2025 Stock Market: We Never Said it Would be Easy

Investors, there are no guarantees in the stock market, and the first two months of 2025 are proving that a lesson to those who just entered the markets the last 2 years and enjoyed +20% returns. It’s been a sloppy, choppy mess which while uncomfortable to those watching day to day or week to week, as we previously warned, 1- is not unusual and 2- likely to be the case for the first couple of quarters of 2025.

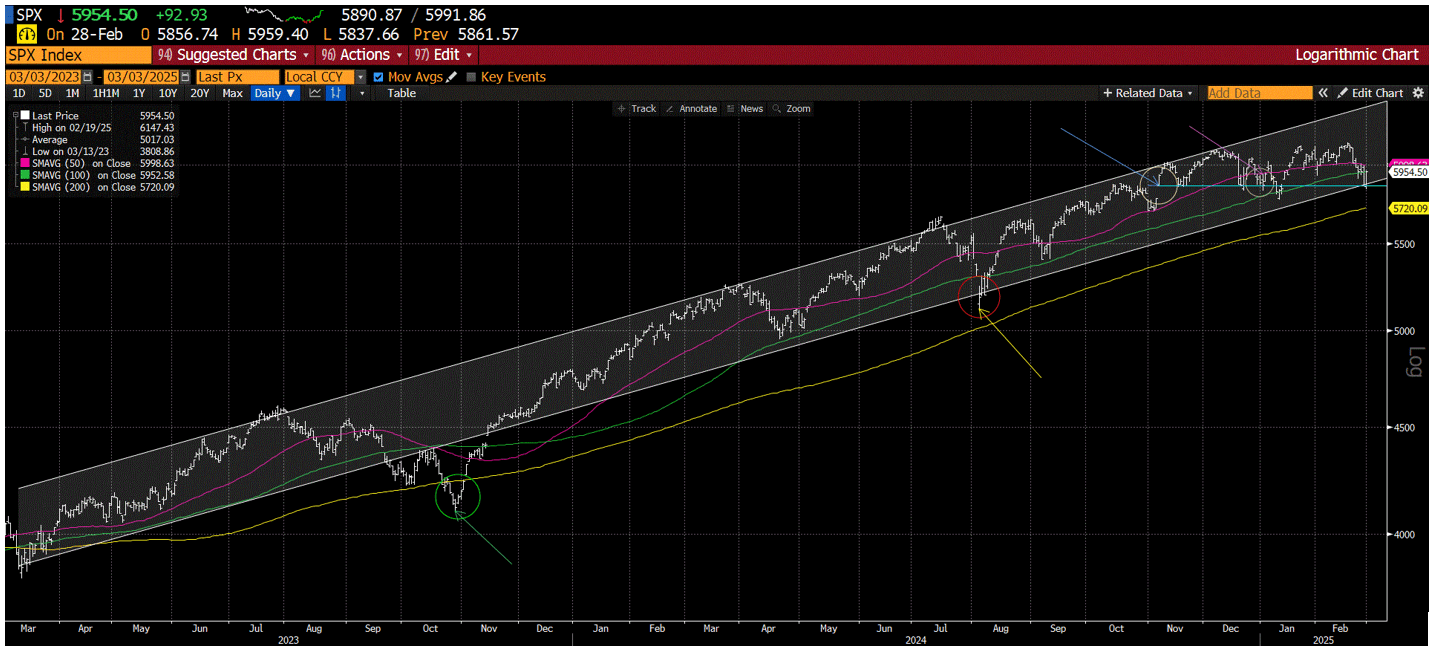

Here is a 2-year chart of the SP500. I’ve drawn the general upward sloping channel we’ve been in for that time period.

On the chart you will see we traded outside this band in October of 2023 for about a month as many were preaching the end of the bull market, recession, Elliot wave Theory Generational tops, or the biggest nonsense I recall at that time, the coming of a replay of the 1987 stock market crash. We felt none of those things were going to happen and were coaching our followers to be buyers of stocks.

