Weekend Update, January 27th, 2025

Index, Sector & Asset Performance

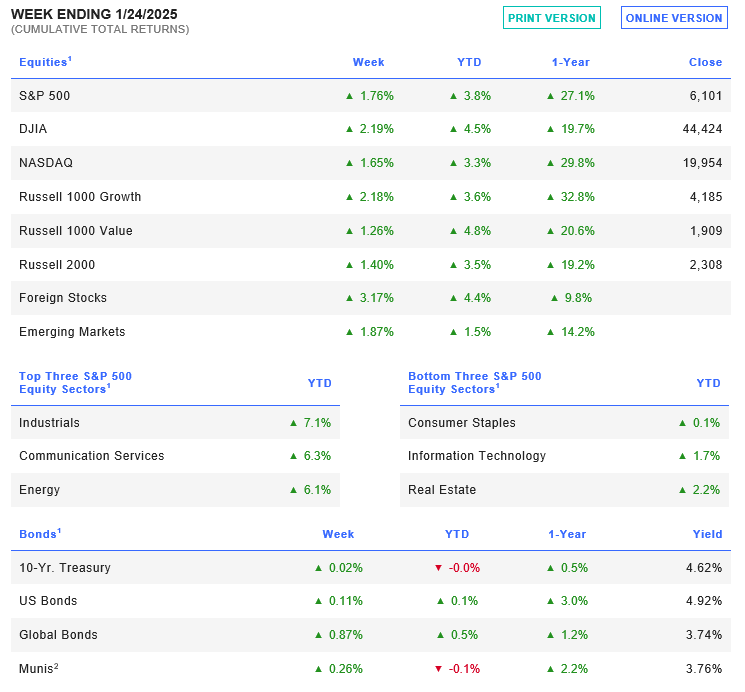

In a holiday shortened week due to the MLK holiday, the S&P 500 index rose +1.7% last week, boosted by better-than-expected quarterly results by bank stocks and hope that the Trump administration will reduce regulations and taxes. The S&P 500 ended the week at 6,101. It reached a record intraday high of 6,128on Friday but ended below the record closing level of 6,118 posted on Thursday. Month to date, the S&P 500 is now up +3.7% for the month and 25% from a year ago.

Better than expected earnings from companies including banks, GE Aerospace (GE), Union Pacific (UNP) and Netflix (NFLX). Communication services (think META, GOOGL, NFLX) had the largest percentage gain of the week, up +4%, followed by a +2.9% bounce in health care and a +2.4% gain in industrials. Markets rallied on an announced partnership between the U.S. and various tech firms to invest $500 billion into AI infrastructure. This sent the AI infrastructure, electrical equipment, power generation, and semiconductors surging.

This morning, U.S. equity futures are down by -0.9% (DJIA) to -4.2% (NASDAQ 100). The main catalyst for the global tech selloff is the advances by China’s DeepSeek spurring a short-term risk off trade rethink of the AI trade that has powered markets higher since late 2022. This happened in front of 4q24 technology earnings reports this week and while 90%+ of companies are restricted from buying back stock. The S&P 500 futures are down -134 points, Nasdaq 100 futures down -830 points, and Dow Jones Industrial Average futures are down -322 points before the market opens.

AI-related stocks are facing a downturn after China’s DeepSeek R1 release, which is seen as comparable to OpenAI’s ChatGPT. It’s reported that the new model might be more cost-effective and operate on less advanced chips.

Nvidia is down -12%, AMD -4.9%, Super Micro -10%, Arm Holdings -9.6%, Dell Technologies -8.8%, Hewlett Packard Enterprise -6.1%, and ASML -8.3%. Broadcom and Marvell Technology both fell -12% pre-open.

The Treasury market is rallying with interest rates down along the curve from -8.5 bps (2s) to -12.2 bps (7s). The DXY/Dollar is also weaker.

Economic Indicators and Earnings Commentary

The Federal Reserve meets mid-week with Chair Jerome Powell set to pause their interest-rate cutting cycle on Wednesday by leaving the upper bound of their key rate unchanged at 4.5%. Traders will focus on Powell’s press conference for clues as to what comes next. This is what historical soft-landing cycles look like. According to Goldman Sachs, the FOMC’s decisions will likely “hinge in large part on how the Committee chooses to handle tariffs. In their base case, tariffs would provide only a modest and one-time 0.3pp boost to inflation, causing it to fall by less but not to rise and leaving the door open to rate cuts”.

For those following government data, Initial jobless claims remained at 223k (which will most likely be revised upward due to the weather events), but continuing claims rose to 1,899k, the highest level since 2021.

The December PCE inflation report is on Friday, and the first estimate of 4Q GDP growth from the government on Thursday. The Richmond Fed Index and the Chicago PMI are also released this week.

China’s economic activity continues to sputter underlining the need for Beijing to do more to prevent another slowdown.

Likewise, Europe is weak, and the ECB is likely to further lowering interest rates this week for a fourth straight meeting.

4Q2024 earnings season started strong. This week’s earnings include AT&T (T), Boeing (BA), Starbucks (SBUX), Microsoft (MSFT), Meta Platforms (META), Tesla (TSLA), International Business Machines (IBM), Apple (AAPL), Visa (V), Mastercard (MA), Caterpillar (CAT), United Parcel Service (UPS), Exxon Mobil (XOM), AbbVie (ABBV) and Chevron (CVX). Most of the largest tech companies report this week.

Global Market Trends/Commodities/Currencies

Oil prices plunged to $74.66/bbl after President Trump urged OPEC at Davos to reduce oil prices.

Bitcoin fell back below $100k this morning on risk off selling.

The US Dollar fell last week as US economic data missed forecasts and Japan looked to raise interest rates.

Gold rose for a fourth straight week, coming within dollars of a new all-time high.

Oak Harvest Weekly Stock Talk

No release due to Houston Weather event.

Past performance is no guarantee of future results. Indexes are unmanaged and one cannot invest directly in an index. They do not reflect any fees, expenses or sales charges.