Weekend Update, June 8th, 2026

Streak Ends

Key Takeaways Last Week

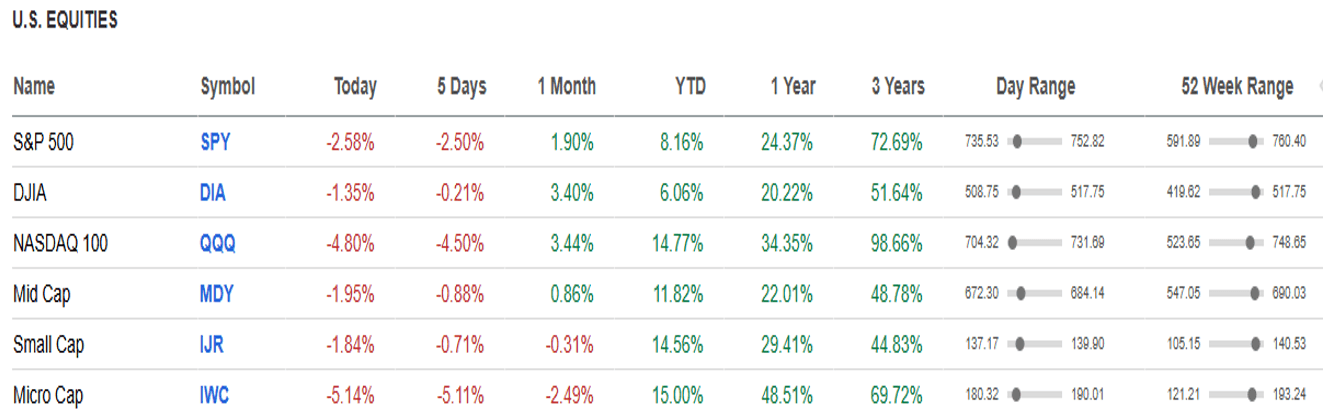

U.S. equities snapped their streak: the S&P 500 fell –2.6% for the week, its first losing week in 10; the Nasdaq dropped –4.7%, the Russell 2000 –2.9%, and the Dow only –0.3%. Friday did most of the damage after a sharp tech selloff on a deleveraging Friday summer trade.

- Interest rates jumped after May payrolls beat expectations. The BLS reported 172,000 jobs added, unemployment steady at 4.3%, and March/April payrolls revised up by 93,000 combined.

- The higher interest rates move hit long-duration stocks hardest with the 10-year Treasury yield rising to about 4.54% and the 2-year to 4.16%, while tech favorites and commodity stocks sold off.

- Oil remained volatile. Oil fell Friday on hopes of U.S.-Iran de-escalation, but Brent and WTI were still set for their first weekly gains in three weeks.

- Gold fell more than -2% Friday as higher real interest rates hurt all commodities, and bitcoin briefly dipped below $60,000 before recovering around $61,000.

May payrolls rose to 172,000, well above expectations, while unemployment held at 4.3%.

The Nasdaq dropped 4.2% Friday, its worst day in over a year.

Semiconductors, AI, and commodity stocks led the selloff after Broadcom failed to exceed expectations.

U.S. Stock Performance – Index and Sector Moves

Financial markets weakened during the week ending 6/5/26.

The S&P 500 closed at 7,383, the Dow at 50,866, the Nasdaq at 25,709, and Russell 2000 at 2,833. Weekly performance was S&P 500 -2.6%, Dow -0.3%, Nasdaq -4.7%, Russell 2000 -2.9%.

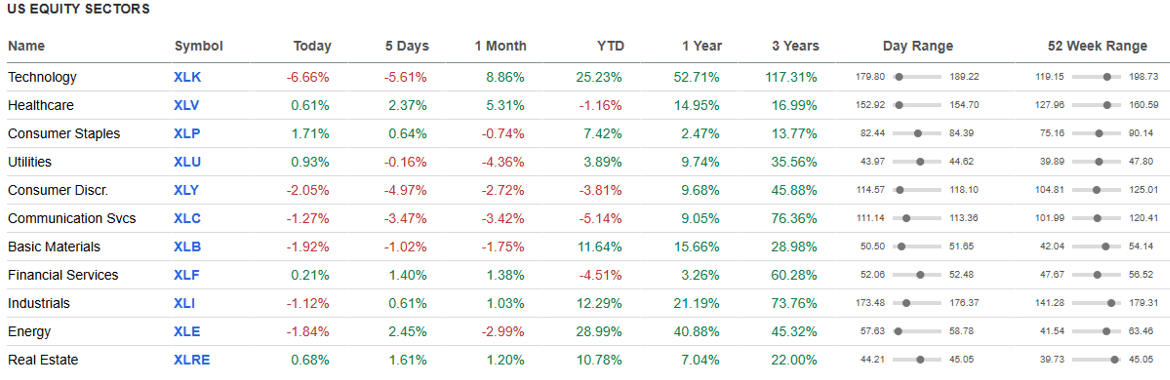

Sector leadership rotated away from technology and semiconductors toward health care, financials, real estate, and consumer staples. Technology and AI leadership weakened as higher yields increased pressure on long-duration growth stocks.

Source: Seeking Alpha

Sector leadership rotated away from technology and semiconductors toward health care, financials, real estate, and consumer staples. Technology and AI leadership weakened as higher yields increased pressure on long-duration growth stocks.

Source: Seeking Alpha

S&P 500 Weekly Leaders and Laggards Ranked

Top Performers (WTD):

- Hewlett Packard Enterprise (HPE), +11.4% – Benefited from AI infrastructure and enterprise hardware rotation.

- Old Dominion Freight Line (ODFL), +10.7% – Rebounded with transport/cyclical rotation and relief from lower oil.

- Cooper Companies (COO), +10.7% – Healthcare/medical-device strength as investors rotated defensive growth.

- Medtronic (MDT), +10.4% – Health-care leadership and defensive rotation helped shares.

- Humana (HUM), +9.9% – Healthcare rebound and managed-care rotation supported gains.

Bottom Performers (WTD):

- ServiceNow (NOW), -13.2% – Software/AI valuation pressure as yields rose.

- Carvana (CVNA), -12.0% – High-beta consumer/growth stock hit by rate concerns.

- Palantir (PLTR), -11.1% – AI momentum unwind and profit-taking.

- Global Payments (GPN), -10.4% – Fintech/payment weakness amid growth-stock selloff.

- Chipotle (CMG), -10.2% – Consumer discretionary pressure and valuation reset.

Breadth & Participation

Source: Seeking Alpha

Breadth weakened materially. Roughly two-thirds of NYSE stocks were down during Friday’s selloff, while the Nasdaq and semiconductor complex absorbed the largest damage.

The equal-weight market held up better than mega-cap tech, but leadership remained narrow and rotation was more defensive than expansionary.

International/Global

International markets were pressured by the U.S. rate move and global technology weakness.

Source: Seeking Alpha

Volatility & Risk Sentiment

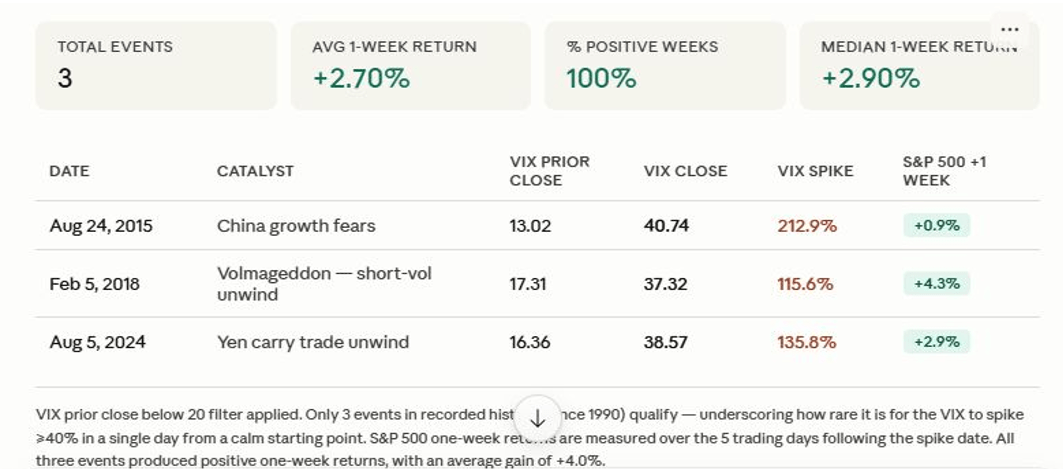

Risk sentiment deteriorated sharply Friday as rate-hike fears returned. The VIX Index rose over 40% on Friday. Historically, that is not the sign of the beginning of something but usually the end of something. Data from John Knott, over the last 35 years, there have only been 3 other times that the VIX has popped 40% or more in one day when starting below 20. The results are below.

Source: John Knott

VIX: 21.57

MOVE Index:75.2

Bonds, Credit & Interest Rates

Treasury yields rose after the jobs report. The 2-year yield settled near 4.160%, while the 10-year rose to 4.537%. The 30-year Treasury was near 5.01%. Credit conditions remained orderly, but higher yields tightened financial conditions for growth equities.

Economic Data, Monetary Policy & Earnings

The May jobs report was the key event. Payrolls increased 172,000, unemployment held at 4.3%, and prior months were revised higher, reducing the odds of near-term Fed cuts. Behind the scenes, the jobs data shows less strength as all the jobs were “part-time” and full-time jobs shrunk. https://www.zerohedge.com/markets/us-jobs-soar-172k-may-smashing-estimates-4-sigma-beat-unemployment-rate-remains-43

FactSet estimated Q2 S&P 500 earnings growth at 21.7%, which would mark a second straight quarter of earnings growth above 20% if achieved.

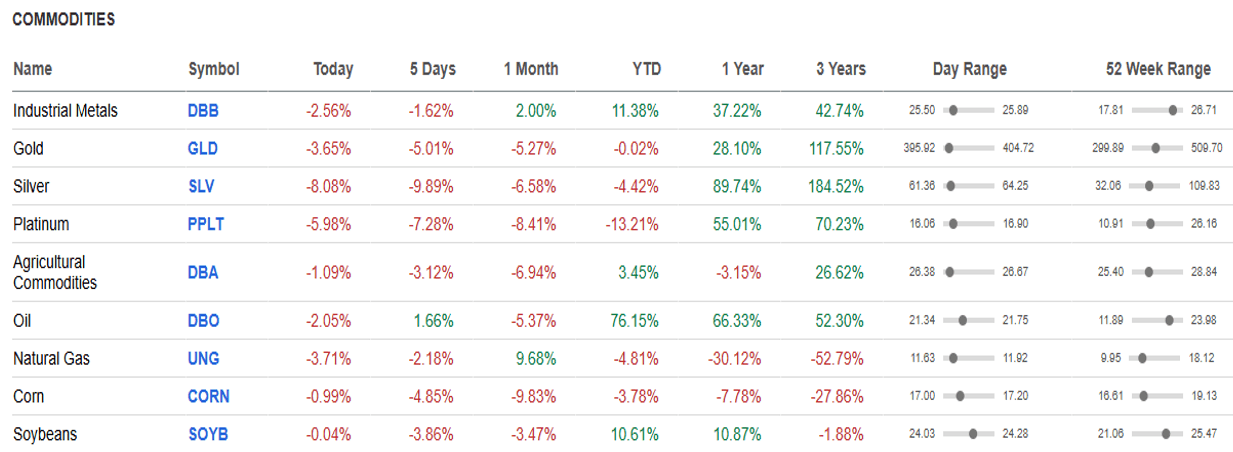

Commodities, Currencies & Macro Assets

Brent crude: ~$93.09/bbl

Gold: $4350

Dollar Index: 100.3

Bitcoin: ~$61,731

Ethereum: ~$1,628

Source: Seeking Alpha

Flows & Positioning

Positioning unwound sharply in crowded AI, software, and semiconductor trades. Money rotated toward health care, financials, real estate, and staples. The Fed’s balance sheet contracted for the second week in a row, the first time that has happened since early January.

What Matters This Week

Markets will focus on:

- CPI and PPI inflation data

- Treasury yields and Fed rate-hike expectations

- Whether AI/semiconductor weakness stabilizes

- Oil prices and Iran/Hormuz headlines

- Breadth outside technology

Bottom Line

The nine-week rally ended as stronger jobs data reignited rate-hike fears and triggered a sharp AI/technology selloff. Earnings expectations remain strong. The question is this is a normal reset after a strong rally or the start of a broader rotation away from AI leadership.

Stock Talk

Past performance is no guarantee of future results. Indexes are unmanaged and one cannot invest directly in an index. They do not reflect any fees, expenses or sales charges. The preceding discussion is for informational purposes only. Investing involves risk and no reference to any security listed above should be considered a buy or sell recommendation. Advisory services are provided through Oak Harvest Investment Services, LLC, a registered investment adviser.