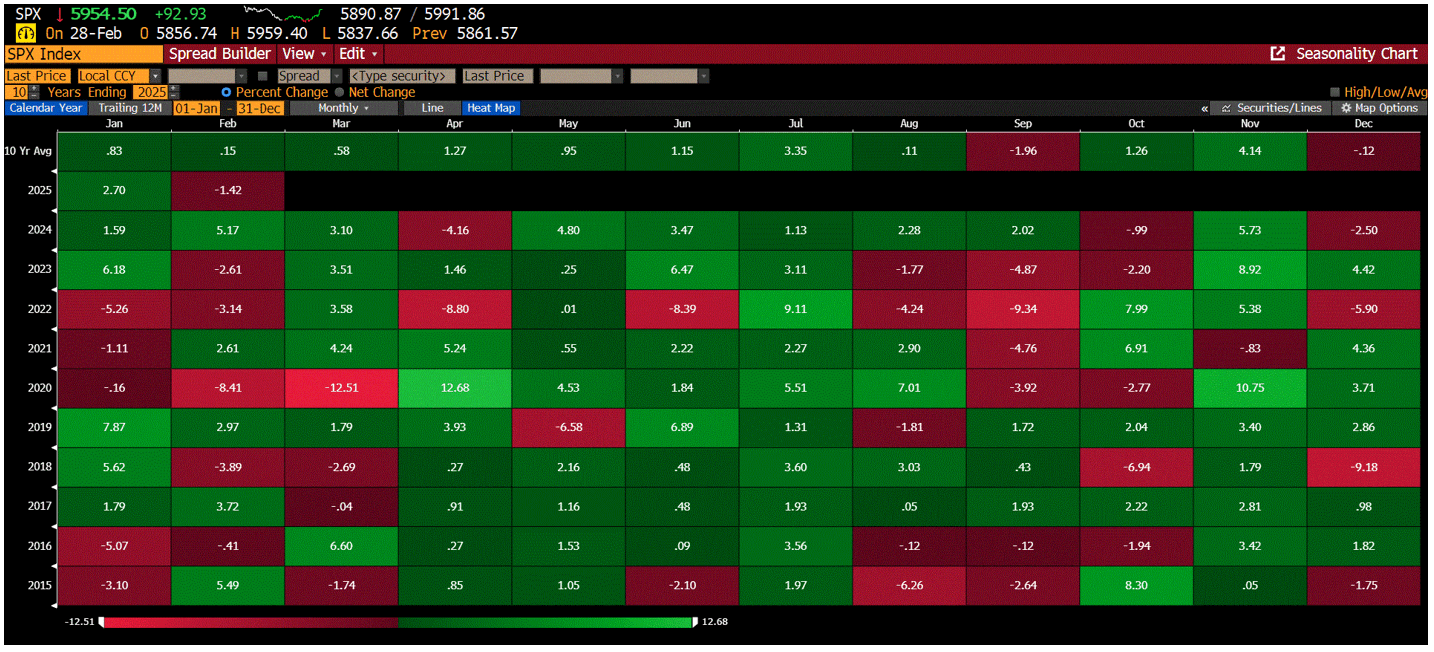

You’ll see the mid-summer pullback in July and August 2024, caused by the unwind of the Yen carry-trade delevering, pretty much on cue for normal summer selloffs. And you will see the gap higher in early November as Donald Trump won a landslide Presidential victory. Which brings us to the present, the first two months of 2025. January went up 2.7% and February down -1.42%. Here’s the SP500 seasonality matrix for the last 10 years from Bloomberg.

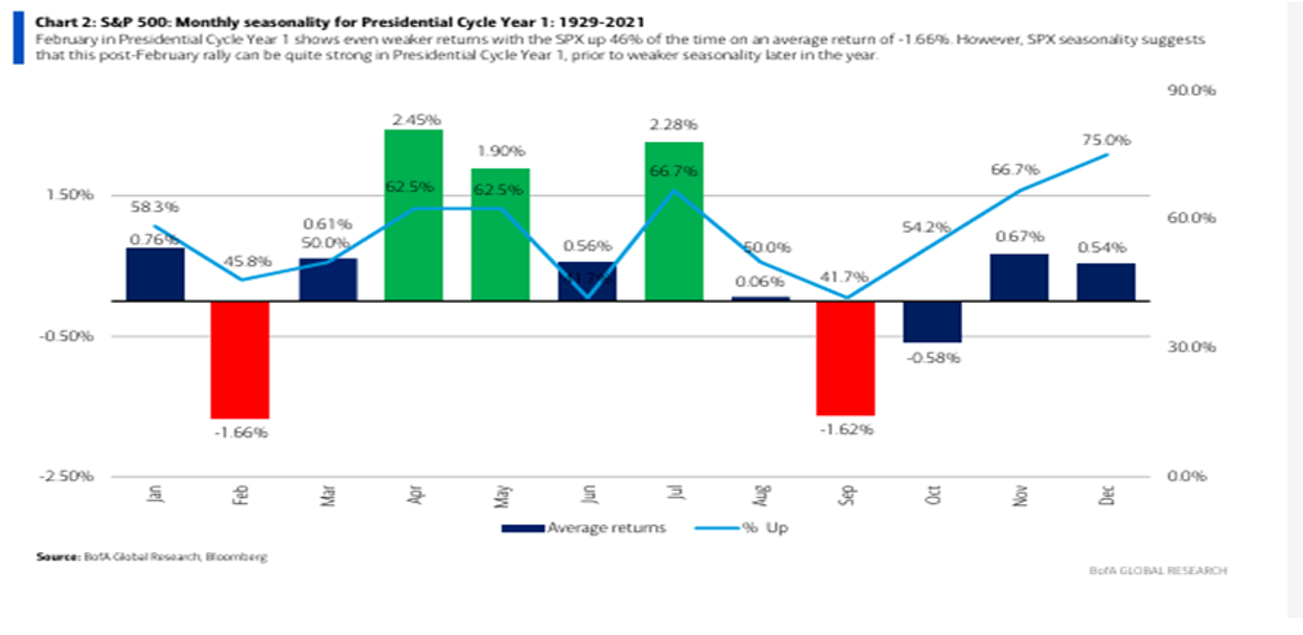

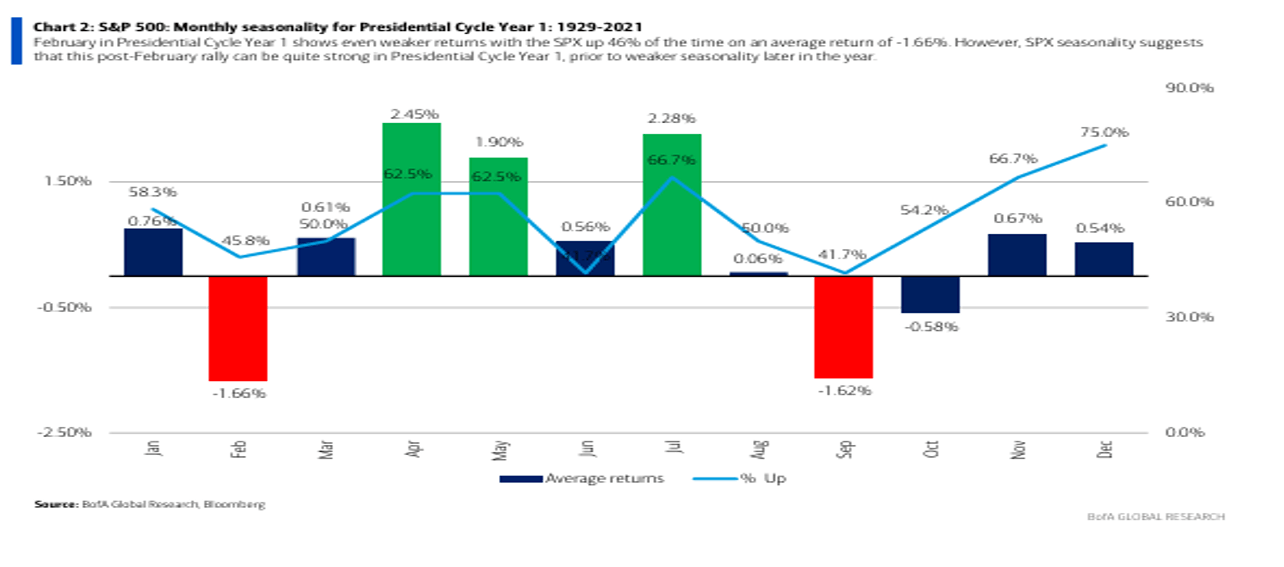

You can compare prior years including the first DJT term. However, the more important data set in my eyes, is the one we’ve presented for a number of months from the quant team and Steve Suttmeier’s group and BAC/Merrill Lynch. It’s the monthly average seasonal returns under the first year of a presidential cycle since 1929. Here’s that data.

As one can see, historically speaking, the first two months of the first year are underwhelming “net”. In fact, the whole first quarter was historically sloppy and choppy. So those who have followed the markets for a long time should not be surprised about the neurotic start to 2025 for the stock markets.

We’ve warned followers, that 2025 was unlikely to be a repeat of the gloriously boring and straight line up of 2017 under the first Trump presidency. The main reason we did not see a direct repeat coming in 2025 was the fact that in 2017 DJT focused on one and only one thing, lower taxes and getting that policy through congress. Lower taxes equal lower friction on consumers and corporations and shareholders love that! The GOPS linear focus on taxes caused the SP500 to move upward in 2017 in a near linear and historically low volatility year.

Compare that to DJT 2.0 out of the gate. As we have discussed, it appears that Trump is going for the early shock and awe taking on a myriad of policy changes in rapid fire manner. Immigration, tariffs, foreigner policy changes, and government firings and downsizing by the DOGE, while potential good for taxpayers and citizens over time, short term do what? Yes, they all increase friction in the economy. The all increase costs to the economy short term and shareholders and financial markets hate added friction, so the S&P 500 has gone almost nowhere since DJT was elected as of close Feb28.

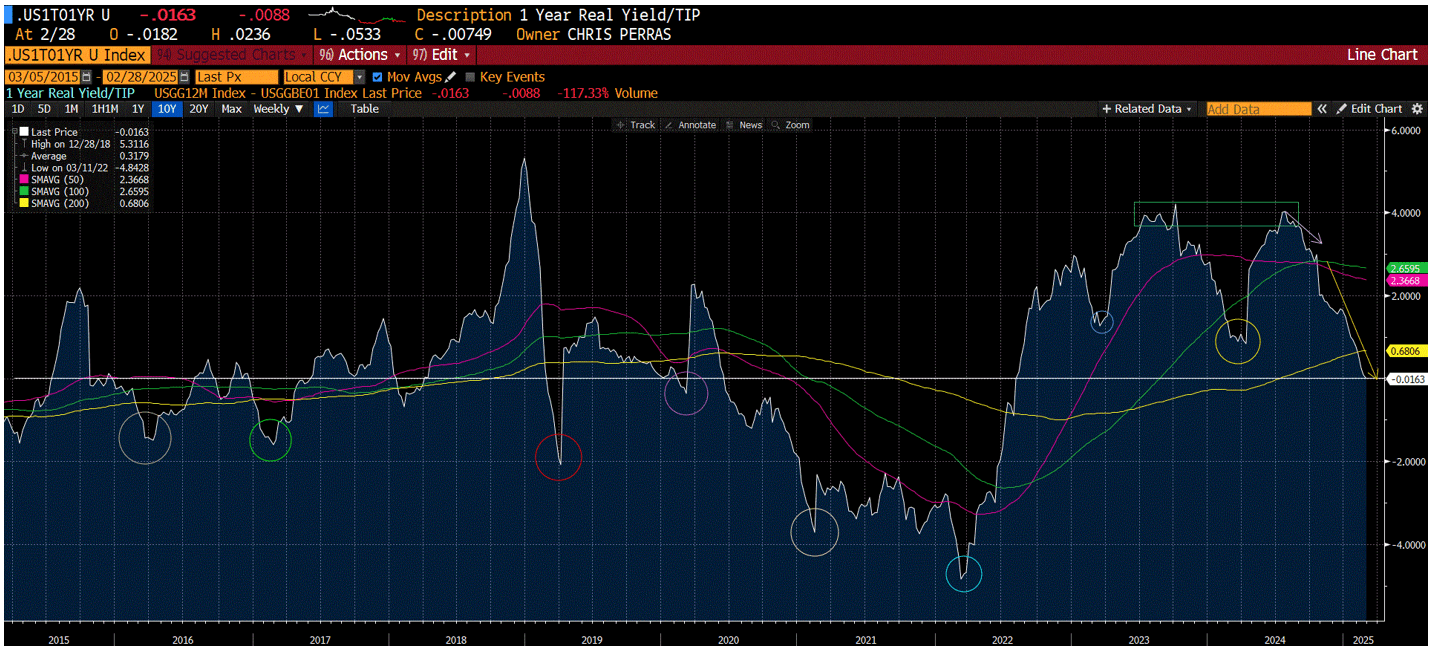

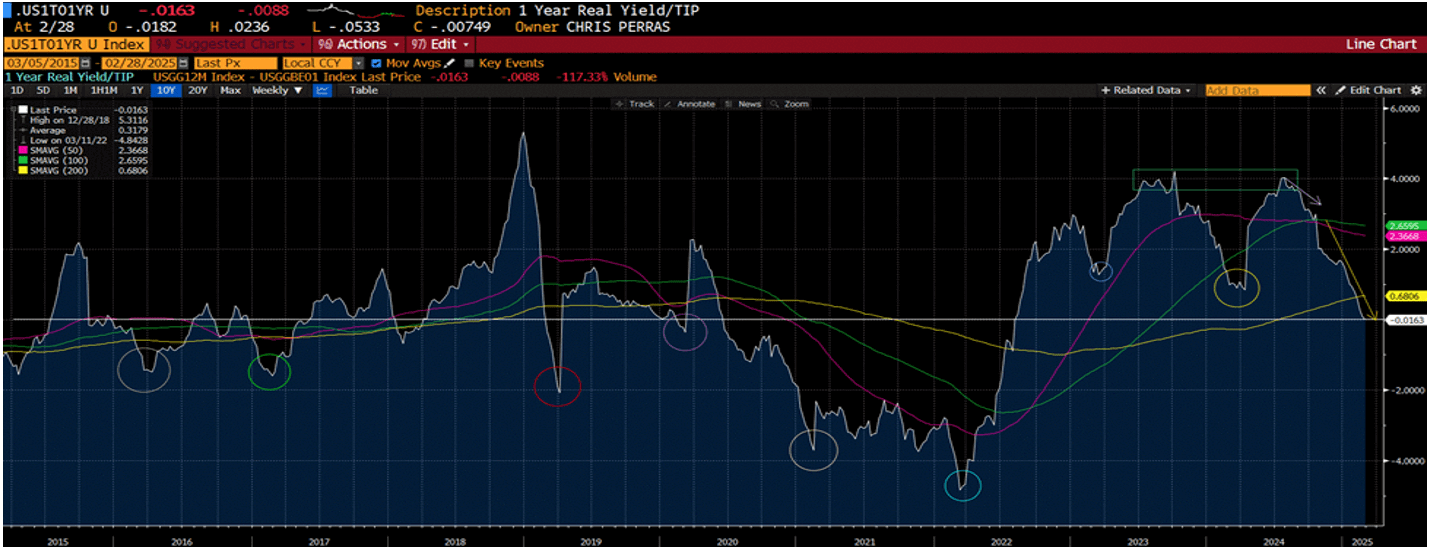

As we’ve pointed out while others weren’t the economy was already slowing into the election as the momentum in the Biden era spending programs like the IRA peaked in midsummer 2024 and were decelerating. As we also have discussed since December, the current policies in DC were crushing economic growth expectations. Here’s a chart of the fast twitch 1-year real interest rate. At peak Biden, IRA spending last summer it was 4%. Heading into the election it had been already cut in half to about 2%, and post-election has plunged back to 0%.

Why? Because all of the current policies in DC are actually anti economic growth in the short term. Immigration reform is anti-growth and consumption over the short term and is tightening policy. Mass federal government firings in DC, while long term likely more efficient and good for the US taxpayer, is short term bad for economic growth and consumer sentiment. Finally tariffs, investors stop listening to politicians, Tariffs are taxes on consumers and initially promote higher prices and lower unit consumption and both are bad for economic growth in the short term.

We discussed this economic weakness, and ongoing slowing fast trend for weeks in our “Behind the scenes, what many on TV won’t tell you, the economy is slowing fast” video, giving numerous reasons including the ending of the Biden fiscal stimulus sugar high as well as increased uncertainty and economic concerns of the Trump DOGE programs causing increased unemployment and dropping consumer sentiment and retail spending,

At the same time that growth forecasts are slowing to a halt, real time inflation expectations have steadily risen since the Trump administration took office. That’s the tariff programs as well as normal seasonality of inflation in the US.

It took me leaving town for others to show their concerns and sell stocks hard at the end of February. However, please remember that the second half of February is historically one of the worst periods for stocks during a year particularly under the first year Presidential cycle. Admittingly I was getting a bit depressed when I came back from my few days off in NYC with the markets dumping. However, there is hope investors and last weeks video, “Stock Rallies start here: Friday fights and Stock Flights”, that aired just, as the market reversed up strongly on Friday, was my first shot at bringing you some good news behind the scenes.

I actually got even more optimistic thinking about the next 18 months as the markets headed down early Friday as the Trump/Zellensky argument was happening on TV. Why? Here’s why. What if Trump is crazy like a fox? As a voter you don’t have to like him or his policies, but that isn’t what investing is about. It’s about return on capital and return on your investment. I got to thinking mid-week, in Trump 1.0 he focused on the easy things or actually one thing his first year in 2017, tax reductions, which all investors love. It was only after 2018 and on that he started focusing on the other policy agenda items, the hard stuff, the stuff that caused friction to investors and the economy. And he was doing that as the Fed was raising rates.

What if this time around, he and his staff have decided, let’s tackle all the hard stuff first. The economy is pretty good, albeit overstated, but let’s get all those friction items out of the way the first 6-9 months. Tariffs, immigration, efficiency/DOGE, defense spending. Let’s get that done first, and then we will focus on the easy stuff, the stuff everyone who is a shareholder or consumer likes, lower taxes, less regulation. Things that lower friction in the economy? Things that would accelerate the economy in late 2025 and throughout 2026 so GOP members can get elected or re-elected in the midterms in the 2h2026. What if, from an investor’s standpoint, he’s crazy like a fox? Think about that.

The good news looking forward to over the next 3-6 months is, seasonality is about to flip in investors’ favor as a tailwind, historically speaking. Looking again at the first-year seasonality of returns from Steve Suttmeier group. If history is a good guide, you’re supposed to be buying the February dip in stocks.

Why might this seasonality kick in positive for stocks in the coming days and weeks ahead? Here’s a couple of data series that support a rally starting here or shortly.

Historically, real growth expectations for the economy almost always crater the first few months in a year. Look at the fast twitch 1-year real growth chart. Look for the timing of the lows on the chart. I’ve circled a bunch of them.

Guess what time of the year each of those circles near the lows happened? Yeap, between the last day in February and the middle of March, call it option expiration in March, which this year is March 20th. If one were to look at the inflation expectations chart, want to guess what trend you would see there over long periods of time? Yeap, you guessed it. Inflation expectations usually peak? Right at the end of February or at the latest by mid-March. No guarantees in 2025, but history is on your side.

