Weekend Update, February 16th, 2026

A Bullish Inflation Print

Index, Sector, and Asset Performance

The US stock market is closed today for Presidents Day. Chinese markets are closed all week for their Lunar New Year holiday.

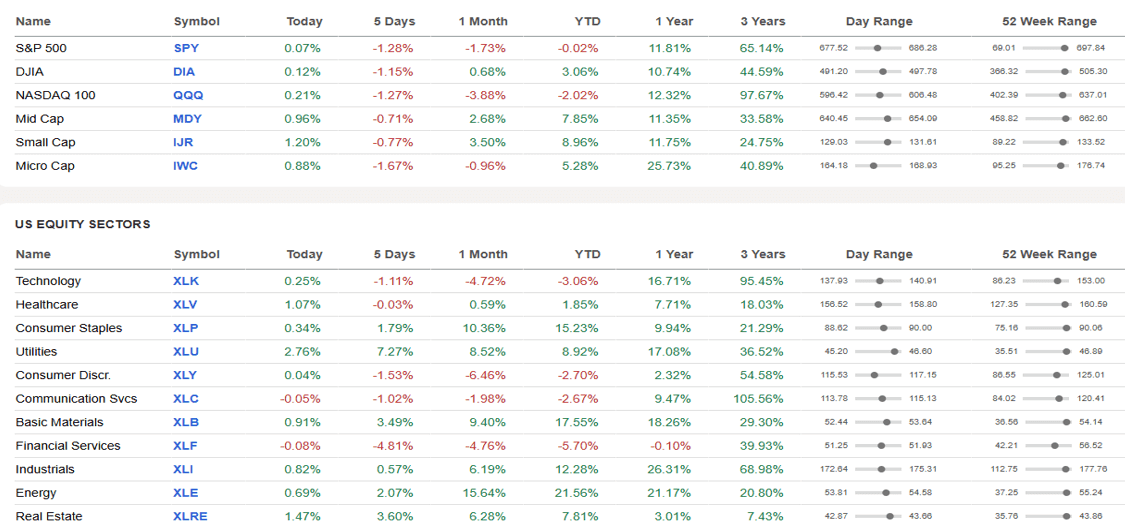

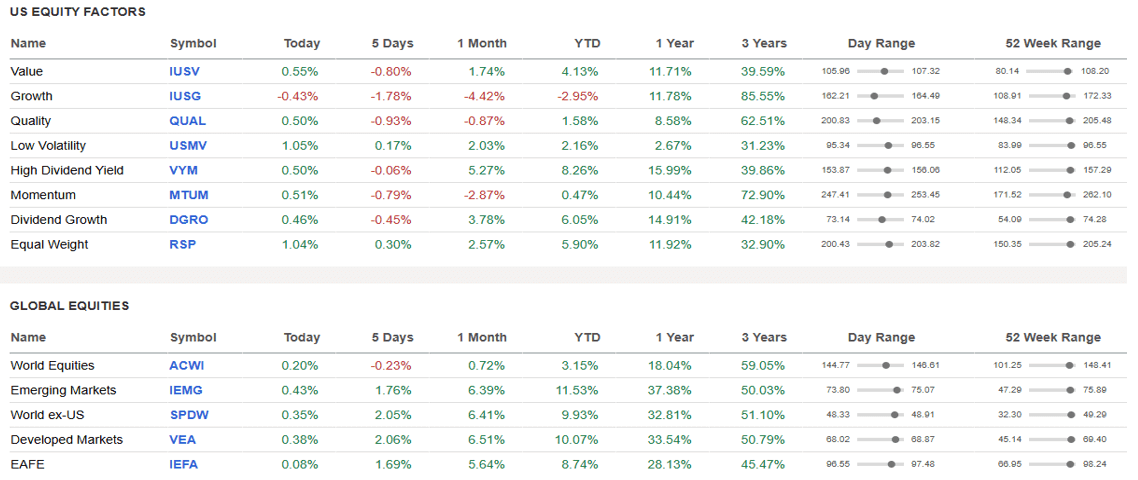

The S&P 500 fell -1.4% last week as declines in the financial and communication services sectors outweighed utility and safety group gains. S&P 500 ended the week at 6,836 and has now traded between 6950 and 6750ish since last October, 4.5 months and counting. The index is down -1.5% for the month of February and back to flat YTD including dividends. The growth biased Nasdaq Composite fell ending the week down -2.10%. Software stocks helped lead growth and tech indexes lower, as worries over whether AI would render many forms of software redundant maintained their presence on investors’ wall of worry.

The financial sector had the largest percentage drop last week, falling by -4.8%, followed by a -3.5% decline in communication services, a -2.1% decline in consumer discretionary and a -2% drop in technology stocks.

AI disruption, real or imagined, was a big factor in last week’s sector action. Early in the week, Altruist announced a new AI-powered tax planning tool that promises to do the work “within minutes”, causing financial service firms’ stocks to drop on Tuesday. The hardest-hit stocks in the financial sector included Arthur J. Gallagher (AJG), which lost -14%, Ameriprise Financial (AMP) and Willis Towers Watson (WTW), each down -13%. LPL Financial tumbled -11% in Tuesday trading, while Charles Schwab fell -7.4% and Raymond James Financial lost -8.8% amid fears that AI will disrupt their industry next

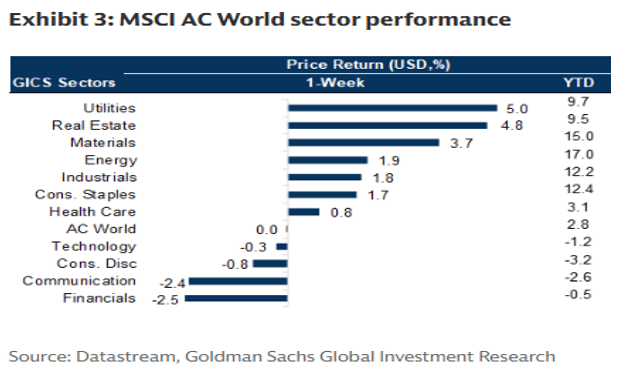

Lower growth, higher yield, utility sector jumped +7.1%, followed by a +3.9% rise in REITs and a +3.7% gain in materials. Energy, consumer staples and industrials also rose. Vistra (VST) was the top utilities gainer, climbing +15%. Iron Mountain (IRM) was the best performer in real estate, rising +15%.

Per Goldman Sachs global sector returns last week:

The appointment of Kevin Warsh as Fed Chairman is creating a bit of uncertainty to the timing of future Fed policy moves. Last week’s data makes earlier Fed easing more likely throughout 2026.

Economic Indicators and Earnings Commentary

The labor markets unexpectedly added 130k jobs (over 60% healthcare sector) in January which is the most since 2024. BLS reported that in January the US added 130K jobs, double the 65K median estimate and up from a downward revised December print of 48K (vs 50K previously). This was also the highest monthly job increase since December 2024. As we’ve seen for the last 2-3 years, expect this data to be revised downward over the coming months as the “seasonal adjustment” was the entire upside surprise. For a thorough breakdown on the data, “Zerohedge”” remains the best source we’ve found.

The economic calendar this week will feature reports on Q4 GDP as well as the December personal consumption expenditures price index. The PCE index is the Federal Reserve’s preferred inflation gauge. Delayed reports on November and December housing starts and new home sales will also be released.

Earnings reports this week include Medtronic (MDT), Palo Alto Networks (PANW), Walmart (WMT), Deere (DE) and Alibaba Group (BABA).

Per Goldman: Consensus expects S&P 500 EPS growth of 7% year/year in 4Q 2025, but this forecast appears too conservative once again. S&P 500 EPS grew by 10% or more during each of the first three quarters of 2025, exceeding analyst estimates by an average of +6 pp.

Commodities and Currencies

Oil crossed above $63 on geopolitics and concerns over Iran.

Copper, gold, silver and other industrial metals have hit new ATHs and are up materially YTD on geopolitical concerns and a fear of global currency devaluation. Precious metals like gold and silver continue their volatile yet strong performance with gold between $4,800-5,000 and silver between about $75-110/oz.

Copper also declined after gold and silver, retreating from recent highs on recent stockpile growth

Crypto assets and bitcoin have been volatile since pulling back from their mid-summer $125k ATH and sit near $70k, -45% off its highs.

The US dollar has been stuck between 97-99 since last April 2025.

OHFG Stock Talk

Per Seeking Alpha:

Past performance is no guarantee of future results. Indexes are unmanaged and one cannot invest directly in an index. They do not reflect any fees, expenses or sales charges. The preceding discussion is for informational purposes only. Investing involves risk and no reference to any security listed above should be considered a buy or sell recommendation. Advisory services are provided through Oak Harvest Investment Services, LLC, a registered investment adviser.