Russell 2000 – Rotation Nation or just Squeeze me Seymour, more Little Shop of Horrors’?

On the morning of Thursday July 11th, the government released its much-anticipated monthly CPI inflation report. It was lighter than economists expected thus given hope to 1 – earlier Federal Reserve rate cuts and 2- more rate cuts in 2024 and 2025.Recall that in his last few speeches, Federal Reserve Chair Jerome Powell indicated that the central bank was aware that holding rates high for too long could hurt the economy. You’ve got positive CPI on the back of a slightly dovish Powell,, and kaboom.

When stocks opened, the S&P 500 gapped higher, but later sold off throughout the day and closed on its lows. While this happened, the long-maligned Russell 2000 gaped higher and strengthened even more on Friday. The variance between the 2 indexes was historically wide for the last 45 years. Yes 45 years! Even more extreme was the Nasdaq Composite, whose blistering YTD 2024 performance, led by large cap tech stocks, underperformed the Russell 2000 by more than 5 percentage points in what appears to be biggest daily gap on record.

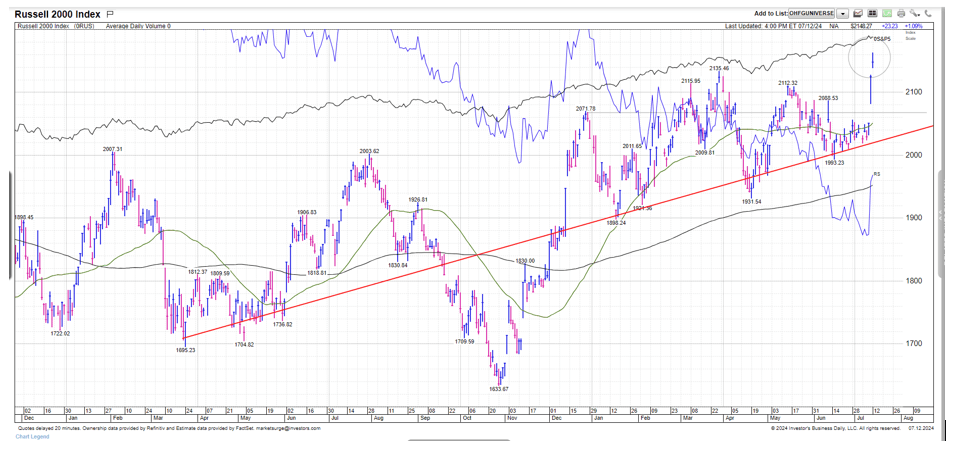

Here’s a daily chart of the Russell 2000. You can see the two huge up days a week ago. Friday July 12th is circled. The etf that best represents the Russell 2000 index is the IWM- iShares Russell 2000. In case you were curious over 30% of this ETF is sold short as a bet it declines or underperforms the S&P 500. That’s outrageously high for an ETF with over $65 billion with a B in AUM.

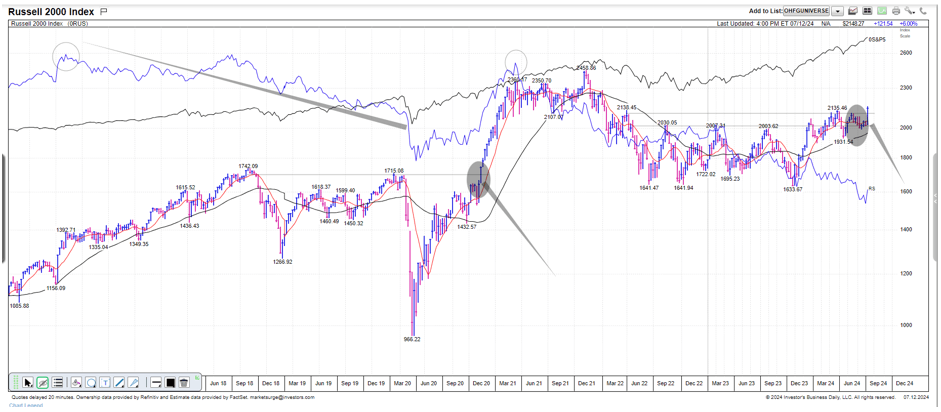

Unless you were short with all those folks, almost everyone and I mean everyone got excited about this move and was out commenting on it. It was historic yes, and it was a great move up for those who have been waiting for small cap stocks to catch up, but was it the beginning of a major secular shift? Or just the start of possibly a 2–4-month bounce in small caps? No one can tell you for sure. Here’s a longer-term chart of the Russell 2000 index. It has finally made both new 52 week and 2-year highs., so the chart has “broken out” of a 2 year trading range.