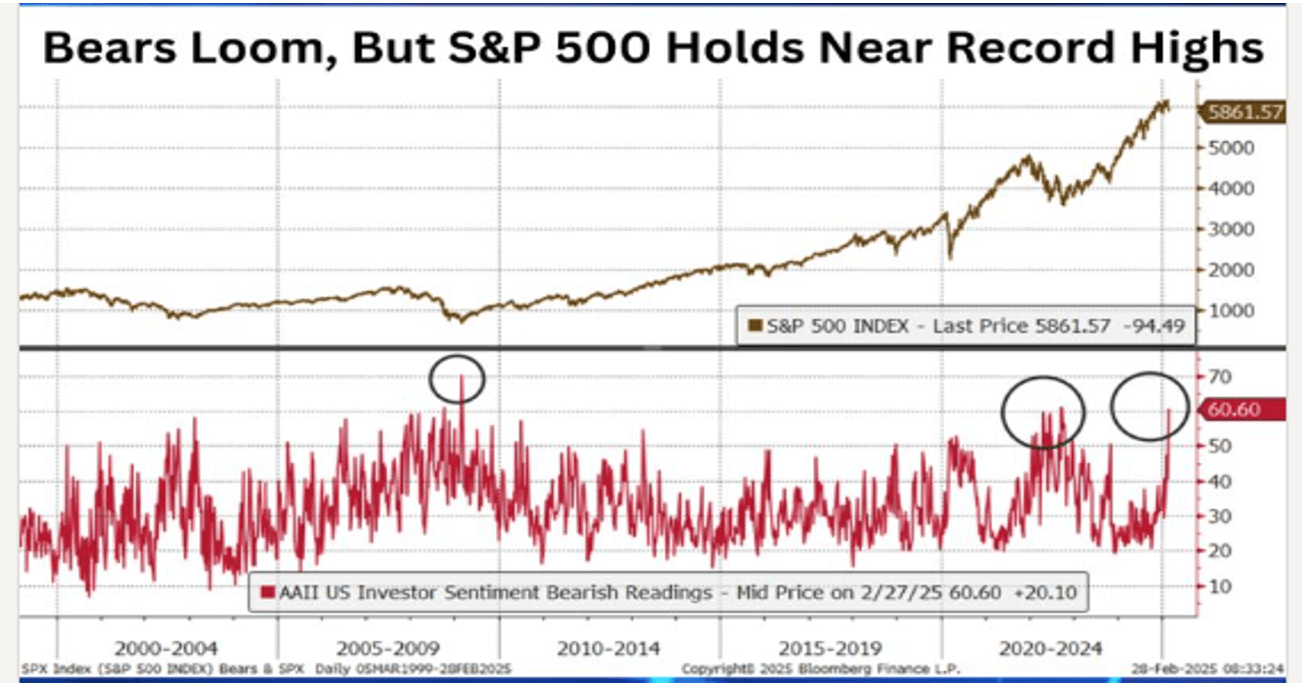

Finally, and possibly most importantly, in the span of less than 8 weeks since Trump was elected, bears are everywhere even with the S*P 500 only about -3% off its all -time high. We have referenced AAII investment sentiment data at extremes many times over my 7 years here at OHFG, including near the panic Covid lows in 2020, making a case for buying, not selling stocks. This measure of investor sentiment has historically been a very good contrary indicator with the markets troughing when bears are high, and the S&P500 peaking when bears are very low.

Here’s an updated chart of just the bearish component of AAII hitting highs only seen at the Covid lows and lows in the GFC in 1q2009.

Recall in March of 2020 the S&P 500 was down over -22% when the AAII reading hit +52%. The S&P500 is currently down only -3% and the bears have grown to 61%!

Not only have the bears reading skyrocketed, but the AAII bulls reading has plummeted. According to Chris Galipeau, Sr Market Strategist at Franklin Templeton, since 1986 there has only been 2 readings of AAII Bulls less than 20% and 3 readings of Bears greater 52% before the last reading. The 1-year average forward return from the bulls under 20% was +20.95% while the 1-year average forward SP500 return for Bears over 52% was a bit over +15%. A calculation using those returns off Friday Feb 28ths close of 5954 would equate to an SP500 of 6842.5 to 7200 over the next year, largely in line with our team’s forecast for 1q26. Of course, no guarantees and this is based on historic investor behavior repeating as it has been doing under the ”Old Normal” since October 2022.

As we have previously mentioned many times, soft landings in the economy do NOT guarantee no volatility. This time around, the Trump administration seem to be going for the early, “shock and awe”, taking on the tough policy issues first.

The good news? We are oversold and historically speaking, nearing what is normally a low in both economic growth expectations in the 1q, a seasonal low in the stock markets, and yes, a seasonal high in inflation concerns.

As you can see, while February has historically been down the first year of a Presidential term, that down has historically been the best buying Soft landings, however rare they are. For now, it’s been a bull market, we are in a bull market and however choppy things appear on your TV screens, we advise to continue to run with the bulls, and that’s bad news for the bears.

Investors know that regardless of the path for the economy and financial markets in the next few months, the investment team at OHFG will be here manning the ship and adjusting our models and long/short hedge equity fund where we can. We expect 2025 to be a very active year for active stock management.

Until next week, have a blessed weekend.

Do you need a retirement plan that goes beyond allocating funds to truly fit your needs? We can help you create a retirement life plan customized for your retirement vision and legacy. Call us at 877-896-0040 @or fill out this form for a free consultation: https://click2retire.com/Connect

Chris Perras

CFA®, CLU®, ChFC®

Chief Investment Officer, Financial Advisor

Chris is a seasoned investment professional with over 25 years of experience working with some of the most successful money management firms in the world. Chris has made it a point in his career to adapt as the market landscape changes, seeking to utilize the appropriate investment strategy for a given market environment. His transition from managing billions of dollars at the institutional level to helping individuals and families retire is guided by a desire to see first-hand the impact he is making in the lives of clients at Oak Harvest.

Click to subscribe: