Turning Off Social Security: What You Gain and What You Risk

Yes, under certain circumstances, you can stop or “turn off” Social Security benefits after you’ve started receiving them. Depending on your age and how long you’ve been collecting benefits, you may be able to either withdraw your application entirely or voluntarily suspend your payments. For some retirees, this strategy can increase future Social Security income, improve survivor benefits, and create greater flexibility in retirement planning. However, it also comes with important rules, deadlines, and potential drawbacks that should be carefully evaluated before making a decision.

Learn more about Senior Financial Advisor Ed Rossi, CFP®, CTS™, TPCP®, CPWA®, NSSA®, CES™, by clicking here.

Key Takeaways

- Social Security benefits can sometimes be stopped after they have started.

- The Social Security Administration offers two primary options: Withdrawal of Application and Voluntary Suspension.

- Withdrawal of Application is only available within 12 months of claiming benefits and requires repayment of all benefits received.

- Voluntary Suspension is available after reaching Full Retirement Age and can increase future benefits through Delayed Retirement Credits.

- Delaying benefits can increase monthly Social Security income by approximately 8% per year until age 70.

- Suspending benefits may improve future survivor benefits for a spouse.

- Stopping benefits can provide flexibility if you return to work or experience changes in your financial situation.

- Suspending or withdrawing benefits may affect taxes, Medicare premium payments, and family benefits.

- The decision should be evaluated within the context of a comprehensive retirement income plan.

Turning Off Social Security: What You Gain and What You Risk

“What if I told you that you could pause your Social Security checks – and potentially come out ahead for doing it?”

Sounds crazy, right? But it’s true. In the next few minutes, we’re going to explain why hitting the “off” switch on your Social Security after you’ve started might be a smart move for some retirees.

Stick around to learn how it’s even possible (yes, Social Security lets you do this!) and three big reasons it could benefit you. We’ll also cover the risks and rules you need to know – straight from official Social Security and IRS guidelines.

Learn more about Senior Financial Advisor Ed Rossi, CFP®, CTS™, TPCP®, CPWA®, NSSA®, CES™, by clicking here.

Can You Really Turn Off Social Security After You’ve Started?

Yes – under certain conditions, you can stop your Social Security benefits even after starting them.

The Social Security Administration (SSA) provides two main ways to do this:

-

Withdrawal of Application (the “Do-Over”)

-

Voluntary Suspension (the “Pause Button”)

Let’s break down both options clearly.

1. Withdrawal of Application (the “Do-Over”)

If you recently started your retirement benefits and have second thoughts, you may be able to withdraw your Social Security application.

-

This option is available only within 12 months of when you first became entitled to benefits, and you can do it only once in your lifetime.

-

You’re essentially telling SSA: “Let’s pretend I never started taking benefits.”

-

However, there’s a catch — you must repay all the benefits you’ve received so far if your withdrawal is approved.

-

This includes any money paid to you or your family members on your record, as well as amounts withheld for Medicare premiums or taxes.

-

Once that’s done, your Social Security record resets as if you never claimed, allowing you to reapply later for a higher benefit.

(Visual cue: Imagine hitting a “reset” button on your benefits.)

Social Security Decisions

Navigate your Social Security decisions with confidence using our

comprehensive report, offering expert insights and personalized guidance

to help you make informed choices tailored to your retirement goals and

financial situation.

2. Voluntary Suspension (the “Pause Button”)

If it’s been more than 12 months since you started benefits — or you don’t want to repay past benefits — there’s another route.

Once you reach your Full Retirement Age (FRA) (around 66–67 for most retirees), you can ask the SSA to suspend your retirement benefit payments.

-

This means you temporarily pause your monthly checks.

-

While your benefits are suspended, you earn Delayed Retirement Credits — roughly ⅔ of 1% per month, or about 8% per year beyond your FRA.

-

When you resume Social Security later, your checks will be larger.

-

You can voluntarily suspend anytime between your FRA and age 70.

-

No repayments are required; your benefits will automatically restart at age 70 unless you resume them earlier.

(Visual cue: Show a timeline from full retirement age to 70 with an upward arrow indicating growth in benefit amount.)

Important Details:

-

Voluntary suspension can’t begin until you reach FRA.

-

If you’re younger (e.g., 64) and regret claiming early, you must wait until FRA to suspend — or consider the withdrawal option if within 12 months of starting.

-

When you suspend your benefit, anyone receiving benefits on your work record (spouse, dependent) will have their payments paused as well — except a divorced spouse.

-

You cannot earn delayed credits past age 70; there’s no advantage to suspending beyond that age.

Three Big Benefits of Suspending or Withdrawing Your Social Security

Why would anyone give up months or even years of payments? Here are three well-reasoned benefits.

1. Larger Monthly Checks for Life

The main incentive is to receive bigger Social Security checks down the road.

-

By suspending payments after FRA, you earn roughly an 8% annual boost for each year you delay.

-

Example: If your FRA benefit at 67 is $1,500/month, delaying until 70 increases it to about $1,860/month — a 24% lifetime increase.

-

Even if you claimed early, suspending at FRA can help recoup some of that reduction.

In short, pausing now can mean more income later, especially if you anticipate living into your 80s or 90s.

(Think of it as “investing” your Social Security by not taking it for a while — the payoff is a higher payout later.)

2. Flexibility if Your Situation Changes (Avoiding Penalties & Taxes)

Life doesn’t always go as planned. You might start Social Security and then decide to go back to work — or realize you don’t need the income right now.

Turning off benefits gives you a valuable do-over.

-

If you claim early and then return to work, the Earnings Test may withhold part of your benefits.

-

Pausing can also help optimize your tax situation. Up to 85% of Social Security benefits can be taxable depending on your income.

-

If you have significant other income, suspending your benefit might keep you in a lower tax bracket or reduce how much of your benefit is taxed.

Example:

Jane retired at 62 and started Social Security. A year later, she began consulting part-time, which increased her income and reduced her benefits due to the earnings limit.

She decided to withdraw her Social Security application after 10 months, repaid what she’d received, and stopped her checks.

This allowed her to work penalty-free and reduce her tax burden. Jane plans to reapply at 66, when she fully retires, locking in a higher benefit — with no earnings penalties.

(Visual cue: Show a scale balancing “Work Income” on one side and “Social Security” on the other.)

Tax Note: If you repay benefits, the IRS allows a deduction or credit for the repaid amount, so you aren’t taxed on money you gave back. Always consult a qualified tax professional.

Click to see all the latest retirement videos for your Social Security research.

3. Maximizing Survivor Benefits for Your Spouse

If you’re married, pausing your benefit can increase your spouse’s survivor benefit in the future.

-

Survivor benefits are based on what you were receiving (or eligible to receive) at death.

-

By delaying, you increase both your benefit and your spouse’s potential survivor benefit.

-

Example: A higher-earning husband who delays by 2.5 years may raise his wife’s survivor benefit by about 20%.

-

Waiting until age 70 includes all delayed credits — meaning the surviving spouse inherits that larger amount.

(Think of this as a form of protection — ensuring your spouse isn’t left with a smaller Social Security check later.)

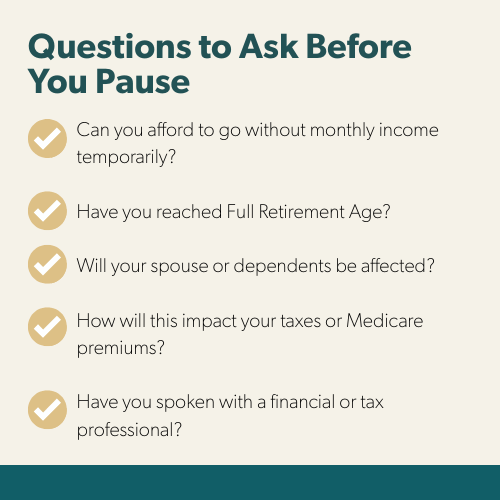

Potential Drawbacks and Considerations

Turning off benefits isn’t always the right move. Here are important risks and trade-offs:

-

No Income During Pause: You’ll need other income (savings, pension, part-time work) to cover expenses.

-

12-Month Limit on Withdrawals: You can only withdraw your application once, and only within 12 months of starting.

-

Repayment Requirement: Withdrawing requires repaying gross benefits received — including withheld taxes or Medicare premiums.

-

Longevity Risk: If you don’t live long enough, the higher payments later may not outweigh the payments you skipped early on.

-

Impact on Dependents: Spousal or child benefits on your record are also suspended during your pause.

-

Medicare Considerations: If your Part B premiums are deducted from your Social Security, you’ll need to pay them directly while suspended.

-

No More “File and Suspend” Loopholes: Under current law, suspending your benefit also pauses any benefits payable on your record.

Conclusion – Making an Informed Choice

Turning off your Social Security after starting is a big decision. It’s not for everyone, but in the right situation, it can be a powerful tool.

The Upsides:

-

Larger lifetime benefit potential

-

Flexibility if your income changes

-

Higher survivor benefits for a spouse

The Downsides:

-

Loss of current income

-

Repayment or timing limits

-

Possible impact on family benefits and Medicare billing

Ultimately, ask yourself:

“Does pausing my Social Security now improve my overall retirement security?”

This depends on your finances, health, and marital situation. Always consult the SSA directly or a qualified financial planner before taking action.

For official resources:

Visit SSA.gov or call 1-800-772-1213.

You do have options if you started Social Security and later regret it or your circumstances changed. Suspending or withdrawing can, in the right case, provide greater flexibility and income later in retirement — but it comes with trade-offs.

Stay informed, plan smart, and make decisions based on your goals and situation.

Thank you for watching! If you found this information helpful, please give it a thumbs up and consider sharing it with others who might be wondering about Social Security do-overs. Remember, retirement planning is not one-size-fits-all. Stay informed, plan smart, and here’s to making the best decision for your retirement. Take care!

➡️ Do you need a Retirement Success Plan that goes beyond allocating funds to truly fit your needs? We can help you create a retirement life plan customized for your retirement vision and legacy. Call us at (877) 404-0177 or fill out this form for a free consultation.

Frequently Asked Questions About Stopping Social Security Benefits

Can I stop Social Security after I start collecting?

Yes. Depending on your circumstances, you may qualify for either a Withdrawal of Application or Voluntary Suspension through the Social Security Administration.

What is the difference between withdrawing and suspending Social Security?

A withdrawal essentially cancels your original claim and requires repayment of benefits received. A suspension pauses future payments while allowing delayed retirement credits to accumulate.

Can I suspend Social Security before Full Retirement Age?

No. Voluntary Suspension is only available once you reach Full Retirement Age.

Does suspending Social Security increase future benefits?

Yes. Delayed Retirement Credits can increase your benefit by approximately 8% annually between Full Retirement Age and age 70.

Does stopping Social Security affect my spouse’s benefits?

Potentially. Benefits paid on your record may also be suspended, although divorced spouse benefits are generally not affected.

Can I suspend Social Security after age 70?

No. Delayed Retirement Credits stop accumulating at age 70, so there is generally no benefit to suspending beyond that age.