What’s All the Buzz About Asset Allocation? Is This Really Important to My Retirement?

By

Louis Horkan

Reviewed by Nathan Kattner

When it comes to investing and retirement, there’s all kinds of articles and other content available online that rely on hype, the use of click-bait, and other means to get your attention.

Oftentimes there’s more buzz than there is meat on the bones, making it tough when it comes to discerning what’s important – that which you should absolutely pay attention to and learn more about.

Asset allocation (and diversification) is the real deal – it’s critical when it comes to your retirement.

Introduction

No doubt you’ve heard or read your fill of the “leaving all eggs in one basket” analogy, which is routinely utilized to introduce the concept of diversification. Overly utilized is a better analogy…

Don’t worry, we’re not going there today.

Instead we are going to cut to the chase and explain the concepts of diversification and asset allocation. And focus on how they are closely linked and together a key to successful retirement planning.

Speaking of planning, there is a process involved. The better you understand what that is and what to expect, you’ll be more comfortable participating in the process.

Diversification defined

In the context of investing and retirement, diversification can be defined as spreading your investment dollars around.

Simply stated, don’t buy just one stock. Or bond. Or mutual fund. Or put all your money into one choice ranch property.

And don’t think that buying four or five airline stocks constitutes creating a diversified portfolio. You’ll realize the folly in this belief the next time there’s a “near-air incident,” the likes of which we’ve seen too often as of late. You’ll probably see your “diversified portfolio” collectively punished in the market as the media spends days on end thereafter scaring the public about air travel.

Which brings us back to the issue of why diversification is important to you.

Again, keeping it simple, it’s a strategy that you can use to manage your risk. Rather than concentrate your retirement money into a single asset class, you diversify these dollars by investing across a range of different asset classes.

You use this strategy to attempt to mitigate risk while trying to maximize returns.

Asset allocation defined

When it comes to asset allocation, at a base level this boils down to your portfolio mix. More succinctly stated, the amounts or percentages of your overall available savings and where that is invested across different asset classes.

When it comes to asset allocation, at a base level this boils down to your portfolio mix. More succinctly stated, the amounts or percentages of your overall available savings and where that is invested across different asset classes.

Hmmmmm….

That sounds very similar.

Linked

They sound similar because they are…they’re very much related. Ying and yang, as it were.

Let’s put a finer point on this to provide better clarity.

If you decided to invest all your money into Boeing stock because you work for them and feel you have a good understanding of who they are and what they do, you would have made an investment strategy decision.

In this scenario you would have decided against diversification as an investment strategy, electing instead to roll your dice with a single investment.

And in doing so you would have created an allocation decision of investing what you have into one type of asset – Boeing stock.

Safe to say your investment would definitely be high risk. Obviously, your thought process would have been one in which you saw Boeing shares poised to take off big time and give you a big return. So you wagered that the reward would justify the risk taken.

The word wagered was used on purpose, as this would definitely be more of a bet versus a well-considered investment decision.

And that might have worked for some period. And then Jan. 5, 2024, rolled around and Air Alaska flight 1282 lost a door plug. Who even knew what door plugs were on an airplane? You may or may not have, even though you work for Boeing.

We’re not experts on aviation, but a door flying off a plane mid-flight does seem like a problem…you might even say significant.

Yikes…

What you did quickly learn was the fact this incident spooked the public, as well as the Company’s customers.

And suddenly diversification as a concept came home big time.

Moreover, you probably wished you would have spread your money around a bit.

Even just placing half your money into at least one other company might have saved you some serious losses. Hopefully not another related company, such as an airline or aeronautical manufacturer, who probably also saw a big decline as well at the same time.

Let’s assume you had invested in multiple stocks and a couple other things; you would have incorporated a strategy of diversification. There’s a good chance your attempt to mitigate risk would have paid off, at least to some extent, when compared with the aforementioned “all-in-one” investment approach.

Carrying this forward, in that scenario your asset allocation would be defined by the mix of assets you invested into, and the extent to which you did so. A simple example would be half of your money invested in five stocks (each in different industries), and the rest of your retirement money spread equally between a couple bonds (a U.S. treasury and municipal bond), as well as a CD.

To put a bow on this, spreading your money around, and into what type of assets, and in what dollar amounts, would constitute your asset allocation within a portfolio incorporating a diversification strategy.

Once again, asset allocation and diversification are closely linked and critical when it comes to investing.

Primary consideration

The good news at this point is you’ve probably gained real clarity about the need to diversify. Now you can begin to focus on your primary consideration – your goals in retirement and how best to achieve them.

Key in that endeavor will be growing your collective retirement assets (whatever they might be) in a manner that provides you the best potential for return while limiting your risk to a reasonable level that allows you to sleep at night. A risk/reward scenario with which you are comfortable.

With that addressed, now you can concentrate on the real issue at hand – asset allocation.

Available asset classes

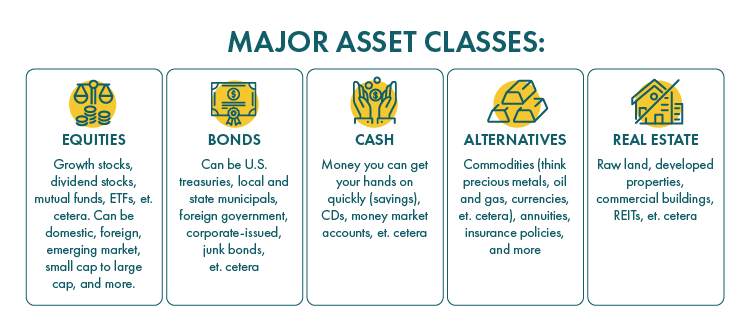

When it comes to what’s available, there are basically five classes of assets: Equities, bonds, cash, alternatives and real estate.

Within each asset class there are an assortment of choices to select from. You can further diversify your portfolio based on where you choose to deploy your retirement dollars within a class, as well as across asset classes.

Major asset classes:

- Equities – growth stocks, dividend stocks, mutual funds, ETFs, et. cetera. Can be domestic, foreign, emerging market, small cap to large cap, and more

- Bonds – can be U.S. treasuries, local and state municipals, foreign government, corporate-issued, junk bonds, et. cetera

- Cash – money you can get your hands on quickly (savings), CDs, money market accounts, et. cetera

- Alternatives – commodities (think precious metals, oil and gas, currencies, et. cetera), annuities, insurance policies, and more

- Real estate – raw land, developed properties, commercial buildings, REITs, et. cetera

RSP process

Okay, so that’s it. Choose an assortment of stocks you happen to like a lot, along with some other types of assets, like bonds, a CD and an annuity (whatever that is), and buy into a property your cousins Vinny and Tito have been pushing on you for years.

There you have it, you’re diversified with an allocation across an assortment of asset classes. You’re all done with creating your retirement portfolio.

Were it so easy…

Whether you’re brand new to investing or you’ve dabbled for years, intuition and/or experience tell you there is a lot more that goes into all of this. You’d be right in your assumption.

Like almost all endeavors in life, there is a plan involved.

In the case of retirement planning, there’s a lot more. Consider the fact that the savings you create will have to sustain you and your family for potentially decades in retirement. This has to be more complicated than following a recipe for brownies.

To get you prepared, you will need a plan that covers all types of important issues. These can range from how to save, what to invest in, how much you’ll be able to spend each month, taxes (there’s a good chance you could potentially owe more than what you pay now), passing on assets to loved ones to ensure their financial security, and more.

At Oak Harvest Financial Group (OHFG), we recognize there is an entire process that goes into proper retirement planning, which is why we created our Retirement Success Plan, or RSP.

Circling back to the topic of investment allocation, the first step in our RSP process is focused on investment allocation. The first meeting we have with you is referred to as the “Allocation” meeting, which is critical to our entire RSP process.

In a nutshell, we use the meeting to determine a number of things. We want to gain a real sense of who you are and what’s important to you. It’s important that we understand the plans you have and your vision for retirement.

A big part of the meeting is determining your comfort level with risk. We do so utilizing a comprehensive questionnaire that helps you to easily convey your fears and comfort level with investing and risk.

We also ask for objective data, including information on your current portfolio, financial statements, tax information, your thoughts on how much you think you wish to spend in retirement, and more.

Another important element in Step 1 is determining whether you are being properly compensated for the risk you are taking – an overall risk/reward assessment. We do this by looking at your portfolio to determine the potential for upside returns versus downside losses.

Between the first and second meeting, our team conducts an analysis of your portfolio. Part of this process involves grading out a key number of metrics, including what we refer to as your risk number and the Grade Point Average (GPA) of your current portfolio.

You can learn more about the Allocation meeting and the many key elements and components involved here.

Beyond the Allocation meeting in Step 1, we move on to the following steps:

- Step 2 – Income planning

- Step 3 – Tax planning

- Step 4 – Healthcare planning

- Step 5 – Estate planning

Comprehensive!

Yes, indeed! As we said before, preparing for retirement involves a plan. Constructing that plan requires a comprehensive approach that is much more entailed than getting out the trusty dartboard to pick some assets where you’ll invest your retirement dollars.

In fact, it involves a process that encompasses consideration of the myriad issues you’ll deal with in preparing for retirement, as well as what you’ll deal with after you retire. A plan that takes guessing out of the equation for you.

Conclusion

If it wasn’t so clear to you before perusing this article, it should now be crystal clear that asset allocation and diversification are REAL IMPORTANT…and absolutely linked – they are ying and yang when it comes to investing and retirement planning.

Beyond understanding what each is, it’s more important to understand their role in creating a portfolio, and even more so in creating a retirement plan.

Having read about our Retirement Success Plan, it should also now be clear that retirement planning involves lots of pieces. There is a process that must be followed in order to ensure all the key issues are covered. Familiarity with our RSP approach should take any fear or trepidation out of the equation and help you fully participate in that process.

Having read about our Retirement Success Plan, it should also now be clear that retirement planning involves lots of pieces. There is a process that must be followed in order to ensure all the key issues are covered. Familiarity with our RSP approach should take any fear or trepidation out of the equation and help you fully participate in that process.

Speaking of planning, if you are currently utilizing a retirement plan (either your own or one created for you), our team would be happy to review it to determine if it is capable of really meeting your goals.

Or we can assist you by creating a retirement plan capable of helping you to retire with confidence. We can build a holistic, comprehensive retirement plan addressing relevant issues, utilizing strategies that cover Social Security, taxes, income, spending, healthcare, legacy, and more, customized to your family’s specific needs.

A plan created with the goal of ensuring you can successfully live out the retirement you envision.

If you are ready to take the next step and talk to a team of retirement planners who can advise on all your retirement needs, and who will put your interests first, Schedule a call today!

Related Content

Asset Class Diversification: Investing’s Only “Free Lunch”

Retirement Planning: Are you Ready for Retirement? with Oak Harvest Retirement Success Plan

What You Can Do With Asset Allocation to Lessen Crippling Taxes and Have More Money in Retirement

Which Assets In Our Retirement Portfolio Should We Spend Down First

Learn about Asset Allocation and Why it’s an important part of Long-Term Investing

Let Us Help You Achieve the Retirement You Deserve!

Investment Advisory services are provided through Oak Harvest Investment Services, LLC a Registered Investment Advisor. Insurance services are provided through Oak Harvest Insurance Services, LLC. Oak Harvest Investment Services, LLC and Oak Harvest Insurance Services, LLC are not affiliated with the U.S. government or any government agency. Information presented is for educational purposes only intended for a broad audience. Not an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies.

“Peace of Mind,” “Safety,” “Principal Protection,” “Lifetime Income, “Guaranteed Income,” or other guarantees are associated with fixed insurance products. No such language refers in any way to investment advice, investment advisory products, securities, or recommendations provided by Oak Harvest Investment Services. Investing involves risk. Rates of return are not guaranteed unless otherwise stated. All guarantees are dependent on the financial strength and claims-paying ability of the issuing insurance company. Annuities have limitations and are not appropriate for all circumstances or individuals. They are not intended to replace emergency funds or to fund short-term savings or income goals. Lifetime income may be available on certain products through an optional rider, at no cost or for an additional cost, depending on the contract. Insurance products are not insured by any federal government agency and may lose value. By contacting us, you may be offered information regarding the purchase of insurance and investment products.

Oak Harvest has a reasonable belief that this marketing does not include any false or material misleading statements or omissions of facts regarding services, investment, or client experience. Oak Harvest has a reasonable belief that the content as a whole will not cause an untrue or misleading implication regarding the adviser’s services, investments, or client experiences. Please refer to www.oakharvestfg.com for additional important disclosures.