07.20.2020 – Market Update

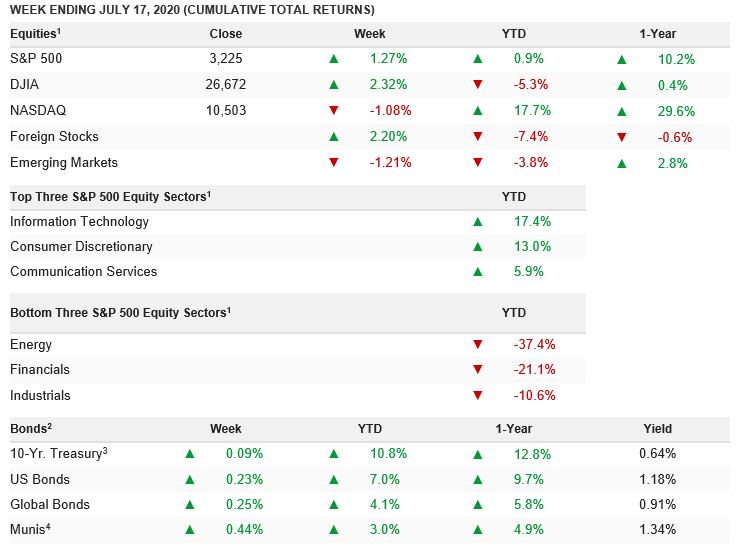

The S&P 500 cash index closed last week at 3225, up 1.25% on the week, which was an option expiration week. The S&P price return is now almost flat on the year on a price basis (-.2%), up about +1% year to date including dividends, and up +10.2% year to year (off an easy comp). The path to 3225 has been anything but “normal” due to the first quarter induced Covid-19 virus economic and stock swoon, however the current resting point is pretty darn close to normal for both an election year and a normal seasonal pattern. Earnings season continues to ramp this week and we should be getting additional positive vaccine data the first half of the week from Pfizer and Astra Seneca (the data has been leaked for about a week).

Industrials and materials were the biggest gainers. Technology has rallied more than 16% in 2020, while consumer discretionary is up more than 12%. Financials rose 3.2% on the week but are still down more than 15% on the year. REITs continue to lag despite the plunge in long-term yields

The domestic economic data flow continued to point to a rapid recovery, particularly in housing. The Citi economic surprise index reached an all-time high of +270 after reaching an all-time low of -125 in mid-April. If that is not a “V-bottom” in the economy versus expectations, I do not know what is. U.S. retail sales jumped 7.5% in June after an 18% surge in the prior month. Retail sales activity is now less than 1% below pre-COVID levels. Excluding gas stations, retail spending has pushed above those levels, led by surges in grocery stores, building materials and online stores.

For the technicians out there, last week also saw a bullish crossover, with the 50-day moving average moving back above the 200-day, we have not seen that since March. That “indicator”, referred to as a “Golden Cross” is not early in daily moves in the averages. That “Golden Cross” indicator is a lagging indicator and the market historically pulls back to its rising 200 day moving average, usually over two to two and half months during late summer, one more time before heading materially higher.

In DC, politicians keep bickering about passing another stimulus bill. The Senate will convene this week to debate the issue. Topping the list of questions is whether to extend the $600 weekly supplement to roughly 25 million laid-off workers, tallying $60 billion per month. The House has already passed a bill with about $3 trillion in aid, including another round of checks to households. Senate Republicans are looking for a more targeted approach to providing relief to businesses and workers that would be closer to $1 trillion, which is still a massive 5% of GDP.

Weekly market updates contain general information and expresses views of Oak Harvest Investment Services. Data, Articles, and information cited are believed to be reliable at the time of creation, but are not guaranteed. Nothing in this content is intended as, nor should it be regarded as, personalized investment advice. Strategies and ideas discussed may not be right for you. Views and opinions expressed may change without notice and do not constitute a recommendation, or an offer or solicitation to buy or sell securities. In addition, Oak Harvest makes no assurance as to the accuracy of any forecast made. Past performance is not indicative of future results. Investing involves the risk of loss.