2025: First Half Market Outlook

First off, Happy New Year and welcome to 2025 as this is the first stock talk of the new year. Over the last 8 weeks, our investment team has answered a myriad of questions into and out of the election in November. We laid out multiple scenarios to how 2025 could play out in the financial markets and our economy. And those following along closely should already understand our outlook for the first half of 2025, but this is a brief video to wrap our first half outlook up with a neat bow.

Our team has been discussing since well before the election why this bull market could remain alive in 2025 regardless of who was elected. Without preempting all of our presentation for our 2025 market outlook summit that Oak Harvest hosts for clients and prospects, that will take place on January — at the Hotel Zaza here in Houston, we will drop some info in todays video.

We believe the first half 2025 will continue 2024s economic soft landing that we have been experiencing in the US, however the first half of 2025 may usher in a bit more volatility than 1h2024 did while the stock market stays on its generally upward trajectory. We covered 3 potential paths last week in our video, The Great, The Good, and The Ugly. We will drop a link to last week’s video below. Our most likely path for 2025? The Good.

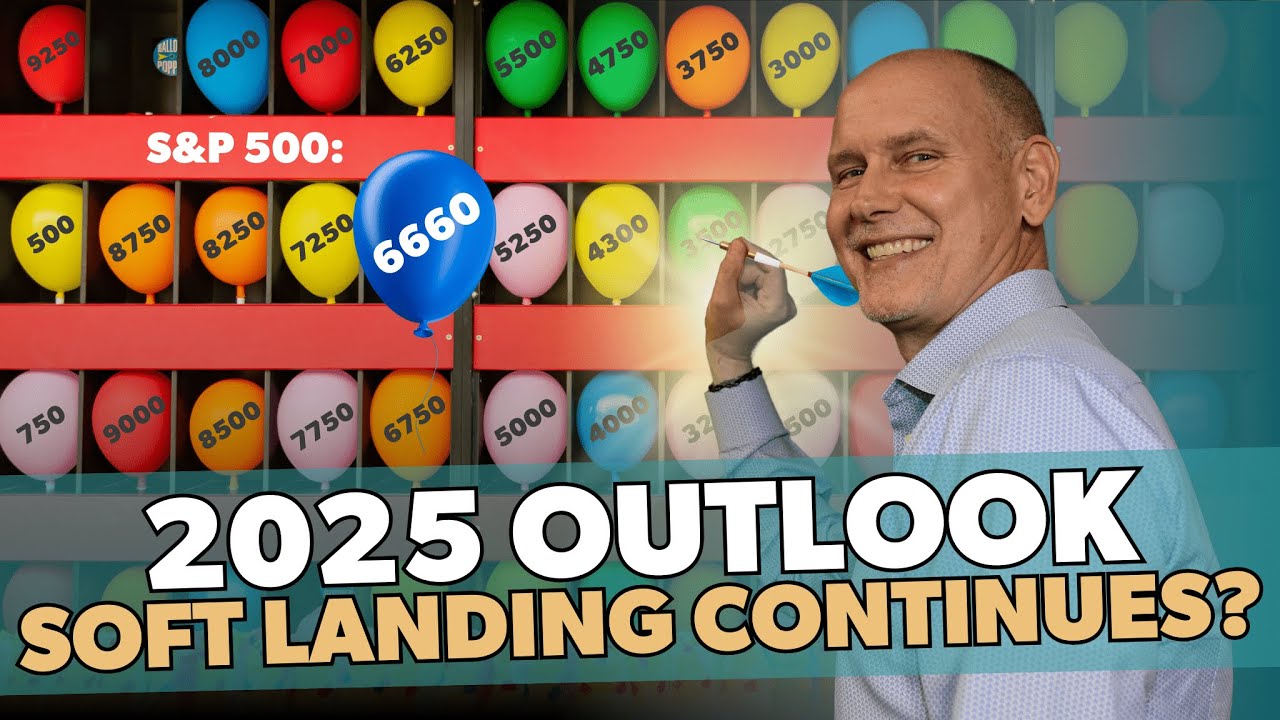

If one wants a historic “model” to the “Good path”, the Greenspan led 1995-97 soft landing seems to be the path we are mirroring. Yes, it’s rare, and very few investment professionals outside of our OHFG investment team were anticipating a soft landing for 2024 back in the 4th quarter of 2023. However, here we sit, near 6000 on the S&P500. Above even our optimistic 5800 projection back in late 4th quarter 2024, and already at our optimistic inaugural ball late January mark we referenced over 9 months ago.

And after almost 2000 S&P500 points, and 14 months of a rally, most of the sell side Wall Street has thrown in the bearish towel and played catchup to out overlooks for the market. In fact, now many previously bearish and wrong strategists are now forecasting higher S&P500 targets than our team.

Our team had been discussing since well before the election why this bull could remain alive in 2025 regardless of who was elected. Without preempting all of our 2025 market outlook summit presentation that will take place on January — at the Hotel Zaza here in Houston, here is some data on our outlook for the “Good”.

What’s the Good in our work? It about 6660 on the S&P 500 during 2025, which would be about +12-13% from our current 5900+ on cash S&P500. The good is a continued soft landing in the economy. Higher earnings, flattish long bond yields, and a peaking to stable dollar. The “Good” scenario anticipates a range of normal volatility that we’ve experienced over the last 10-15 years leaving out the Covid collapse. Unfortunately for investors, we currently do not see a return to the low to no volatility markets of 2017, Trump 1.0. But even without a collapse in volatility like 2017, the overall S&P500 can have a good year in 2025.

The best historical precedent for the Good outcome in 2025 is probably 1994-1997 with 1995 being what we just experienced this year in 2024. We actually discussed this 1995/96 period early in 2024 as many doomers were calling for crashes and economic calamity. Why did we reference this one? Well, this is one of the few times in stock market history that the Fed Reserve, back then under Alan Greenspan, was actually able to engineer just an economic slowdown without causing a dramatic economic downturn, recession or financial collapse in markets.

Back then, in the summer of 1995 and 4th quarter, Greenspan and the Fed cut interest rates to 5.25% from 6% over about 6 months, cooling the economy without tanking it. Investors, does this sound familiar? As much hysteria as there is in current financial press about rising long term treasury yields, even back then US Treasury yields ended higher in the 12-month period following the first FOMC interest rate cut. Why? Because the economy was Ok with the slowed pace of interest rate cuts and saw an extended economic cycle.

Back then, overall bond total returns trailed cash returns and stock returns. What’s this mean? It means you wanted to stay in shorter term maturity treasuries in your fixed income holdings, for the soft landing in the economy. You wanted to own cash and 2-5 year treasuries not 10-30 year maturity fixed income instruments.

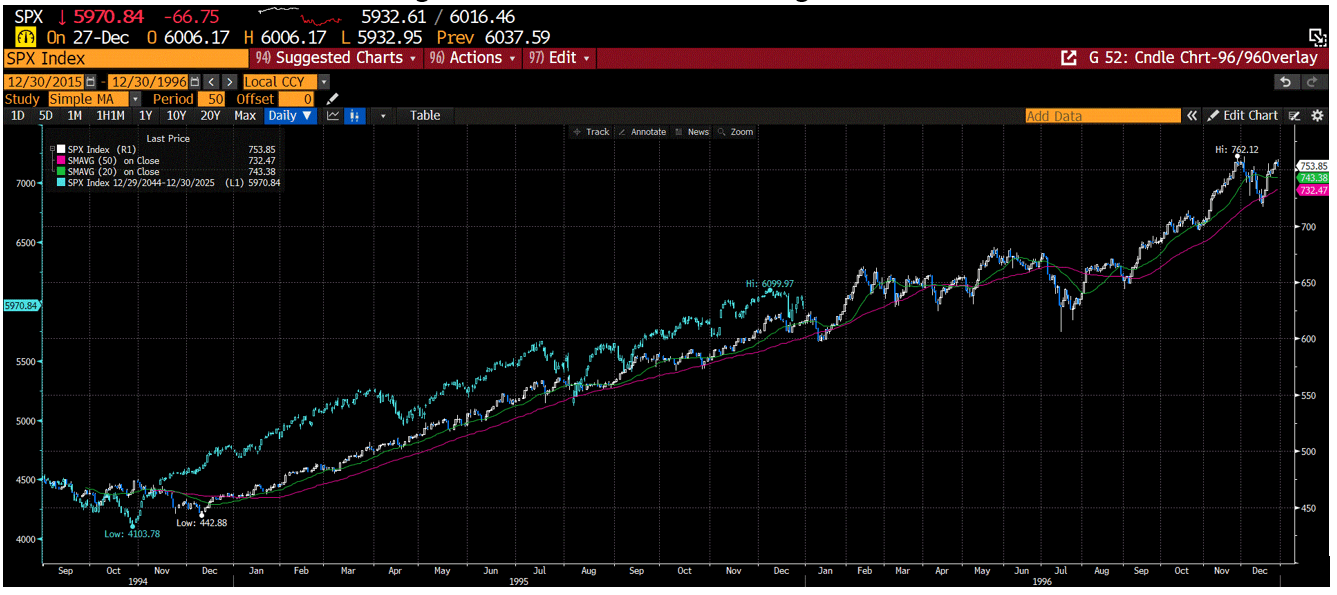

As for stocks and the S&P500? Here is the chart of the S&P500 from 1995-95 overlaid with 2024/2025. Soft landing in stocks vs. soft-landing in 2024.

1996 saw a continued soft landing for the economy, but market volatility ratchetted higher throughout the 1h96. Right now, the forward volatility markets suggest that this is a decent likelihood again in the first half of 2025. The bull would run on in the first half of 2025 and end the year much higher, but the bulls might be subject to more volatility month to month in the 1h25 than last year in 2024.

Just to remind those who weren’t investing in 95/96. The S&P 500 started the year 1996 on a bit of a sour note, selling off for the first few weeks about -3.5%, but then found its footing into earnings and rallied strongly to put the index up about +6.5-7.5% into April. However, looking at the month to month returns of 1996, post mid-February 1996, the S&P 500 did nothing “net” for almost 6 months, trading in a wide range through late July. During the summer of 1996 the S&P500 rose to about +10% YTD but sold off -9.5-10% in a summer swoon before regaining its footing and ending 1996 on a very very strong note with the S&P500 up about +20% on the year.

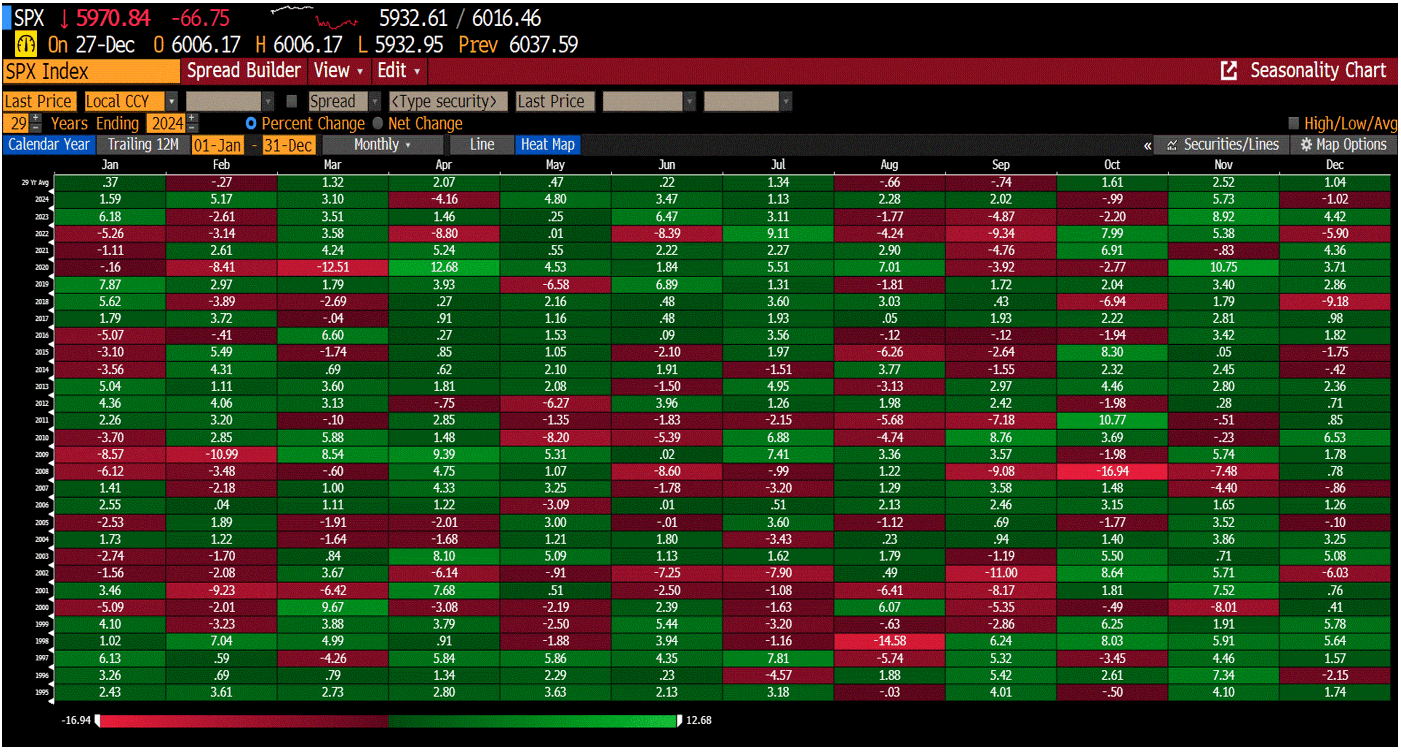

For all you stock market historians and data junkies with good eyesight, here is a table with the monthly returns of the S&P500 dating back to 1995.

You can follow along throughout 2025 and see if we are following any similar pattern throughout the year.

As for a list of those things that our team feels will be most important to extending this stock bull market for another year. And investors, these are listed in order of importance.

- S&P 500 earnings growth and growth rates continue to be strong. Stocks follow earnings and marginal cash returns over periods measured in years.

- Interest rates, whether nominal, real interest rates, and inflation expectations. Lower trending rates at the long end of the Treasury curves, which are generally market based, are better for equities than higher trending rates. Why? Because the terminal value for equities is based on discounting their free cash flow over years back to present value, and when you make that calculation with a lower interest rate, your terminal value goes up. When that calculation is done with a higher rate, your present value for equities goes down.

- Keep a watchful eye on the US dollar. I think this is the key chart for 2025. There is no de-dollarization of note in global markets. Currencies are a relative game. No one wants to own communist or socialist currencies over capitalist oriented country currencies. The S&P 500 and its returns would be best served by a gradually weaker dollar in 2025, much the same way it weakened in 2017 under Trump 1.0. A weaker US dollar would broadly help earnings of large cap multinational companies, which lagged in 2024.

- Goldilocks for equities is stable to lower longer-term interest rates, lower trending inflation and stable to lower real rates. That’s what happened in general in 1996 and in 2017.

- China truly stimulating their economy would be a HUGE deal for global stock markets. No band-aid announcements like the last 2 years, but real monetary stimulation that gets consumers spending. Let’s be frank. China’s domestic economy is a disaster currently. There is no chance they are growing at the rates their government says. It is one of largest markets in the world for products and services and global stock markets and investors would be best served if they actually put in place some programs to stimulate consumption by their population in 2025/26. Whether they are waiting to see President Trumps hand and gameplan, I don’t know, but they did stimulate in 2017 and their markets were one of the best performing asset classes that year even with the Trump Tariffs and geopolitical tensions.

- Tax rates for both corporations and individuals. Lower corporate tax rates for businesses means more cash for shareholders and hopefully higher ending investment returns as well. Lower to stable taxes for individuals, means more cash in your wallet to spend as consumers or invest as investors. It also takes the pressure off many investors who need to sell stocks now or in 2025 to beat the rush to higher tax rates in 2026.

- Fiscal restraint. Investors need to remember that whether you liked the Bidenomics IRA economic plan or not, many public companies and their shareholders benefitted from the spending in 2023/24 and it makes those companies comps more difficult to achieve growth in 2025/26 particularly if those programs get cut back in a material way during Trump 2.0. What’s good for the taxpayer and lower deficits on the surface, might not be good for the investor. This is one of my own biggest fears that can lead to slower growth in 2025 and 2026 in the US and lower earnings than many think.

- There is a great deal of discussion, debate, and hysteria in many circles on this subject. Tariffs are taxes. Frankly most politicians don’t know much about real world economics. Tariffs are friction on consumers and manufacturers and friction is bad for investors. Investors hate friction that separates them from their money and desired investment. Tariffs should not affect the service component of the US much leaving consumption. Overall, the necessary goods that we import from possible tariffed countries to survive is relatively low. Additionally, since the initial Trump tariffs were enacted during his first term, most international companies have diversified their manufacturing supply chains away from China. Autos would be hurt due to Mexican production, and some others like electronics, however we are energy independent and now a large exporter of BTU’s.

- Immigration policies. Yes, mass deportation of illegal immigrates would likely initially cause not only and economic slowdown, but also an increase in service inflation. Our team sees a softer policy once implementation begins as a weaker economy is not in the administration’s best interest.

- Geopolitical uncertainties. These get talked about all the time by many economists and strategists on TV and in social media. There is an entire consulting field around this topic, but I rarely if ever hear the most successful longer-term investors talking about this subject. Traders, yes? Long term investors? Warren Buffet? Technology and Venture capital investors? Almost never. Generally, its theorists trying to predict the unpredictable. You hear “black swan” zealots preaching about these risks all the time, and how many rich pessimists do you know?

Investors, S&P500 7000 in late 2025? Is it doable in the next 12-14 months like many strategists now saying? Many strategists who were much too pessimistic and negative about 2023 and 2024 and seem to now want to catch-up? The simple answer is yes. It would be a near EXACT replay of Trump 1.0. Is it “easy”? No of course not. The unforecastable can play out. Maybe it is different this time. For now, the math I follow says 6660 would be a likely topping place in 2025.

Until proven otherwise, my suggestion to you is if you didn’t in late 2024, if you are in or near retirement, give your financial advisor a call in early 2025 and walk through your financial plan and determine if you and your money are taking the right amount of risk given your current and future spending. Walk through your budget and goals with them and determine if with the substantial stock market gains of 2024, you are taking more risk than you need to. If you are years away from retirement, meet with them and discuss if you are perhaps not taking enough risk to meet your longer-term retirement goals. And of course, investors, I suggest you take an hour or two out of your busy new year and tune into our Market outlook that will be livestreamed on January— at — to keep abreast of our investment teams current thoughts and perhaps directly answer and address a few our your lingering economic and investment questions.

And with that, the Oak Harvest team wishes you and your family blessed and a Happy New Year ahead in 2025.

Chris Perras

CFA®, CLU®, ChFC®

Chief Investment Officer, Financial Advisor

Chris is a seasoned investment professional with over 25 years of experience working with some of the most successful money management firms in the world. Chris has made it a point in his career to adapt as the market landscape changes, seeking to utilize the appropriate investment strategy for a given market environment. His transition from managing billions of dollars at the institutional level to helping individuals and families retire is guided by a desire to see first-hand the impact he is making in the lives of clients at Oak Harvest.

Click to subscribe: