Weekend Update, November 18th, 2024

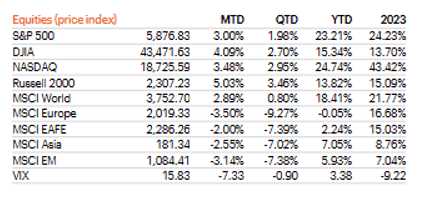

Index, Sector & Asset Performance

US stocks gave up about half their initial 2024 post-election rally last week. Excuses ranged from a stronger dollar to higher interest rates, a more hawkish Federal Reserve, concerns over Trump appointments to Health and Human Services, a newly created DOGE department to cut federal spending, and lower tech earnings in the semiconductor industry. FWIW, the same weakness occurred into November option expiration in 2016 posts the markets initial Trump election week surge. The S&P 500 ended the week down – 2.05%.

Year to date returns from FS Investments:

Only three sectors were positive last week. The top group last week was Financials, gaining +1.4%. Individual stock returns included Charles Schwab (+9.1%) and Wells Fargo (+6.1%).

Health Care stocks got trounced last week dropping -5.6%. Health Care is now the worst-performing sector year-to-date, with a gain of +4%. Vaccine manufacturers plummeted because of uncertainty surrounding healthcare policies in the upcoming administration transition.

Technology stocks fell -3.6% last week. Monolithic Power Systems fell almost -25% on the talk of an NVDA socket loss and Super Micro Computer fell another -24% as their delisting deadline approached.

Fixed income markets sold off last week on the interpretation that the Fed might move more slowly in cutting rates for the rest of 2024 and in early 2025. The 10-year Treasury yield tried to hit 4.50% on Friday but closed at 4.45% on the week, up +15 bps. Fed Chairmen Powell said there was no hurry to accelerate rate cuts given the state of the economy. Fed Fund Futures, which are not predictive, moved market expectations of a 25bps rate cut on December 18 to 60% from around 80%.

Economic Indicators and Earnings Commentary

CPI in line in October, rising +0.2% m/m but up 0.3% excluding food and energy, or +3.3% y/y. Over 60% over the current CPI gain is rent/housing related which is lagging versus market rates. Even that CPI component is being held up by higher mortgage rates, not by end market pricing. Retail sales were mixed. Initial jobless claims remained low at 217,000, pointing to a low layoffs.

Applied Materials underwhelming 3q24 earnings report on tough China comps and a subdued 2025 outlook, dragged the SOX index and many tech stocks lower.

Global Market Trends/Commodities/Currencies

Bitcoin continued its ascent on global easing and speculative trading around Trump 2.0 buying it as a reserve. Here is an overlay of Bitcoin in 2016-17 versus 2024. You must squint hard.

Oil finished at $70/bbl again. Energy stocks were underperformers under Trump 1.0 as more drilling led to lower energy prices. Higher U.S. oil production and tariffs would be a negative for prices. Good for consumers, generally bad for investing in energy equities.

Gold pulled back on a stronger dollar, declining for its 3rd straight week ending under $2600.

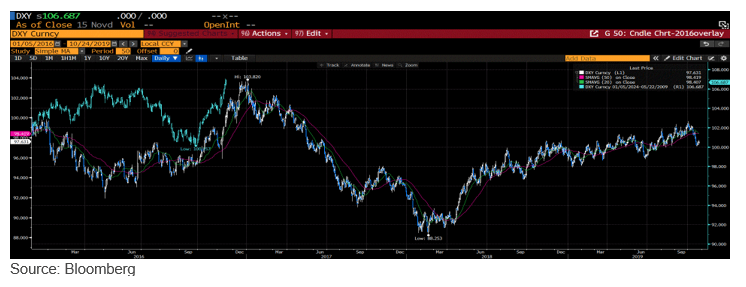

“De-dollarization”? Not so fast dollar Doomers. The dollar continued to rally during the week ending up 1.5%. The DXY index is up over +3% post-election. That said, the near EXACT same move occurred in 4q2016 during the first Trump win, with the dollar peaking spot-on year end 2016 and declining in 2017. Here’s the DXY path in 2016-2017 overlaid on 2024.

Oak Harvest Weekly Stock Talk: Trump 2.0: History Repeats?