Weekend Update, August 4th, 2025

Index, Sector, and Asset Performance

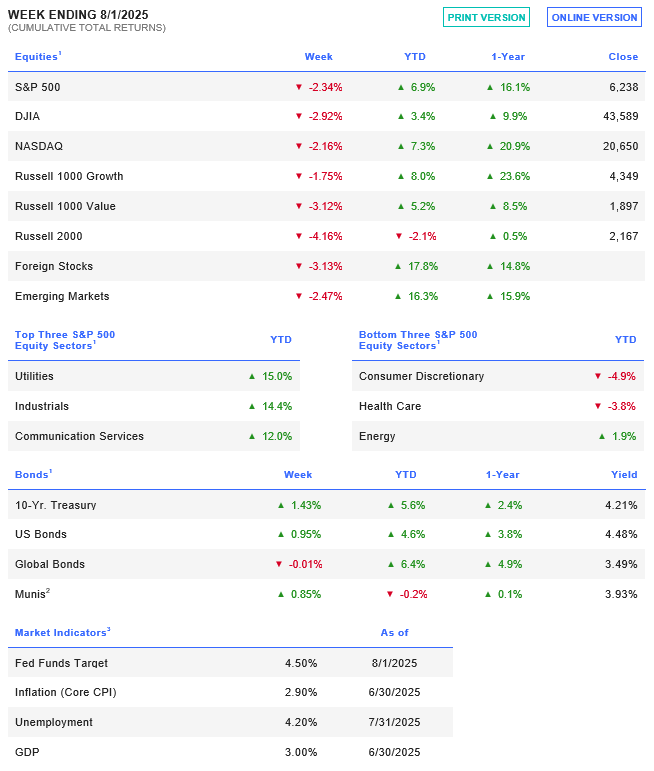

Seasonally hits on cue, with August through late September stalling and exhibiting weakness. The S&P 500 sold off every day last week on an intraday basis. When the week ended, the Nasdaq 100 and S&P 500 (-2.4%) were both down by over -2% for the week, and the Russell 2000 fell over -4%. The S&P 500 reversed almost -3.35% from its Thursday intraday ATH to its Friday low’s.

Even with Fridays losses, the S&P 500 is up+ 6.1% this year. The S&P rose +2.2% in July, its third consecutive monthly gain.

Utilities were the leading sector on the week up +1.5% as the market rotated into weaker real growth, lower bond yield proxies. Economically weaker and stronger dollar sensitive sectors, such as materials, led decliners, falling -5.4%, while consumer discretionary lost -4.5% and healthcare was down -3.9%. Counterintuitively for a slower economy, healthcare stocks fell as President Trump threatened drug makers with broad price controls and China demand remains weaker.

Per Goldman Sachs:

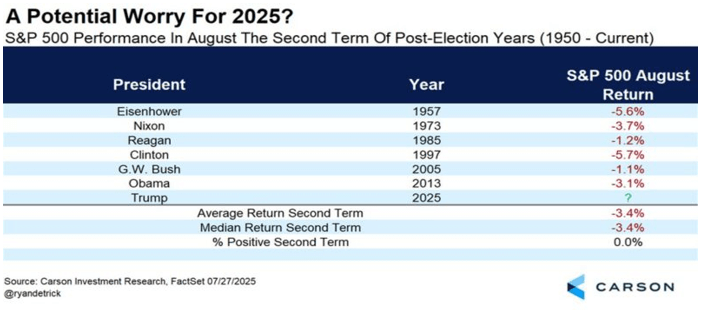

We are entering a seasonally weak period which is historically even worse during the second term of a President. Per Ryan Detrick at the Carson Group, August has been overlay weak in the first year of a second term President with an average loss of almost -3.5%.

Economic Indicators and Earnings Commentary

There was an FOMC meeting last week where the committee left rates unchanged, sounded hawkish on inflation, and had 2 members dissent on the vote for the first time in decades.

Subsequently, a jobs number was released with continued huge negative revisions down showing a weaker employment market for Americans. Non-farm payrolls rose by 73,000 in July, according to data released Friday by the BLS, missing the estimate compiled by Bloomberg for a 104,000 increase. The OHFG investment team has highlighted this overstated BLS data for over two years. Once again, Zero Hedge does the excellent rundown of what’s really going on in the US jobs market.

ISM Services survey and June Durable Goods as well as consumer credit updates are some of the few data points this week.

The market just processed almost 35% of the S&P 500 earnings reports last week and, on the surface, the numbers looked strong. Most companies beat expectations, which yes, had been lowered earlier in the year for tariff uncertainty. Revenue and earnings growth are still coming in above estimates, however many leading stocks sold off. With negative summer seasonality inflecting, the economy slowing, and demand pull forward having been likely in the 2nd quarter in front of tariff implementation, no one can dispel the notion of “double ordering”, demand pull forward, or inventory building until later in the 3rd quarter.

2/3rds of the S&P 500 have reported 2Q earnings, and over 60% of the companies that have reported have beaten consensus EPS forecasts. This is one of the highest positive surprise rates in 25 years, though the bar was set low coming into the quarter.

Apple (AAPL) after reporting a double beat and its best revenue growth in years, stock sold off with the market. This was the 4th consecutive negative earnings reaction in absolute terms.

They reported revenues of $94.04B, versus the expected $89.56B, and earnings per share of $1.57, versus the expected $1.44.

Monolithic Power Systems (MPWR) had a double beat. They reported revenues of $660M, versus the expected $650M, and earnings per share of $4.21, versus the expected $4.12.

This week’s earnings calendar includes Palantir Technologies (PLTR), Advanced Micro Devices (AMD), McDonald’s (MCD), Walt Disney (DIS), and Eli Lilly (LLY).

Commodities and Currencies

Oil continues to do little as demand is weak and OPEC continues pumping seemingly to hurt Russian economics.

Gold is stuck near $3,300/oz.

Bitcoin sold off toward $115,000.

Oak Harvest Weekly Stock Talk

Summer Stock Seasonality Begins

Past performance is no guarantee of future results. Indexes are unmanaged and one cannot invest directly in an index. They do not reflect any fees, expenses or sales charges. The preceding discussion is for informational purposes only. Investing involves risk and no reference to any security listed above should be considered a buy or sell recommendation. Advisory services are provided through Oak Harvest Investment Services, LLC, a registered investment adviser.