has a downward affect on P/E multiples for equities as 1-treasuries can become more attractive than the uncertainty of equity investing, and 2- you have to discount future cash flow of your investments by a higher interest rate, which mathematically lowers the present value you are willing to pay.

A stronger dollar in late 2024 and 2025 is also weighing on investor sentiment. Why would this happen? Don’t we all want a stronger dollar if there is truly US exceptionalism? Isn’t a stronger dollar good for America? The answer is yes and no. Yes, a stronger dollar is good for America and Americans. It’s good for US consumers and bad for foreign consumers as its inflationary for them and positive for USA consumers if you’re buying goods produced elsewhere or traveling abroad. However, a stronger dollar is a definite headwind for the S&P 500 overall as much of the S&P 500 is comprised of USA companies operating in a multinational arena. The likes of JNJ, KO PEP, CAT, and even technology companies based here sell anywhere from 25-50% of their goods and services outside the states. For these multinational companies, a stronger dollar is a headwind to both revenue and earnings growth as it depresses both numbers when their foreign sales are translated and converted back into USA dollars.

Look no further than the recent reports from both Oracle and Adobe in the software technology world warning of $100; s of millions of dollars in headwinds to their recent 4q24 and future 1h25 revenue and earnings due to the strong US dollar in 2h24.

Expecting more of the same from most large cap multinational S&P500 companies, aggregate earnings estimate for 4q24 and 1h25 have been coming down over the last 4-8 weeks. While this is a very normal occurrence at this time of the year, it does serve as a headwind to equities, particularly as longer-term interest rates have risen.

An additional headwind to global growth, economic demand, and earnings growth in 2025 continues to be China. Chinas domestic consumption economy is pretty bad right now and the stimulation programs that have been announced to date don’t seem to be working yet. China is still one of the top economies and largest markets in the world for products and services, and whether you agree with their political policies or not, global stock markets and investors would be best served if they put in place some programs to stimulate consumption by their population in 2025/26.

Maybe they are waiting to see President Trumps hand and gameplan, I don’t know, but they did stimulate in 2017, and their markets were one of the best performing asset classes that year even with the Trump Tariffs and geopolitical tensions. Equity markets would like a adrenaline boost from China in 2025, not more of the meandering lower that’s been going on now for a few years.

Investors, those are a few of the reasons we see why 2025 has gotten off to a bit of a rocky start in the equity markets even with the higher confidence of Trump 2.0 with lower taxes, lower regulation and a soft-landing economy. As we can see by the soft landing under Greenspan, historically speaking, it isn’t unprecedented for mid years in a soft-landing environment to begin this way, we’ve reference 1995-97 many times the past year and 2025 is starting off a lot like 1996 did. Weak with higher volatility out of the gate as we mentioned it could back in December. However, investors this does not mean that the bull market in US equities is over or that 2025 cannot be the third year in a row of healthy investor gains in US stocks.

We hope that you join us next week on January 23rd, at 630 PM central via YouTube as OHFG we are hosting our first half market outlook, and we will be livestreaming a good deal of the evenings events for others to see. Theres a link for registration in the description below and once again please feel free to submit any questions you might have that you would like the team to touch on in the comment section of this week’s video. Until next week, or we meet again, have a blessed weekend and my prayers go out to anyone affected by the fires in the West.

Do you need a retirement plan that goes beyond allocating funds to truly fit your needs? We can help you create a retirement life plan customized for your retirement vision and legacy. Call us at 877-896-0040 @@@or fill out this form for a free consultation: https://click2retire.com/Connect

Chris Perras

CFA®, CLU®, ChFC®

Chief Investment Officer, Financial Advisor

Chris is a seasoned investment professional with over 25 years of experience working with some of the most successful money management firms in the world. Chris has made it a point in his career to adapt as the market landscape changes, seeking to utilize the appropriate investment strategy for a given market environment. His transition from managing billions of dollars at the institutional level to helping individuals and families retire is guided by a desire to see first-hand the impact he is making in the lives of clients at Oak Harvest.

Click to subscribe: