Buy the Dip (“BTD”) Week 2

Market Update 2020-1-23.

U.S. equities look to open about 0.5% higher on more positive vaccine news, with AstraZeneca and the University of Oxford the latest to claim effectiveness in preventing infections. Moreover, the FDA cleared Regeneron’s antibody drug which has the potential to reduce the number of severe cases and hospitalizations.

Equity markets were a mixed bag last week after the prior week’s strong rally. The S&P 500 slipped 0.8%, with strength in energy and banks offset by weakness in health care and utilities.

On the vaccine front, Pfizer rolled out even more optimistic testing results, and said that it would seek emergency U.S. government approval. Vaccine announcements have been a big driver of the rotations in the markets. The laggards of the past 2 years, energy and banks, are up by double-digits over the past month on the S&P 500, while technology and consumer discretionary are flattish. The latter groups are up almost 20% each since COVID-19 began, while banks and energy are down 23% and 35%, respectively. Small caps stocks have also been a big beneficiary of the shift to vaccine trading and rotations. Small caps continued to rally last week, up 2.8%, while large caps were down.

Economy

Back in the economy, the data was generally positive. Retail sales were solid. In the U.S., we are seeing record-high homebuilder confidence, near-2005 levels of existing home sales, and robust price gains. That being said, construction costs are rising faster, and we expect housing stocks to lag the market after Q1 2021.

Markets

On November 19, the US stock markets observed an extremely rare and positive trading event, a “Zweig Breadth Thrust”, named after the late financial markets’ trader and historian, Marty Zweig. Since 1950, for only the 24th time, his indicator exceeded 1.85x. Of the prior 23 occurrences, only once were stocks down over the next 6 months. The average of the 22 up occurrences over the past 70 years was +13.65% with an average maximum drawdown of only 1.78% over the 6 months. History does not always repeat and there are no guarantees, but this data could be positive for the stock market.

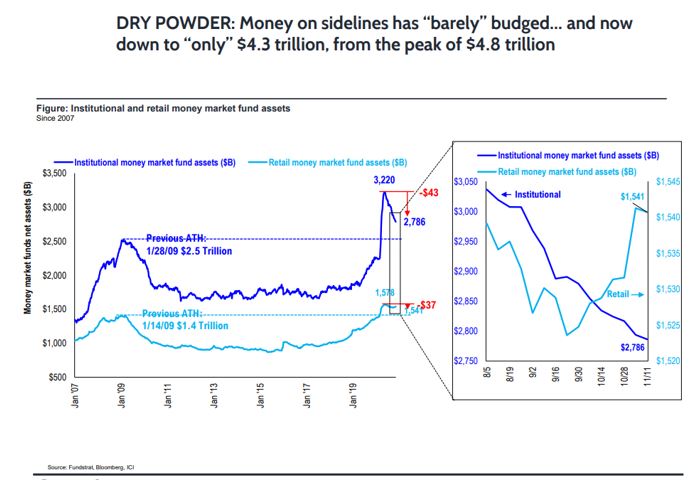

Additionally, while much is made on the news about stocks being at new all-time highs, one can see from the attached chart from FundStrat that there is still trillions of dollars sitting idly by on “the sidelines.” While institutional investors have been putting money to work the last 6 months, retail investors have largely been sitting on their hands waiting.

Resources

- Please listen to our podcast from three weeks ago entitled: “Waiting No More: This is How Early Bull Markets Look.”

- Our complete H2 2020 outlook was posted in July and can be found by clicking here.

Weekly market updates contain general information and expresses views of Oak Harvest Investment Services. Data, Articles, and information cited are believed to be reliable at the time of creation, but are not guaranteed. Nothing in this content is intended as, nor should it be regarded as, personalized investment advice. Strategies and ideas discussed may not be right for you. Views and opinions expressed may change without notice and do not constitute a recommendation, or an offer or solicitation to buy or sell securities. In addition, Oak Harvest makes no assurance as to the accuracy of any forecast made. Indexes like the S&P 500 are not available for direct investment and your results may differ. Past performance is not indicative of future results. Investing involves the risk of loss.