Oversold Earnings Bounce into Seasonally Weak May

After selling off -5% during the first 3 weeks of April, the S&P 500 rebounded +2.7% last week, in its normal seasonal timing, on strong earnings by technology stocks. Economic data junkies got some relief that PCE inflation data series wasn’t higher than feared in March. Interest rates are also starting this week rallying, largely retracing last week’s losses. The 10-year Treasury yield is down -5 bps to 4.62% and the 2-year yield is back below 5.0% this Monday morning.

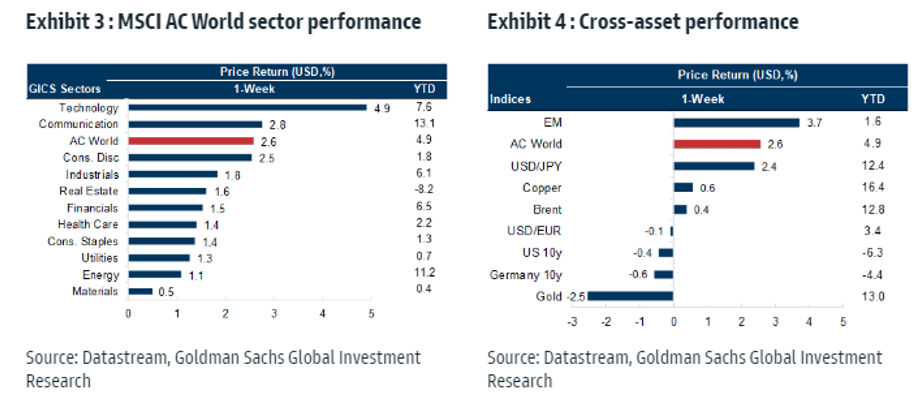

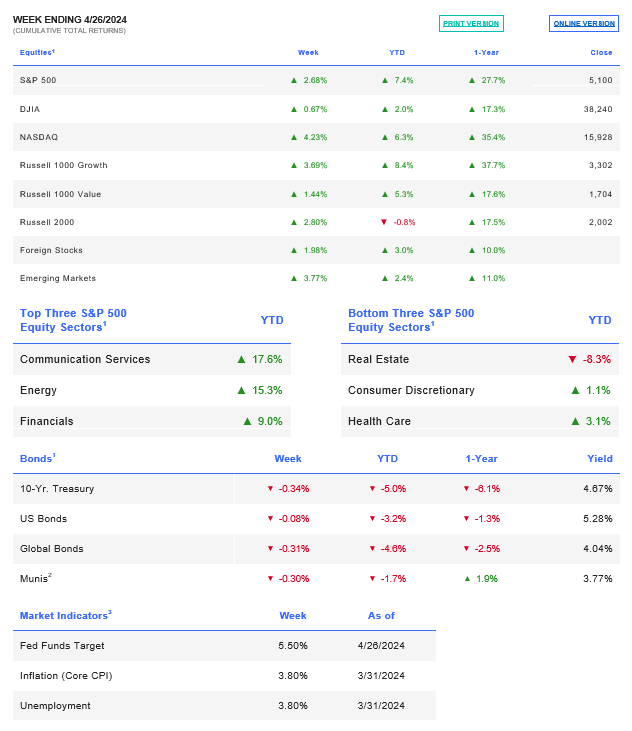

Sector and asset class performance last week, compiled by our friends at Goldman Sachs:

The Federal Reserve meets mid-week and won’t lower policy rates on Wednesday. It’s likely to message a hawkish tilt. On a positive note, it could announce details on when and how much it will taper QT, which Chair Powell has previously said may come “fairly soon”. A slower pace of balance sheet runoff in its bond portfolio could take some pressure off long-term interest rates. Almost all Fed members have warned that recent inflation numbers have largely closed the door on near-term rate cuts. Recall, that the Fed has a poor history of forecasting future events.

The most recent crisis “da jour” presented by the macro bear camp throughout the financial media is the continued rapid devaluation in the Japanese yen. This morning the JPY was under more pressure having crossed over the ¥160 mark overnight. It hasn’t closed above that level since 1986. While possibly sounding smart at cocktail parties in the Hamptons, this is likely another non-event for US equities, however historically, our stock markets are seasonally week in the month of May, averaging a down move of almost -1.5% in the month during Presidential election years. Between, the Fed this week and insider selling windows reopening shortly, our team expects normal seasonal weakness over the coming weeks.

Click here to watch the Oak Harvest Weekly Stock Talk: The Good, the Bad, and the Ugly.

![]()