Weekend Update, June 24th, 2024

Index, Sector & Asset Performance

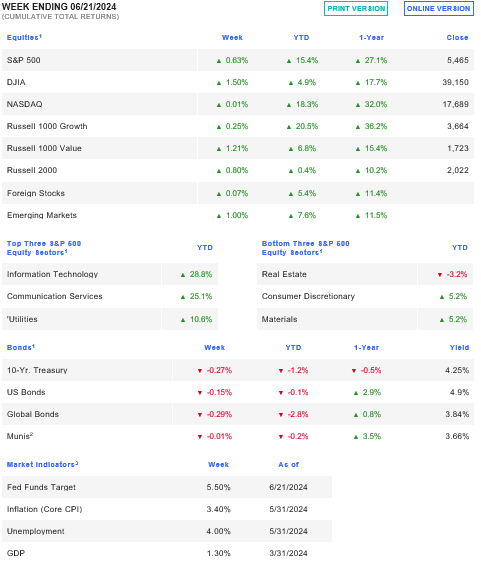

The S&P 500 reached its 31st all-time high for 2024 crossing the 5500 level before reversing lower. Post the Wednesday market holiday, the S&P 500 opened Thursday’s higher and then faded to form what many technicians will see as a short-term exhaustion gap. This was accompanied by a big reversal in the best performing S&P 500 stock year to date, Nvidia (NVDA). On Friday, Nvidia shares declined another -3.2%. Nonetheless, Nvidia is still up +155% year to date, and it briefly became the most valuable public company in the world last Tuesday.

The cash S&P 500 index hit an intraday record of 5,505.53 early last week, registering a +0.6% gain on the week. The 2024 market leading Nasdaq finished the week flat, but the Dow index rose 1.45% for its best weekly performance since May.

Economic Indicators and Earnings Commentary

Earnings this week include Micron Semi (MU), as well as CCL, GIS, FDX, LEVI, NKE, and PAYX.

The week’s key economic data is Friday’s personal spending report. Retail sales have been softening since January. Consumer spending, over 70% of the USA economy, looks to have remained slow and could be under 2% quarterly rate in over a year. The Fed should be on track to cut rates for the first time in over four years in September if not July is the data continues to weaken as our team expects.

Thursday’s data includes lumpy durable goods orders. Durable goods orders likely fell in May with weak aircraft bookings and a strong dollar. Excluding aircraft, nondefense capital goods orders likely rose modestly.

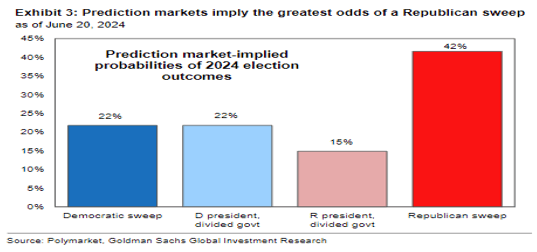

Thursday night brings the first debate for the coming November presidential election. Prediction markets assign a 42% probability to a Republican sweep. The policy outcomes from the election will likely impact the dollar and the relative performance of equities with domestic vs. foreign sales.

Global Market Trends/Commodities/Currencies

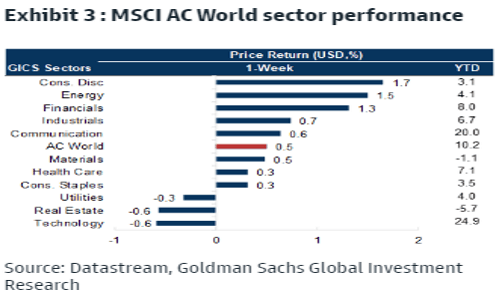

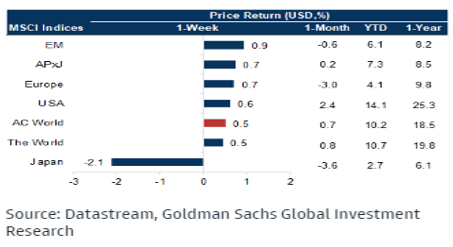

Global equity markets were mixed last week, with France bouncing (+1.7%) and the price weighted, value biased Dow (+1.5%) leading the world indexes higher. Japanese equities fell again.

Oil prices rose last week as increased worries of tensions in the Middle East and declining stockpiles in the US. WTI and Brent crude finished the week higher at $80.73 and $85.24/bbl, respectively, as US crude oil inventories declined by more than consensus had anticipated. Gold fell last week to 2331.20/troy oz on the back of a stronger dollar and pushed out Fed rate cut bets.

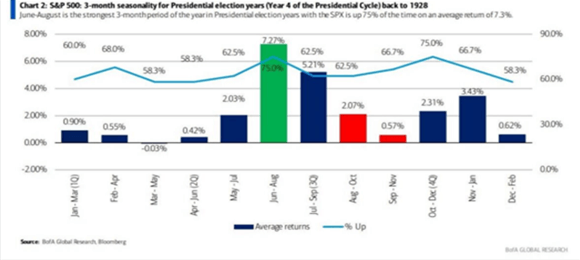

OHFG Exclusive Data & Charts: Summer Rallies are the Norm, even during election years, however, remember investors, risk is assessed up-front, before actions are taken, not after the results are in:

Here is a table on what historical total return an investor earned during a 3-month holding window in the 4th year of a Presidential election cycle. It also shows historic odds of a positive total return for every 3-month period. For example, an investor buys in May and sells at the end of July. This table says that historically, 62.5% of the time, an investor made a positive 3-month holding period return and their average return was 2.03%, between May and July in the 4th year of a Presidential cycle.

Oak Harvest Weekly Stock Talk: 2024 Summer Stock Markets – When Things Get “Real”ly “Interest”ing