Weekend Update, June 17th, 2024

Index, Sector & Asset Performance

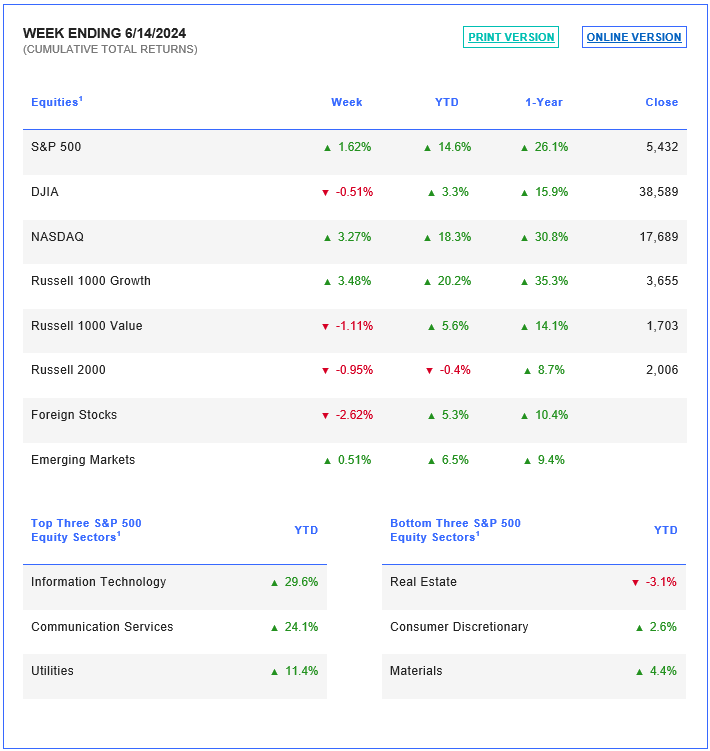

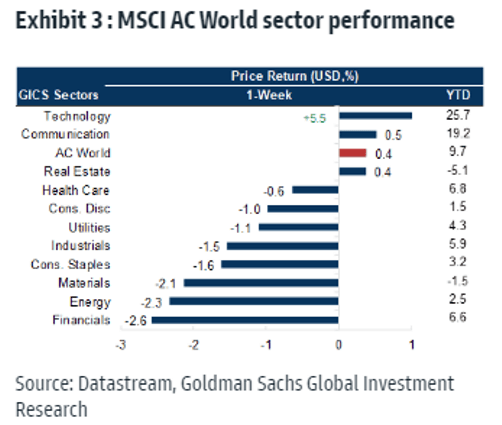

Global equity markets were mixed last week but remained on their winning streak in the US. US equities, particularly the growth-driven Nasdaq Composite and the S&P 500, reached new all-time highs, with the latter up +14% in 2024 following a +24.2% gain in 2023, albeit off a low 2022 close. Encouraging U.S. inflation data helped, but most of the strength in the S&P 500 was confined to technology. The S&P 500 rose +1.6%, while the Nasdaq gained +3.2%. Technology added +6.4% within the S&P 500 and with communication services and consumer discretionary, were the only sectors up on the week.

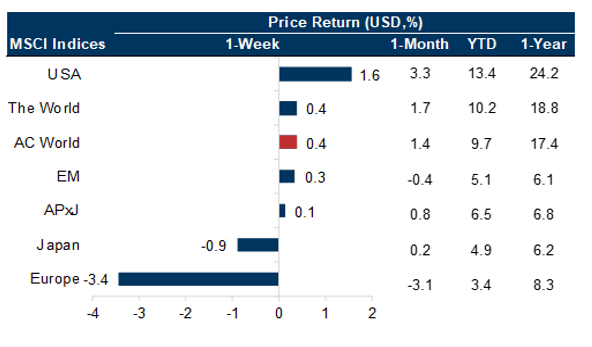

Overseas, the uncertainty surrounding a snap election in France pulled that index down more than -6% on the week and negative for 2024.

Economic Indicators and Earnings Commentary

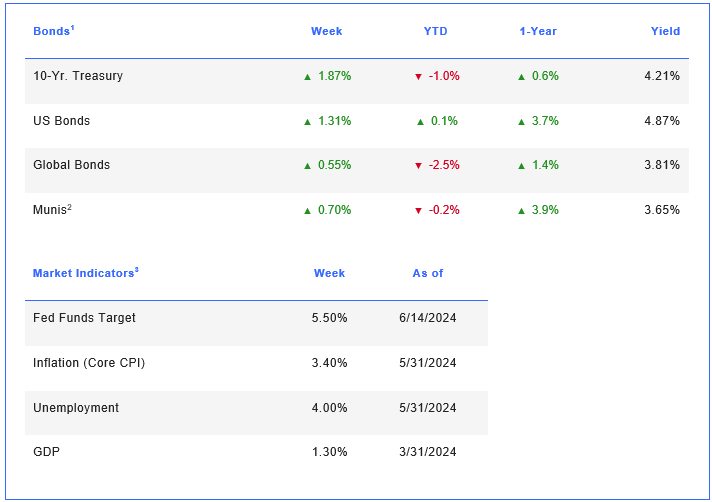

Last Wednesdays U.S. CPI and FOMC meetings were the big events for the first half of June. The CPI was good news. This reversed a string of increases seen earlier this year as inflation did its seasonal turn up. Some of the news was offset by a cautious Fed who lowered its view on this year’s expected rate cuts from 75 bps to 25-50 bps, followed by 100 bps in 2025. Almost half the Fed is still looking at two cuts this year and the good inflation news kept coming later in the week with declines in May producer and import prices.

Initial jobless claims rose a lot, showing that U.S. growth is slowing. The entire Treasury curve took a large parallel shift lower last week, cutting both 2- and 10- year yields by about 20 bps. At just over 4.2%, 10s are now almost -50 bps below this year’s peak reached in late April. The market is also back to fully pricing in two Fed rate cuts this year. These numbers kept the ongoing rally in the S&P 500, led by tech stocks, to fresh record highs, before slipping on Friday.

Global Market Trends/Commodities/Currencies

Outside of the U.S things got squirrelly in Europe with volatility spiking and stock markets dropping, where a very different mood now reigns. The ECB has cut rates due to a softer economy and milder inflation trends. However, the political front brought last week’s big surprise. The European Parliamentary elections on Sunday saw a lean far rightward. In response, French President Macron dissolved parliament and called a snap election for June 30 and July 7. This move was greeted with panic in their markets. The CAC 40 fell almost -7% on the week, while local bond yields rose even amid a big rally elsewhere.

Oil prices rose over +3.5% last week and are up about 6% YTD. Gold prices rose +.7% and are up almost +13% YTD. Copper fell on the week on the back of weak China data. However, copper is still up +13.6% YTD.

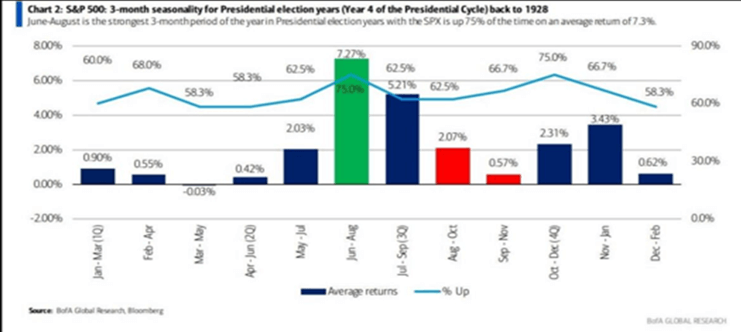

OHFG Exclusive Data & Charts: Summer Rallies are the Norm, Even during Elections

Summer Rallies are the Norm, even during Elections

Here is a table on what historical total return an investor earned during a 3-month holding window in the 4th year of a Presidential election cycle. It also shows historic odds of a positive total return for every 3-month period. For example, an investor buys in May and sells at the end of July. This table says that historically, 62.5% of the time, an investor made a positive 3-month holding period return and their average return was 2.03%, between May and July in the 4th year of a Presidential cycle.

Oak Harvest Weekly Stock Talk: Tactical Trading – Summer Loving

Oak Harvest Live Stream (6/13/24): Advanced Portfolio Management Strategies