Pres. Trump vs. Fed Chair Jerome Powell: Who’s Right About Interest Rates in 2025?

My title this week, Interest Rate Smackdown: President Donald Trump vs. Federal Reserve Chairman Jerome Powell, whose right on interest rates? Shows my age, I’m the lost generation Gen X, who grew up with both Ronald Reagan as President and the rapid emergence of the WWF, World wrestling Federation as entertainment with Hulk Hogan, Andre the Giant, Randy Savage, and the “nature boy” Ric Flare, “wheew” rocking to prominence. For those not familiar with wrestling and bigger boxing fans, I probably should have titled this one “Let’s get ready to rumble”, the famous opening used by ring announcer Michael Buffer who also was the exclusive ring announcer for President Trump owned casinos when they hosted boxing matches.

This week, we aren’t talking directly about stocks and the stock markets. Nope, we are going to focus on the bond market and more importantly the direction of interest rates that the Federal reserve, ex programs like QE, has control over, those are shorter term interest rates. While many investors ask what interest rates are doing and directly go to what the Fed’s actions are, more seasoned investors know that the markets and investors control the level of most interest rates.

The Federal Reserve sets the federal funds rate. What this rate? It’s the interest rate depository institutions, mostly banks, lend reserve balances to other institutions overnight on an uncollateralized basis. Basically, it’s the rate banks charge each other for short-term loans. Time and time again on TV we here many commentators talk about “Fed Funds futures”, which is the markets guestimate about what direction, when, and by how much the Fed will change this rate in the future. As we’ve discussed for years at OHFG, historical data says, tracking, discussing and worrying of FFF is meaningless and unpredictive of future Fed action outside of the 5-7 day window in front of each Fed meeting. In other words, the Fed historically has almost no real idea where they will be setting interest rates out months, or quarters in the future, let alone years, and yes, investors, the Fed is generally a momentum investor. Rate cuts lead to more rate cuts. Interest rate increases lead to more increases.

So, to the here and now. On Thursday, May 29th, President Donald Trump called Federal Reserve Chair Jerome Powell to the White House for their first face-to-face meeting since the President retook office in January. President Trump told chairmen Powell that he thought Powell was making a “mistake” by not lowering interest rates.

Should investors be surprised by President Trump’s actions and opinions, certainly not. Why? Because every President, whether they are Democrats or Republicans. wants the Fed to lower interest rates. Every President wants an ally in the Fed and the tailwind of lower interest rates to help push the economy forward. To help better their own agenda. Lower rates and looser money? Easier for business to get credit at the bank and cheaper to invest. Generally easier for consumers to get loans at the banks and buy houses and cars. Consumption and service is near 75% of the US economy. Most individuals and businesses, ex banks themselves, like low interest rates or lower trending interest rates.

Post the two’s meeting, the Fed released a statement that the FOMC, will “set monetary policy, as required by law, to support maximum employment and stable prices.” They went on to say that their decisions will be “based solely on careful, objective, and non-political analysis.”

Ok fine, we know the players. We also know their goals, mandates, objectives and desires, political or not. But who is right right now? Is the President right and the Fed is too tight? Should the Fed be cutting rates? Or is the Fed right by holding pat concerned over Trump administration tariff policies and their effect on future inflation?

Well, let’s check the tapes and the data and come to a conclusion. First, lets check the tapes over the last 10 years, who has the better track record at predicting the economy and if rates are too high, the Fed to restrictive and rates should be dropping.

Quick flash back to a similar time period in the 2h2018 during Trumps first term. Post the 2017 Trump tax cut sugar high in the markets and economy, the Fed went on an aggressive interest rate increase policy. In early 4q18, the President went on the attack, publicly criticizing the Fed for its rate increases. The President, being his direct and unfiltered self, called the Fed “crazy,” “loco” and said it’s “gone wild” with interest-rate hikes. He went on to blame the central bank, for the sharp decline in the stock market in mid October 2018.

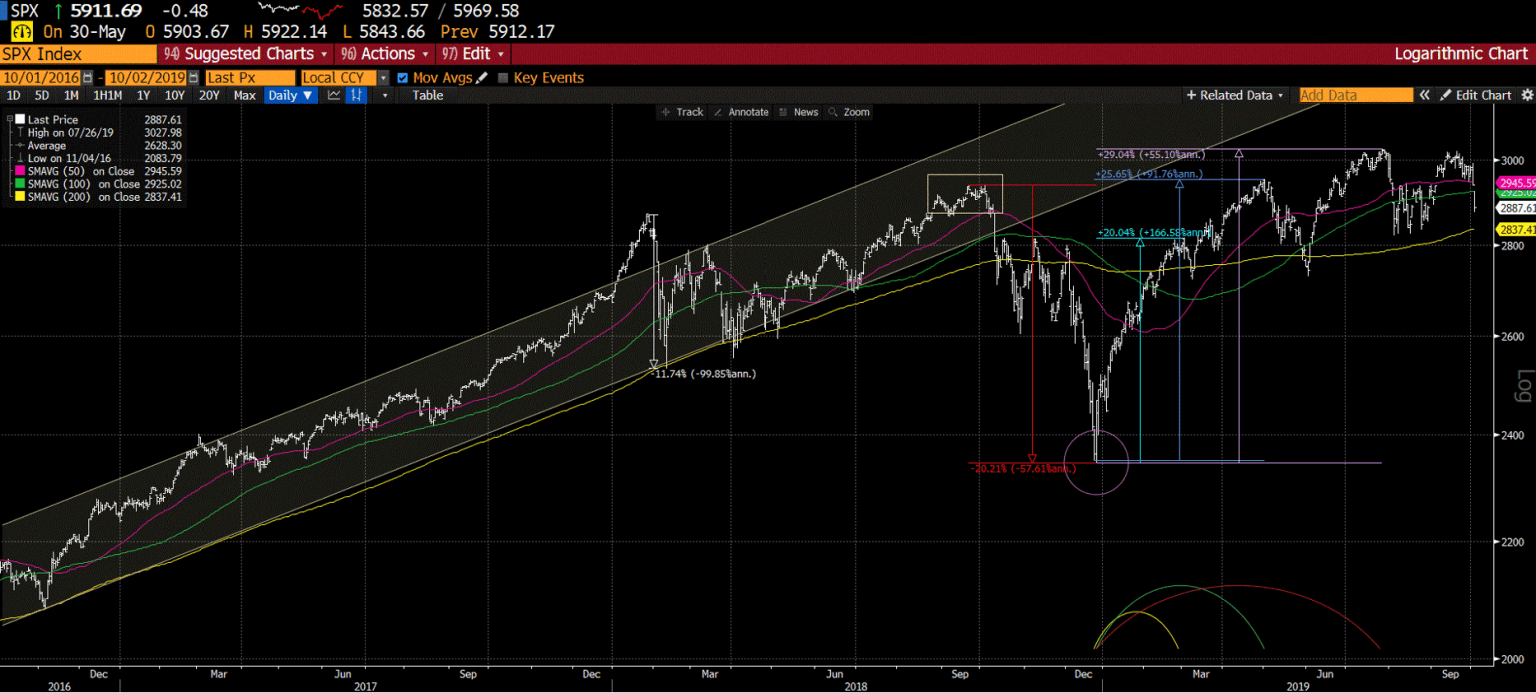

To remind investors, here’s a chart of the S&P 500 from Trump first term including the historic, near linear low volatility straight line up in 2017, followed by a series of sharp corrections to start 2018 when the President flipped policies to focus on tariffs and China as an adversary, and the markets late 2018 selloff of almost exactly -20% into the XMAS eve low after the Fed raised rates again on December 18th while the economy was already slowing and softening into year end.

As it turns out, the President was correct back then about the economy slowing and only a few weeks after the Fed raised rates in mid-December 20218, in early 2019, The Fed had to quickly switch their gameplan.

Partly due to the impact of the administration’s trade war combined with the effects of higher interest rates, the economy slowed, and Powell and the Federal Reserve quickly had to pivot away from a tightening policy. Eventually the Fed cut rates 3 times in 2019, July, Sept, and October. To offset the negative economic impacts of both the Fed raising too much in 2018 and the trade policies of the Trump administration.

So, I have to give round one of the bout, smackdown, and fight to President Trump. His verbiage was a bit rough for my liking, but it turns out, yes the Fed was too tight back in 2018 for the economic circumstances back then.

Fast forward to today. Is the President, right again about monetary policy? Is the Fed too tight? Is the Fed and all their economist too worried about inflation induced by Trump tariffs 2.0 and not worried enough about an economic slowdown its causing? Should the Fed be more anticipatory, kind of like their 50-bps rate cut move in front of the election in 2020?

The Fed is currently holding its target range for the federal funds rate at 4.25% to 4.50%. Is this too tight? Is the President right again about interest rates? Followers know, I’m a stickler for real time market data. Tradeable data or market-based trends. I hate consumer “surveys”, like the Michigan consumer sentiment or inflation expectations surveys, that can be manipulated, tend to be surveying emotionally charged individuals, and historically are not predictive at all of the future. The real time data says? Yes, the President has a better handle on where the economy is going and where interest rates should go. Yes, some of this is being induced by his own policies, but the Fed is suppose to react to the hand they are dealt regardless of whose in office.

Investors, the real time data says, inflation peaked in March 2022, 3 months before the Fed started raising rates, and its been in a steady down trend for the 3 years since. Pick a maturity for inflation break evens in the bond market, 1, 3, 5, 10, 30 years they are all trending lower for the last 3 years, they all peaked seasonally as they tend to in late March early April, and they are once again heading lower. 30-year, 2.3%, 10-year 2.33%, 5 year, 2.4%, 2 year 2.6%, and 1-year 2.8%. The 5yr 5 yr forward BE inflation rate is also 2.3%.

Yes, those levels are all above the Feds 2% goal, and yes the shorter term 1 year rate is the highest, but one would expect that as the tariff price shock hits a bit short term, but are any of them out of control like 2022, post Covid, Fed and Biden induced economic consumption led sugar high? No.

Here’s the jiggly and fast twitch 1-year BE inflation rate the last 10 years. Sure, enough reaching its zenith in March 2022 at 6.35%, steadily declining into the summer of 2024 Biden IRA economic peak spending, rapidly rising again on Trumps election, yet peaking in March 2025 on Trump tariff talk.

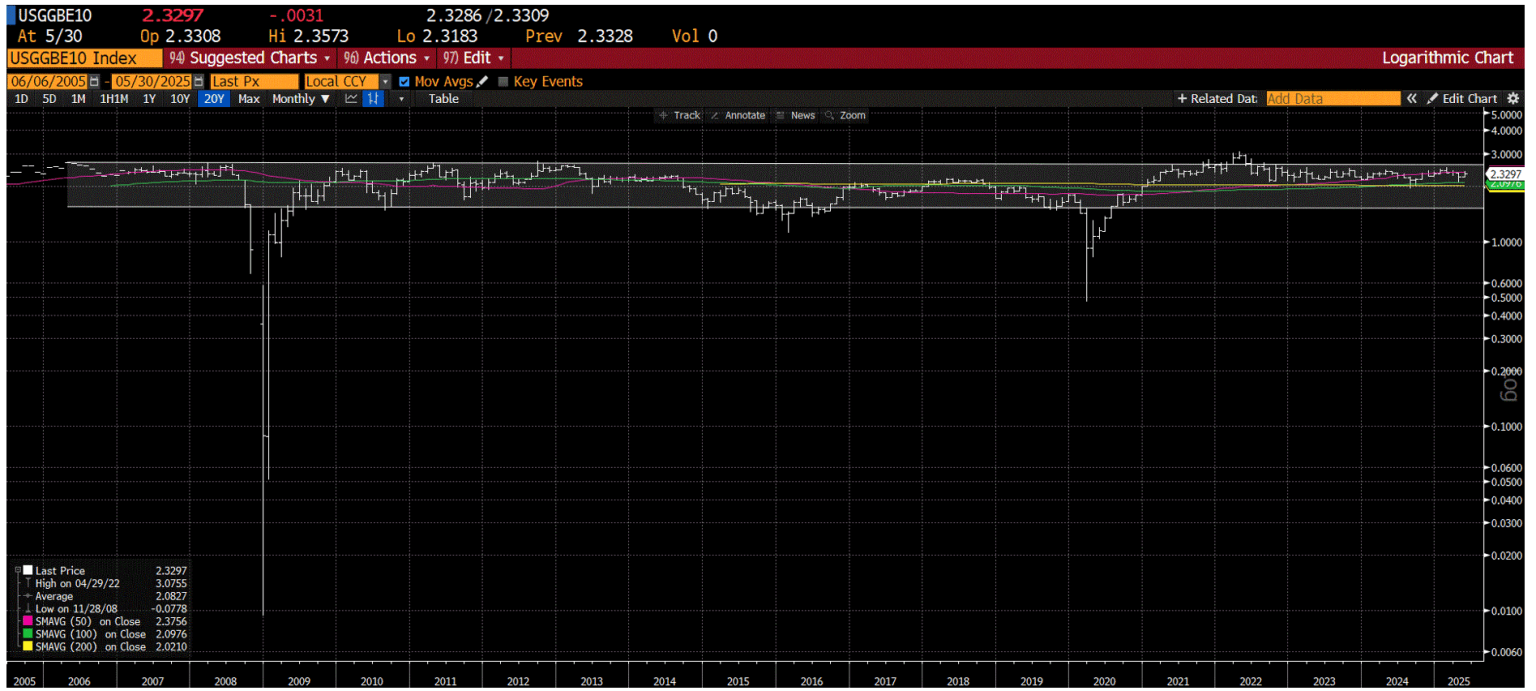

Ok, you want something longer term looking than one year. Something that looks out past this President to the next one or two? Maybe to see if this administrations tariff policy is ushering in a period of stagflation”. That terrifying word that keeps getting thrown around on TV by many doomers who seem to have been wrong for 15 years in counting on the stock markets? Who have been repeatedly wrong calling almost annually for a recession? Ok, lets look at 10 year inflation BE rates.

Right now they sit at 2.32%. Here’s a 20 year chart of those rates. Let this chart sink in for a bit.

Over the last 20 years, during periods when the Fed was mostly fearing deflation and worried that there wasn’t enough inflation in the economy, rates almost never dropped below 1.6%. Meanwhile throughout the 2006-2013 period, this rate also reached 2.75%. For the most part, for 20 years, the 10-year Inflation BE rate has bounced between 1.6% and 2.75%. Right now we are closer to the high side of that bound but its trending lower, not higher, since its peak in March 2022.

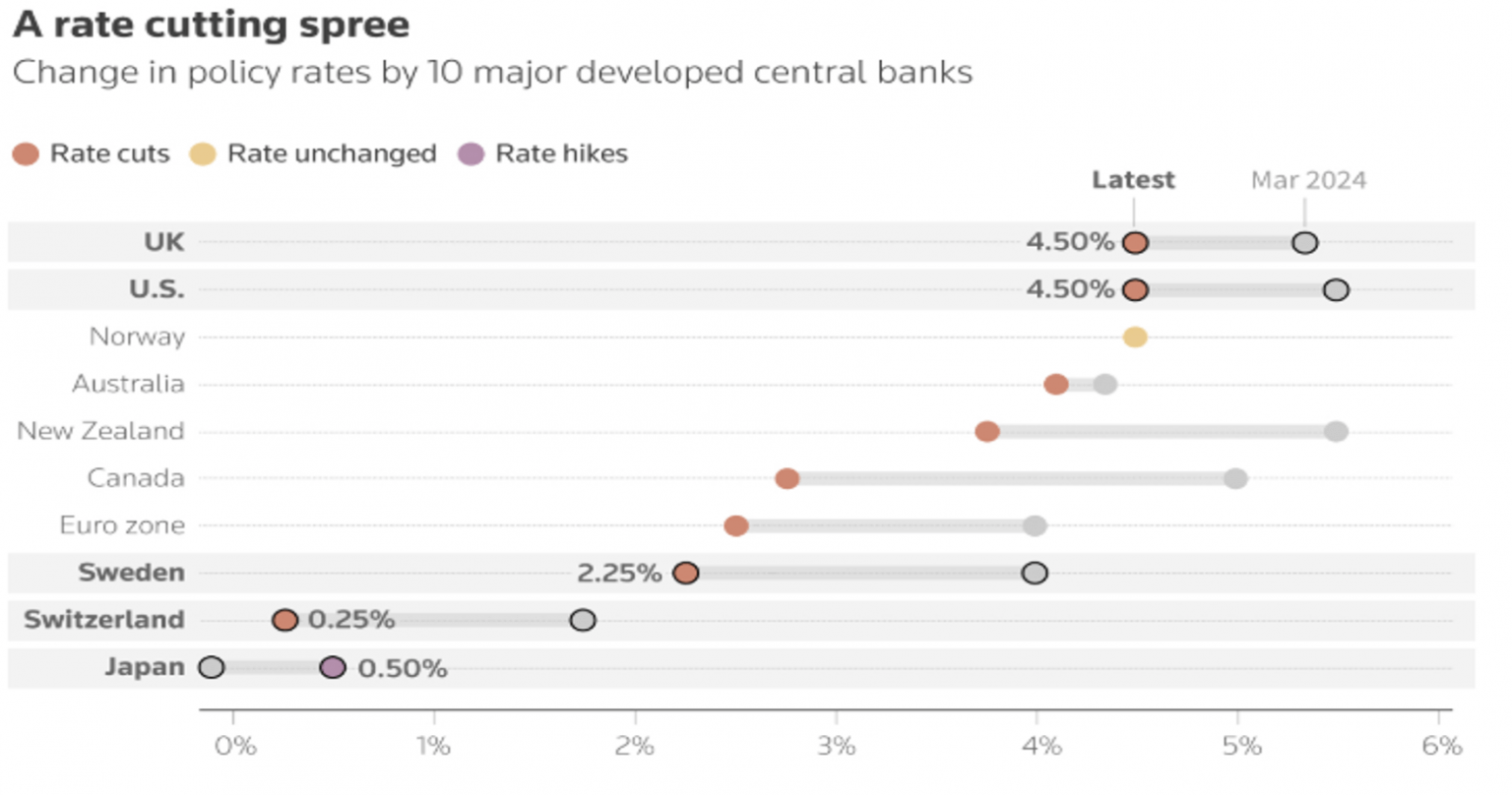

Investors, most large central banks around the world are cutting interest rates. They have been since 2024. Canada seems to always be first this cycle, and they started the parade last year. Here’s a table from Reuters with data from the LSEG. The US has been on one of the slowest paths of rate cuts, and remains one of the most restrictive monetary policies in the world.

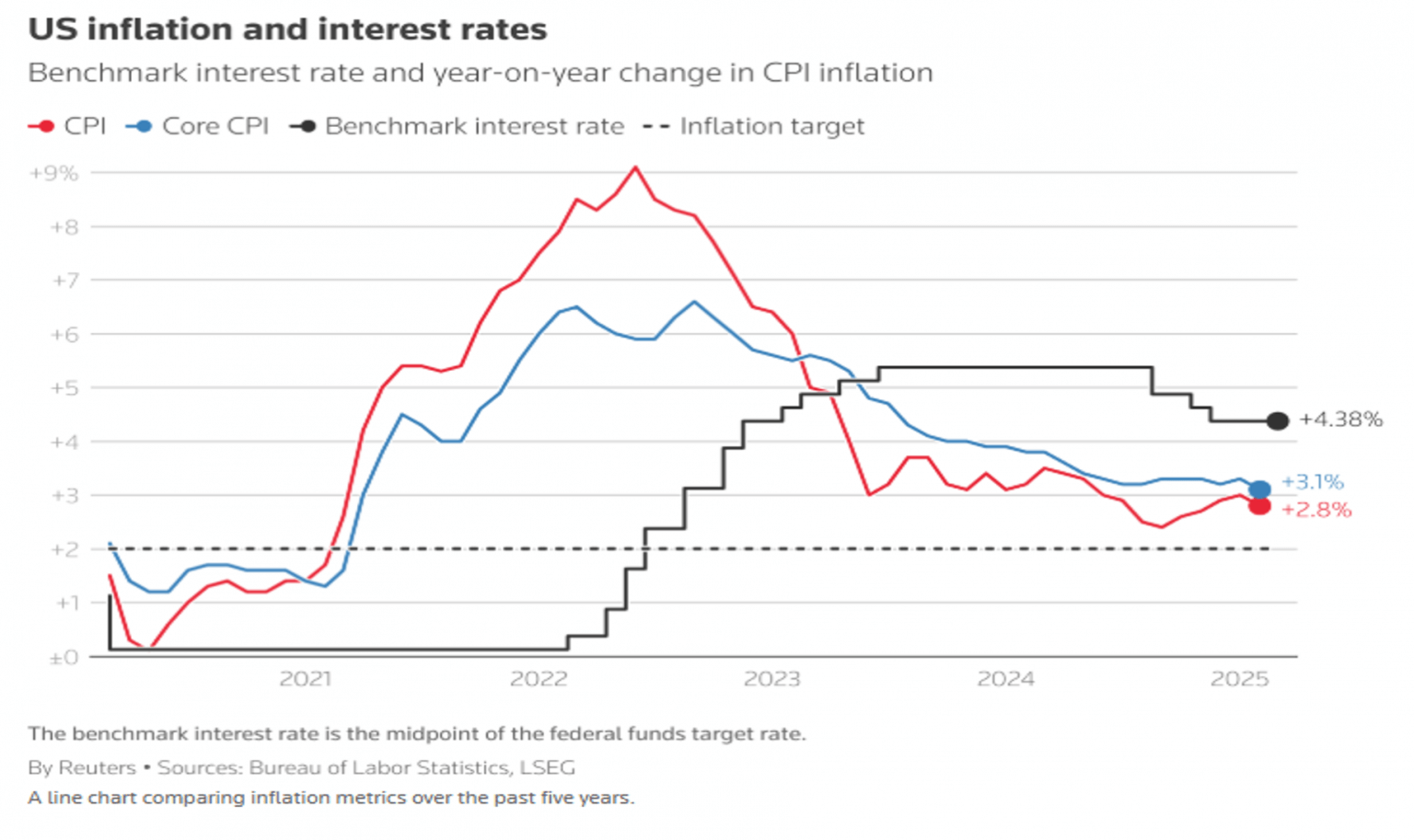

How restrictive? Another chart from Reuters showing the Fed Funds rate versus both our CPI and Core CPI, two metrics the Fed watches.

Looking at this chart, the Fed funds rate is anywhere from 125-150BPS higher than the USA inflation rate which is trending lower, and hasn’t been over 4% since early 2023. Investors, in my book, the Fed is too tight. They have room to cut now and should.

Inflation will continue coming down while the economy slows throughout 2025 regardless of the 1-time tariff affects. Have you looked at housing pricing and demand? Yes prices are high, but the housing market is now favoring buyers over sellers. Price cuts abound in almost every housing market I see to induce buyers. Airfares will likely come down as leisure demand into the US dries up for a bit. Deals at restaurants are picking up. Chilis led this charge about 12-18 months ago and many are following. Apartment rental rates look to be easing, and higher initial concessions being given to renters in many large cities across the USA just as job hopping, the “take this job and shove it index”, is slowing and new multifamily units are hitting the market.

Investors, I have to say, the weight of the evidence for the second act of Trump vs. Powell looks also to be in the Presidents favor. In my analysis the weight of the evidence is on the Fed being too tight in their monetary policy. Whether they are being political, to academic in their line of thinking, or just too slow and reactionary? I don’t know, but on this subject, should the Fed restart cutting rates sooner not later? I’ll place my vote in the Presidents camp. Let’s restart the Fed cuts and keep this economic expansion going slow and steady for a few more years.

Regardless of what the Fed does on interest rates over the coming months, or whether a more public fight breaks out again between the President and Powell, the investment team at OHFG will be here manning the ship and adjusting our models and long/short, hedged equity fund, OHFGX, where we can.

Until next week, have a blessed weekend and know that the OHFG team is doing what we can to plan for you and your family’s future regardless of what stage you are at in your career or retirement.

Do you need a retirement plan that goes beyond allocating funds to truly fit your needs? We can help you create a retirement life plan customized for your retirement vision and legacy. Call us at 877-896-0040 or fill out this form for a free consultation: https://click2retire.com/Connect

Chris Perras

CFA®, CLU®, ChFC®

Chief Investment Officer, Financial Advisor

Chris is a seasoned investment professional with over 25 years of experience working with some of the most successful money management firms in the world. Chris has made it a point in his career to adapt as the market landscape changes, seeking to utilize the appropriate investment strategy for a given market environment. His transition from managing billions of dollars at the institutional level to helping individuals and families retire is guided by a desire to see first-hand the impact he is making in the lives of clients at Oak Harvest.

Click to subscribe: