Weekend Update, May 18th, 2026

Friday Interest Rate Shock, Oil, and AI

Key Takeaways Last Week

U.S. stocks were mixed for the week as Friday’s interest rate driven selloff erased most earlier gains. The S&P 500 rose +0.1%, the Dow fell -0.2%, the Nasdaq fell -0.1%, and the Russell 2000 fell -2.4%. Year to date, the S&P 500 is up +8.2%, Dow +3.0%, Nasdaq +12.8%, and Russell 2000 +12.5%.

- Stocks fell Friday as yields overseas spiked, oil prices rose, and Treasury yields jumped as investors were disappointed with the US/China trade summit and European political elections are rattling markets.

- The 30-year Treasury yield reached its highest closing level since 2007.

- April CPI rose 3.8% year over year, with energy driving a large part of the increase.

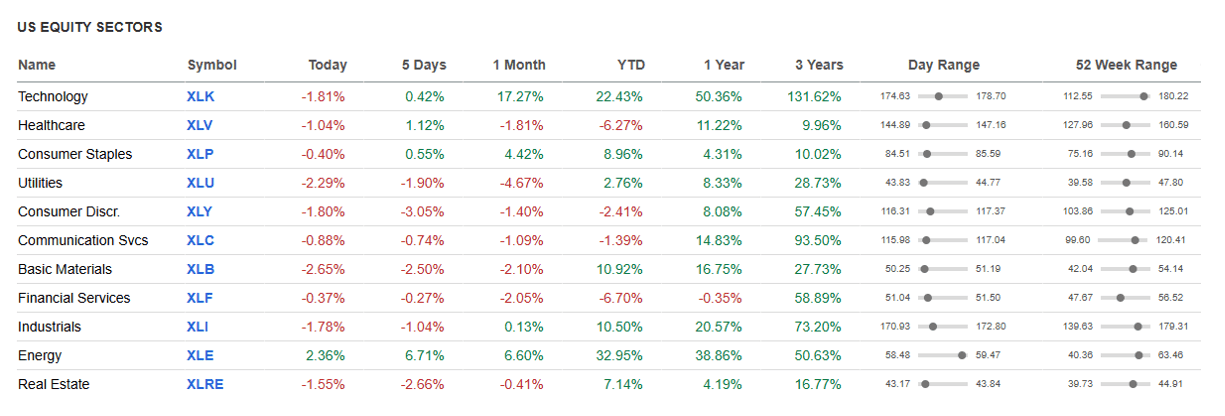

- Energy was the strongest sector, rising about +6% for the week.

- AI and semiconductor stocks pulled back late in the week after a strong rally.

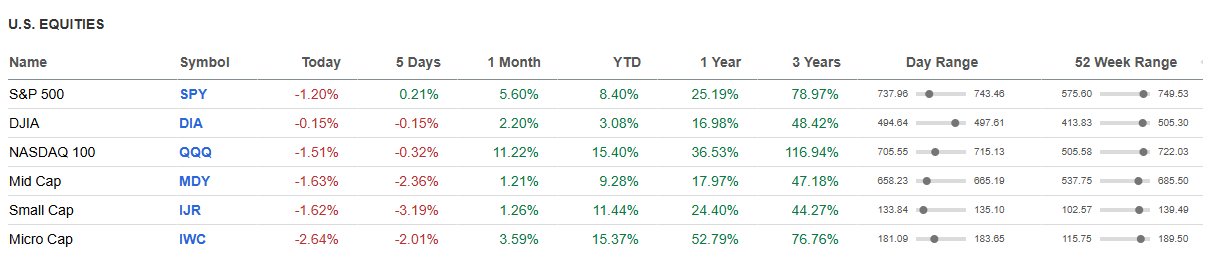

U.S. Stock Performance – Index and Sector Moves

Financial markets were mixed during the week ending 5/15/26. Data Seeking Alpha.

The S&P 500 finished at 7,408, the Dow at 49,526, the Nasdaq at 26,225, and the Russell 2000 at 2,793.

Sector leadership shifted toward energy, while semiconductors and high-growth technology weakened late in the week as investors reacted to higher yields and rising oil.

AI Capex

The current AI/semiconductor rally continues to draw comparisons to the Dot.com period from October 1998 to March 2000, when semiconductor and networking stocks dramatically outperformed during the internet infrastructure buildout. The similarity today is narrow leadership and powerful semiconductor momentum; the key difference is that today’s leading AI companies generally have stronger earnings and cash flow.

S&P 500 Weekly Leaders and Laggards Ranked

Top Performers (WTD / best available data):

- Akamai Technologies (AKAM) – AI infrastructure contract and earnings momentum.

- Datadog (DDOG) – Rallied after Q1 revenue exceeded expectations and 2026 guidance.

- Micron (MU) – AI memory demand and strong high-bandwidth memory pricing.

- Fortinet (FTNT) – Rose after strong Q1 results and higher 2026 guidance.

- Energy leaders / XLE components – Energy outperformed as oil rose.

Bottom Performers (WTD):

- Intel (INTC), -16.9% – Investors reassessed the AI chip trade and Intel’s position.

- Moderna (MRNA), -15.5% – Reversed after earlier vaccine-related gains.

- Constellation Energy (CEG), -15.1% – Fell after guidance, higher debt/cost worries.

- Charles River Labs (CRL), -14.8% – Continued pressure in China.

- Albemarle (ALB), -14.2% – Lithium weakness and write down/oversupply concerns.

Breadth & Participation

Market breadth weakened despite the S&P 500’s seventh straight weekly gain. New lows on the NYSE outpaced new highs, and breadth indicators turned down late in the week.

The equal-weight S&P 500 continued to lag the cap-weighted index. Leadership remains concentrated in AI, semiconductors, and select mega-cap growth names.

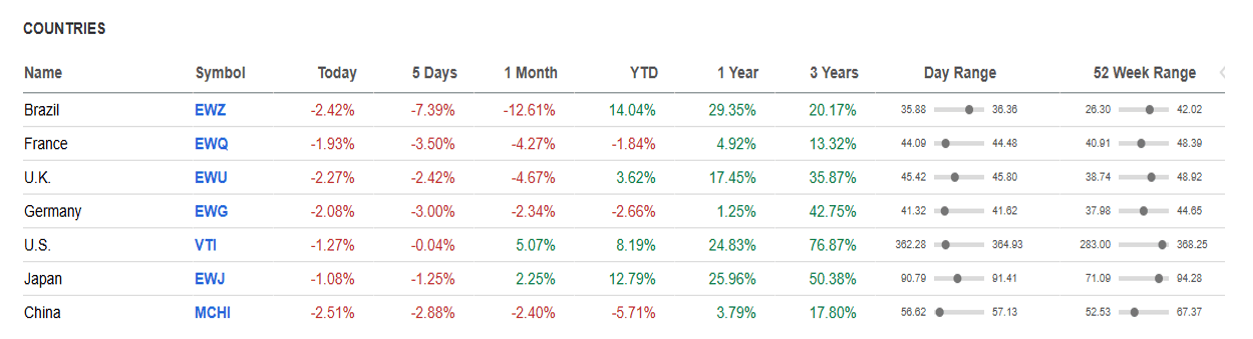

International/Global

Emerging markets and slow growth economies got rocked Friday by a stronger dollar and rising interest rates. Yields in Japan and Europe broke out to major new high yields pressuring all financial assets ex oil and energy stocks. Brazil and Germany were the worst markets, the US the best.

International markets weakened as rising oil, higher yields, and little progress from the Trump-Xi summit weighed on sentiment. The summit produced few breakthroughs, while U.S.- Iran related uncertainty remained important global risks.

Volatility & Risk Sentiment

Risk sentiment deteriorated late in the week. The VIX closed at 18.43, a modest rise.

MOVE/Bond Index: 79.87, exploded higher Friday on higher yields, causing forced deleveraging and collateral damage.

Bonds, Credit & Interest Rates

Treasury yields rose sharply. The 2-year Treasury yield ended at 4.09%, and the 10-year ended near 4.59%, both the highest since February 2025. 30-year Treasury yield hit 5.13%, highest closing level since July 2007.

Credit conditions remain stable, but higher rates are tightening financial conditions.

Economic Data, Monetary Policy & Earnings

April CPI rose 0.6% month over month and 3.8% year over year. Energy rose 3.8% in April and accounted for over 40% of the monthly increase. April PPI rose 1.4%, the largest monthly increase since March 2022.

FactSet reported Q1 S&P 500 blended earnings growth of 27.7%, with revenue growth of 11.4%, the strongest since 2022 if sustained.

Consumer Stress Commentary

Consumer pressure increased as higher gasoline prices weighed on discretionary spending. April retail sales rose 0.5%, but growth slowed from March, and excluding gas stations retail growth slowed to 0.3%.

Gasoline prices reached about $4.53/gallon, up $1.35 from a year earlier. Credit-card delinquencies are rising. Retail traffic rose 2.6% year over year in April, but higher gas prices distorted nominal sales growth.

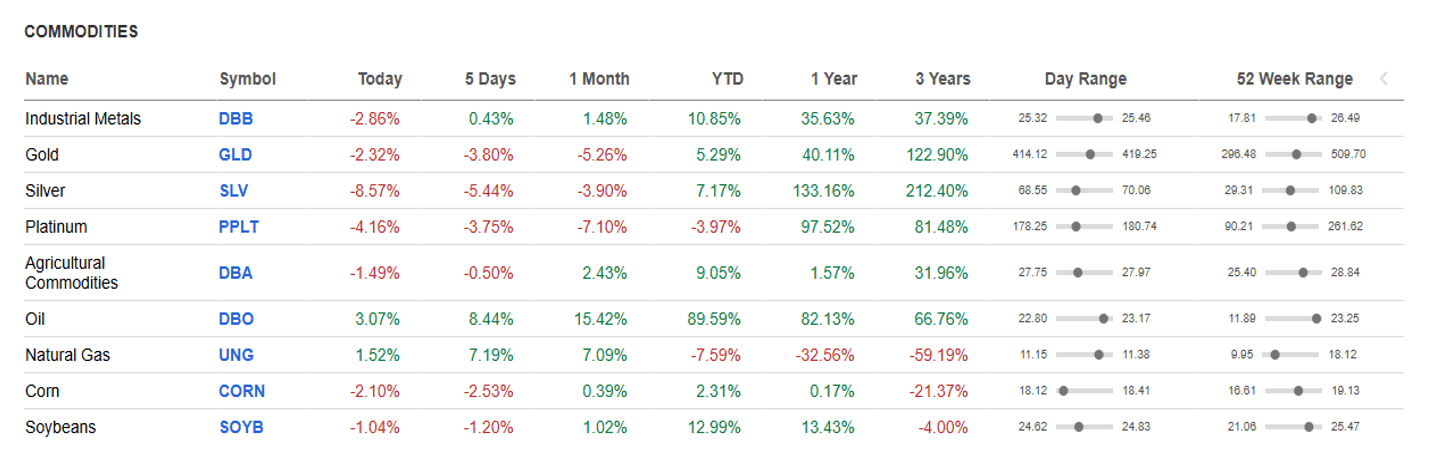

Commodities, Currencies & Macro Assets

Commodities hate days like Friday, stronger dollars and higher interest rates. Both raise the carrying costs of idle inventory for most companies.

Oil surged on Friday post the China summit as no additional help was offered and Strait of Hormuz risk and Iran tensions continue pressing inflation higher. WTI crude traded near $105/bbl Friday.

Gold: fell -$150/oz Friday on a stronger Dollar

Dollar Index: rose against all currencies Friday

Bitcoin: fell -$3000 on Friday on risk off

Ethereum: fell -$100 on Friday

Liquidity Conditions

Equity liquidity remained supportive for large-cap leaders but weakened at the end of the week on the global spike in interest rates hurting small caps and speculative growth. Treasury and global bond liquidity appeared fragile as long-end yields surged.

Flows & Positioning

Positioning remains crowded in AI, semiconductors, memory, cloud infrastructure, and mega-cap technology. Friday’s pullback showed that leadership can reverse quickly when yields and oil rise together.

What Matters This Week

Markets will focus on:

- Nvidia earnings and AI capex commentary

- Walmart, Home Depot, and consumer earnings

- Fed minutes and rate-hike expectations

- Oil prices and Strait of Hormuz developments

- Whether breadth improves or mega-cap leadership narrows further

Bottom Line

Markets held onto a small weekly gain for the S&P 500, but the tone worsened on Friday, option expiration day. Rising oil, inflation data, and higher Treasury yields pressured equities, especially AI and semiconductor leaders. Energy benefited from geopolitical risk, but higher oil also raises inflation and consumer-stress concerns. Until yields and oil stabilize, markets may remain vulnerable to sharper rotations beneath the surface.

Stock Talk

Stagflation Nations: What, Where, Why, and How it could affect your investments

AI remains the dominant earnings story, but the market is beginning to test whether growth stocks and the economy can withstand higher yields, rising oil, and more inflation-sensitive Fed expectations.

Past performance is no guarantee of future results. Indexes are unmanaged and one cannot invest directly in an index. They do not reflect any fees, expenses or sales charges. The preceding discussion is for informational purposes only. Investing involves risk and no reference to any security listed above should be considered a buy or sell recommendation. Advisory services are provided through Oak Harvest Investment Services, LLC, a registered investment adviser.