Weekend Update, January 6th, 2025

Index, Sector & Asset Performance

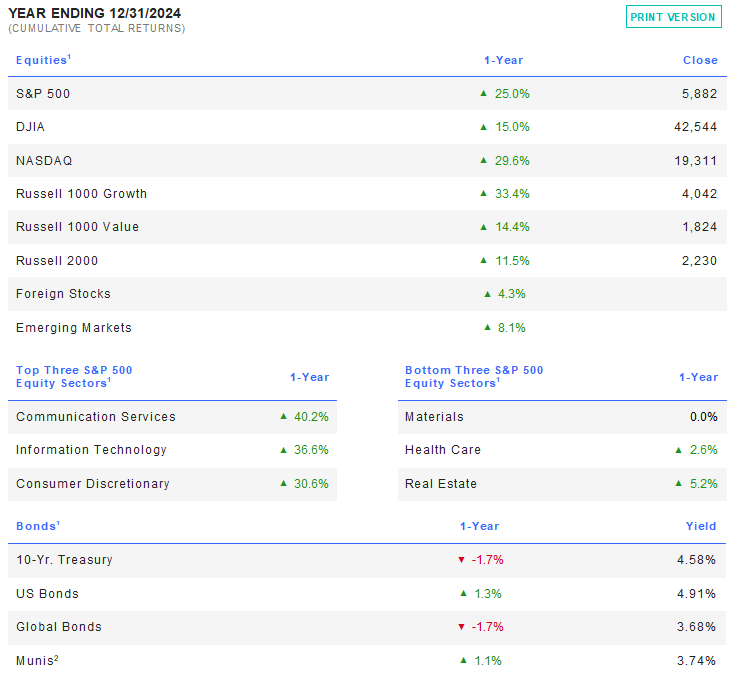

While stocks declined 3 of the last 4 weeks of 2024, the S&P500 ended 2024 posting its second straight +25% annual gain including dividends for the first time since the 1995-2000 period. The Mag 7 (now the Mag 8 with Broadcom) gained almost +50% and drove almost half of the index return after accounting for +60% of S&P500 performance in 2023.

Equity indices (DJIA, S&P 500, NASDAQ Composite) were down -0.5% to -0.6%, with interest rates up about 4 bps. Even so, the S&P500 ended the weekly strongly on Friday up 1.25% (74 points) on the day ending at 5942, however the “Santa Claus rally” technically ended about 35 points short of successful. This morning’s 74 point, 1.25% gains are adding to last week’s late rally.

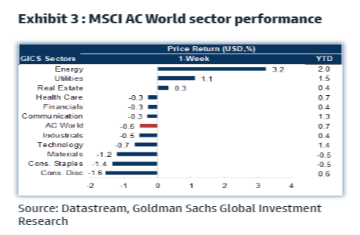

Sector performance last week per Goldman Sachs:

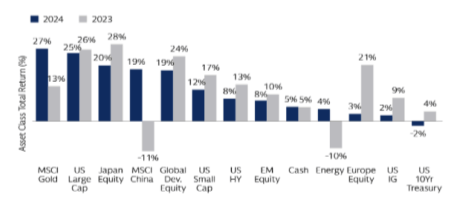

Per Goldman Sachs, 2024 asset class returns:

Interest rates were volatile in 2024, but the trend was to a normal yield curve. The 10-year Treasury yield hit a low of 3.62% midyear before finishing at 4.56%. The 2-year yield finished the year where it began, at nearly 4.25%. The Fed reduced its policy rate by -100 bps throughout the 2h24 but rate cut expectations for 2025 were pared back on a stronger economy.

Economic Indicators and Earnings Commentary

The US economy once again averted a much-predicted recession in 2024. The U.S. economy beat economist expectations for a second consecutive year. GDP growth will end around +3% for 2024 compared to an initial consensus estimate of +1.3%.

Progress on inflation slowed as the core PCE rose +2.8% y/y. This number should fall in early 2025 due to base effects and the seasonal nature of inflation in the US.

The S&P500 begins the year with a forward P/E ratio slightly over 21.5x, near its historically higher end of valuation. Reminder, valuation is historically a horrible market timing tool and as much as its discussed by economists and academics, the OHFG investment team knows no professional money manager using the Schiller index as a stock timing tool.

The ISM services index will be released on Tuesday and followed by Friday’s employment report. The minutes from the December FOMC meeting will be released on Wednesday.

Global Market Trends/Commodities/Currencies

The U.S. bested international stock markets again in 2024. Global equities rose barely 5.5% in dollar terms, growth stocks dominated value stocks, and large cap stocks beat small caps once again.

The price of a barrel of oil rose to nearly $74 last week and hit its highest level since December 19. All told, oil prices ended the year where they started, and energy stocks broadly lagged the overall markets. Lately, natural gas is leading energy commodities higher on the back of cold weather in the USA and demand from Europe post Russian pipeline shutdown.

Bitcoin rallied late in the week back above $95k.

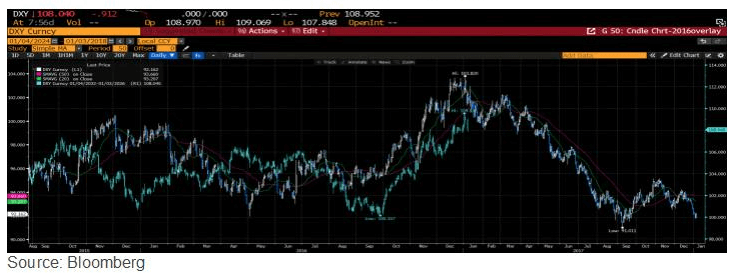

The US Dollar is the “chart of 2025” that bears watching. Most believe it will continue to strengthen in 2025 on “US Exceptionalism”. The breath of the US and international stock markets would be better served with a peaking in the US dollar in the 1h25 and a slow and gentle decline, per what transpired in 2017 under the first Trump presidency. You can follow along then versus now.

Oak Harvest Weekly Stock Talk

2025-1ST Half 2025 Outlook, Quick Hits

Past performance is no guarantee of future results. Indexes are unmanaged and one cannot invest directly in an index. They do not reflect any fees, expenses or sales charges.