However, as one can see it still sits almost 10% lower than the highs set in late 2021.near 2450 on the index. Moreover, if one looks closely at the continuous blue line in the background of these charts, that’s the relative strength of the Russell 2000 vs. the S&P 500, you can barely see a blip up in that metric. Since the Russell’s relative strength peaked in March 2021, its been 3.5 years of woeful underperformance relatively and absolutely versus the S&P 500.

An optimist would look at the chart and say with the Russell 2000 having a weekly close above 2125/35, the setup looks a lot like late 2000 which I have circled on the longer-term weekly chart. Back then, the Russell broke out to a new 1 and 2 year high and went on to race up over +600 points or another 35% over the next 9 months. A similar move now would equate to close to 2850 on the Russell. Well I’m sorry to say, while I think it goes higher, I cant get to a move that high over the next year.

Why? Because the cause of the move up was 1 – short covering by poorly positioned hedge funds and quants, and 2 – lower inflation lifting expectations that the Fed cuts sooner or deeper which could extend the economic cycle and reaccelerate growth in 2025. But behind the scenes, what I see really going on is more of the same in the economy. Slowing. And while slowing inflation and slowing growth is good at first as investors think goldilocks and a soft landing. The data behind the scenes is creaking and warning that the Fed waiting until September to cut rates might be too little too late. Remember that a slow growth or recessionary environment would be tough for small-cap stocks, which tend carry more debt and to be more economically sensitive and oriented to US consumers more than larger companies.

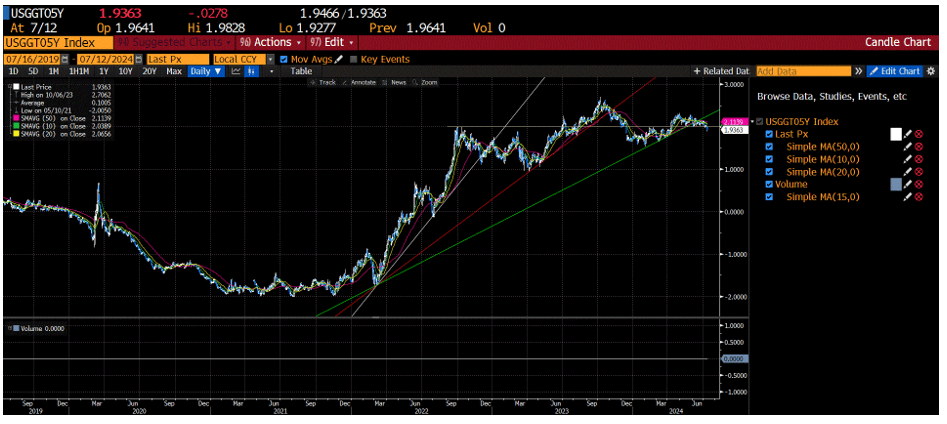

Remember back to our previous discussions of “real growth and real interest rates”? Real interest rates, being the component of interest rates that is the premium to inflation. The one that controls equity risk premium and asset valuations. The one that the Fed refers to when they are discussing being tight or loose in money? Well the real time real rate has been great at signaling worsening economic growth that goes beyond just “slowing” that is reported by economists and groups like the Alanta Fed GDP now tracker. Here’s a daily chart of the 5-year real interest rate the last 5 years. Followers of OHFG will recall how in October 2022 and then again in October 2023, based on this factor and a few other, our investment team signaled what we thought would be a bottom in stocks and strong forthcoming rallies.

What’s interesting is on Thursday July 12th when the CPI data came out, this metric broke below 2 and most of its moving averages. That’s why the Russell 2000 ripped. That’s why the computer algorithms bought and sold different baskets of stocks. Remember slowing and slower is good, until it isn’t. Isn’t as in when and where?

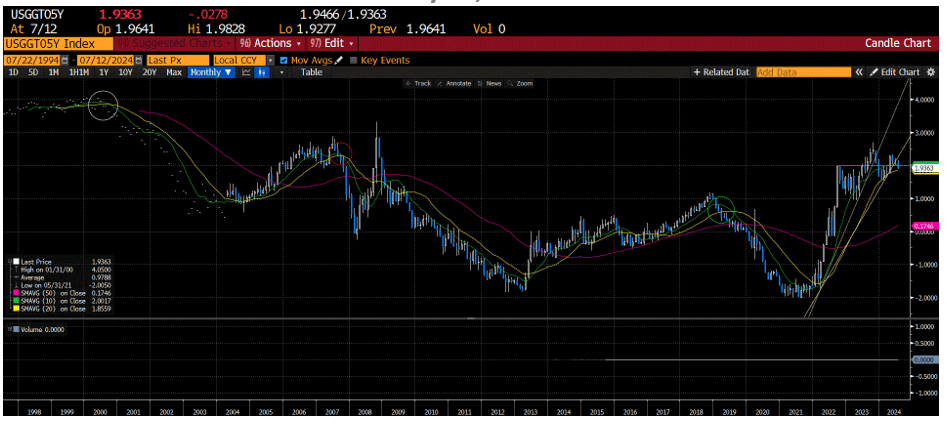

Well, here is a monthly chart dating back 25 years of the same 5-year real interest rate.

The current pattern looks like a big head and shoulder top to me. Many investors would think that this is a good thing, Lower interest rates is good on the good bad right? Shouldn’t all boats rise in the market with lower rates? Unfortunately, prior to the advent of the GFC in 2007/08, and implementation of quantitative easing, and other post GFC programs, this is actually a warning flag in my book. As one can see, prior to these programs, when markets were less influenced by the Fed, when real interest rates have broken moving averages and started downtrends like late summer of 2000 and late summer of 2007, historically its started the clock ticking for a more major slowdown and eventually a recession in the next 12 months. That wasn’t the case in 2h09 0r 2018 because the Fed jumped in with special programs, they jumped in with the Fed backstop and Fed put in an extraordinary way. But investors, do you believe they will immediately break out that same play book if they see a significant slowdown? After trying for 2 years to regain their reputation as independent?

I don’t know if they will, but I wouldn’t bet my portfolio and all my gains over the last 2-3 years being greedy thinking that the Fed backstop will be in full force in late 2024 or 2025. As we’ve previously discussed, if you are a retiree or near retiree who has had a tendency to get emotional about your investments when the markets are down and volatility is high. Does it take every ounce of your willpower not sell the lows? Dot com bust? GFC recession? Covid pandemic?

If over the years you have found yourself reacting emotionally in your portfolio to Presidential elections and their uncertainty, now is the time to talk to your advisor to walk through your plan. Well in advance of other investors concerns of will the 3q24 be a soft-landing pullback that refreshes, or the beginning of a much more painful economic and market downturn

Discuss how much risk is in your allocation plan under downside market scenarios just in case the economy rolls over in late 2024 and 2025 regardless of who is elected this November. While most 3rd qtr selloffs are just cyclical corrections and short-term pullbacks in otherwise long-term bull markets and economic expansions, it is virtually impossible to tell if that selloff is a mild correction in an economic soft landing, or if it’s the beginning of something more dire like it was in 2000 and 2008. I will argue with all takers that it didn’t matter who was elected those years, Bush or Gore in 2000, or Obama or Cain in 2008, the ultimate winner was already dealt a bad hand by the Federal Reserve and the economy by the time they were elected.

Investors, if you are going to make reallocation decisions to shift money out of stocks and equities into less volatile assets, its best to do it when indexes are up, and volatility is low. Not the other way around.

If you are uncomfortable with wider range of possible equity outcomes, the Oak Harvest team has launched a new strategy that retains the ability to go long stocks, short stocks, as well as buy partial hedges and shock absorbers for a stock portfolio. Information on this exciting new strategy of ours can be found at www.OakHarvestFunds.com.

From the whole team here, thank you and have a great weekend.

Do you need a retirement plan that goes beyond allocating funds to truly fit your needs? We can help you create a retirement life plan customized for your retirement vision and legacy. Call us at 877-896-0040 or fill out this form for a free consultation: https://click2retire.com/Connect

Chris Perras

CFA®, CLU®, ChFC®

Chief Investment Officer, Financial Advisor

Chris is a seasoned investment professional with over 25 years of experience working with some of the most successful money management firms in the world. Chris has made it a point in his career to adapt as the market landscape changes, seeking to utilize the appropriate investment strategy for a given market environment. His transition from managing billions of dollars at the institutional level to helping individuals and families retire is guided by a desire to see first-hand the impact he is making in the lives of clients at Oak Harvest.

Click to subscribe: