Iran War – Max Pain? Go Time?

Key Takeaways Last Week

- U.S. equities finished the week lower, with the Dow lagging and the Nasdaq more resilient.

- S&P 500 closed at 6,632, its lowest level of 2026, -5% below its ATH, and down -3.1% YTD.

- The dominant driver was oil and geopolitical risk in Iran, accelerating inflation concerns.

- Defensive groups fared better than cyclicals.

- This week, focus shifts to the FOMC, and earnings including Micron, FedEx, and Accenture.

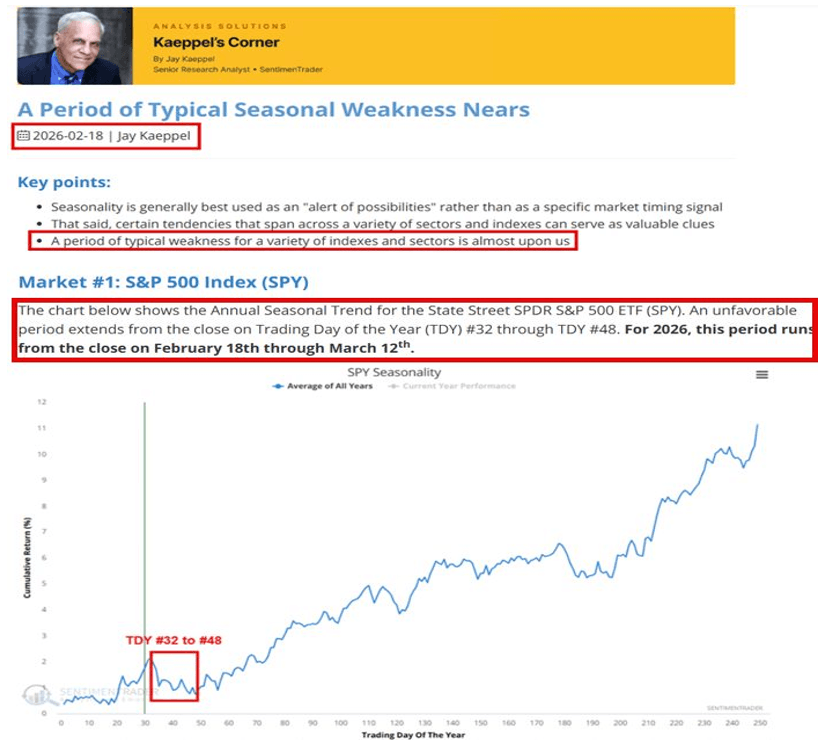

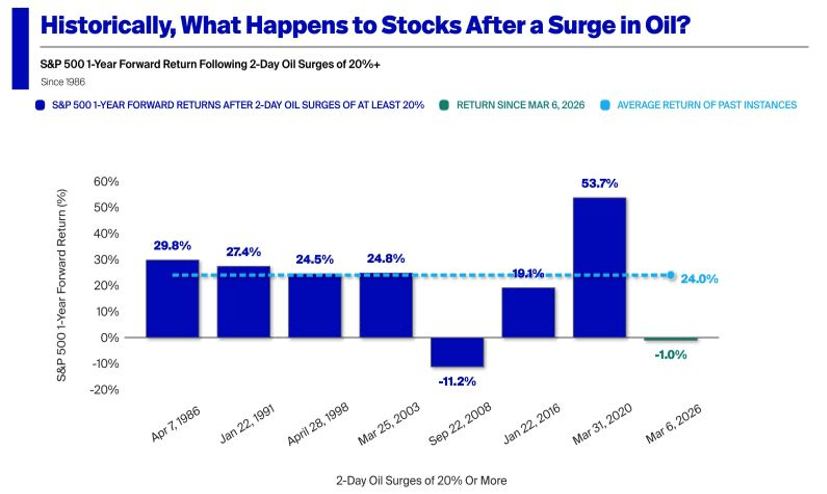

- Market tone remains sensitive to headlines in Iran and inflation however we are entering a period of historically better seasonal stock performance.

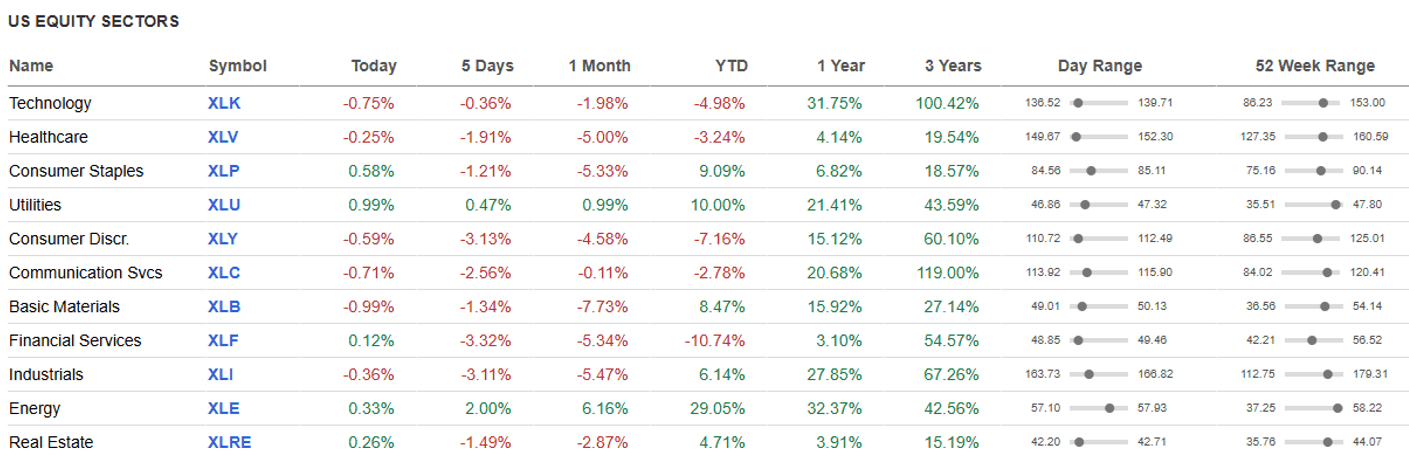

U.S. Stock Performance – Index and Sector Moves

Source: Seeking Alpha

S&P 500: sold off on higher inflation concerns. Sector dispersion remains high.

Dow 30: weakest index with largest financial and economically sensitive stocks.

Nasdaq 100 / Nasdaq Composite: attempting to bottom on “peak” inflation and earnings.

Source: Seeking Alpha

Defensives led on a relative basis with only utilities and energy up on the week.

Energy remains the strongest major sector YTD, even pre-Iran war.

Financials and banks were the weakest sector on the week and remain a major laggard YTD.

The market continues to reflect a slower-growth, higher inflation concerns and a geopolitically sensitive market regime.

Occidental Petroleum (OXY) had the largest percentage increase in energy, rising +6.8%, followed by a +5.5% gain in APA (APA). Fiserv (FISV) and Global Payments (GPN) in the financial sector dropped -10% each. FactSet (FDS) shares fell -9% as Deutsche Bank cut its price target on the stock to $275 per share from $335. In industrials, Axon Enterprise (AXON), fell -14%, and Equifax (EFX), dropped -11%. Ulta Beauty (ULTA) was the worst performer in consumer discretionary, tumbling -17%.

Volatility & Risk Sentiment

- Equity volatility increased dramatically last week

- Risk sentiment deteriorated through the week following the spike in oil.

- The market is entering what is seasonally a stronger return and lower volatility period.

Bonds & Interest Rates

- U.S. Treasury rose last week on continued oil shock induced inflation fears.

- The bond market is balancing slowing growth against sticky inflation and commodity shocks.

- Federal Reserve expectations for 2026 remain highly uncertain.

Economic Data, Monetary Policy & Earnings

- CPI: headline inflation remained contained, but the market is worried about energy. CPI (Feb): headline +0.3% m/m, +2.4% y/y; core CPI +2.5% y/y. Inflation looked relatively contained before the oil shock became the market’s focus.

- Core inflation: sticky enough to keep the Fed cautious. Major components are easing.

- Existing home sales: slow but better than expected.

- Jobless claims: low enough to imply labor-market resilience. Initial jobless claims: 213,000 for the week ending March 7, down 1,000 from the prior week.

- Consumer sentiment: soft, reflecting pressure from inflation and job uncertainty.

Monetary Policy / Fed

The market is now focused on this week’s March 17–18 FOMC meeting with key themes: inflation not yet fully defeated, energy risk complicating disinflation, and the labor market weakening but resilient.

Earnings reports this week include Micron (MU), FedEx (FDX), and Accenture (ACN).

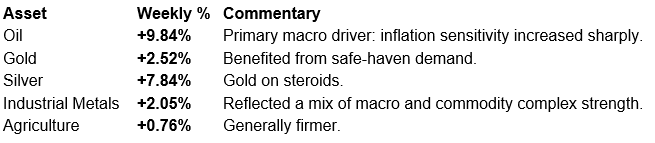

Commodities, Currencies & Macro Assets

Commodities were one of the biggest stories of the week, with most broadly higher on the Strait of Hormuz shutdown and its effects on energy and other cargo disruptions.

Bitcoin is trading around $73k+, rising even as stocks have been volatile.

Commodities

Currencies – DXY (Dollar Index): rallied back above 100 on a flight to safety and a short squeeze. Emerging market currencies sold off on global growth concerns.

OHFG Stock Talk

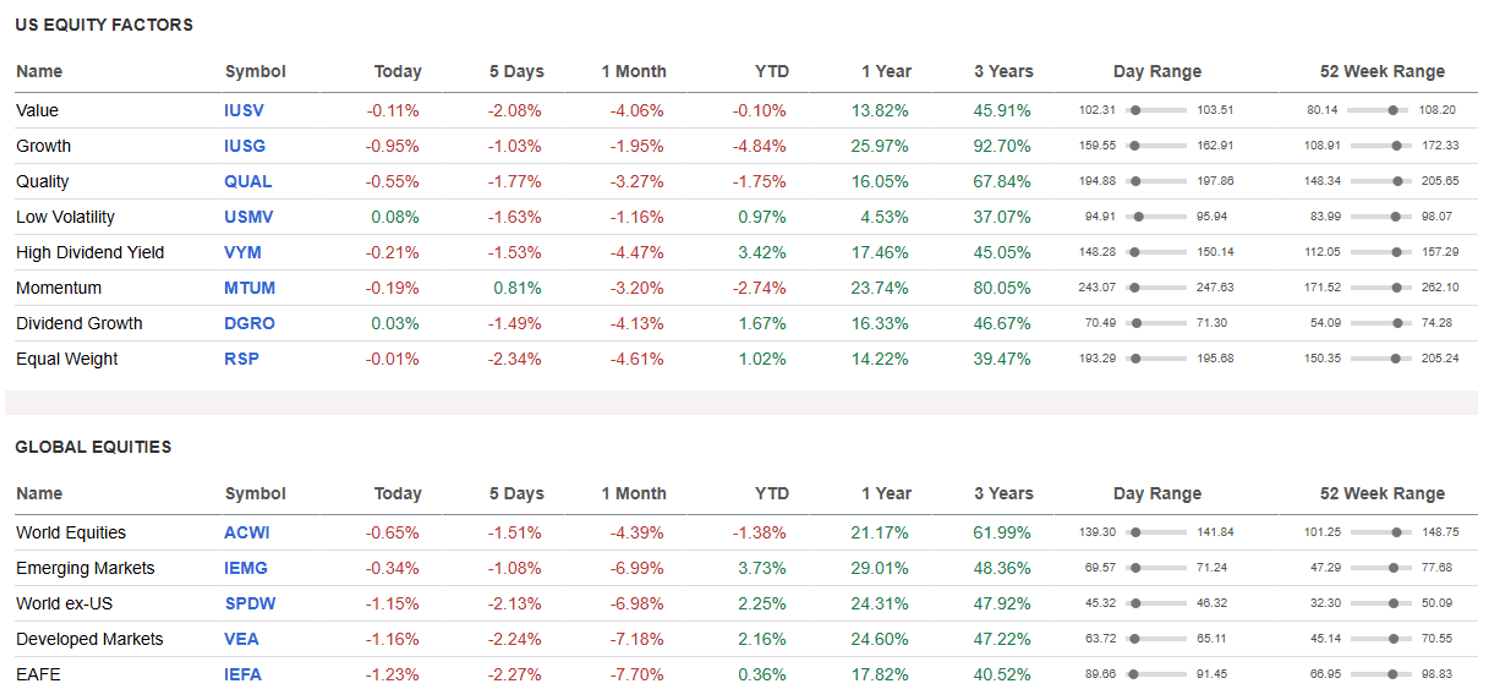

Factor Returns

Source: Seeking Alpha

Extra Data

Source: Jay Kaeppel

Source: Phil Rosen

Past performance is no guarantee of future results. Indexes are unmanaged and one cannot invest directly in an index. They do not reflect any fees, expenses or sales charges. The preceding discussion is for informational purposes only. Investing involves risk and no reference to any security listed above should be considered a buy or sell recommendation. Advisory services are provided through Oak Harvest Investment Services, LLC, a registered investment adviser.