Weekend Update, April 28th, 2025

A GOAT Appears

Index, Sector & Asset Performance

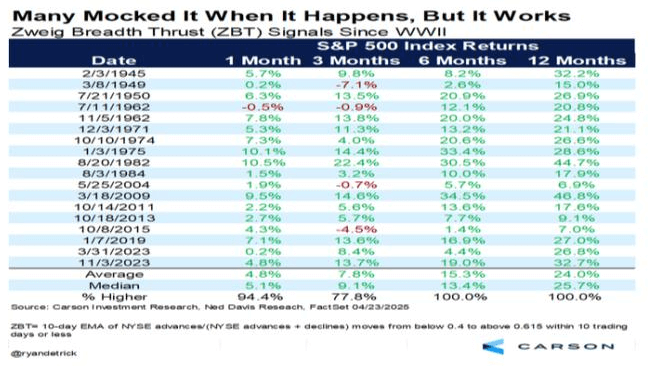

A GOAT stock market data indicator, Zweig Breadth Thrust, is triggered on April 24th. US stocks rallied strongly last week with the walk back on tariffs last week by President Trump saying the tariffs on Chinese imports would “come down substantially.” China also exempted some imports from the US from its 125% tariffs. With this and negative positioning, the S&P 500 staged a BIG turnaround last week, in a move which traders will call a bullish “engulfing” candle versus the previous week’s range. This rally broke to a new recovery high with S&P 500 closing the week at 5525. The rally came as financial firms beat EPS estimates and GOOGL provided a relief rally amongst large cap technology shares. The S&P 500 rose +4.5% fueled in part by President Donald backing away from a threat to fire Federal Reserve Chair Jerome Powell.

One of the most reliable signals in market history triggered on April 24th: the Zweig Breadth Thrust.

We’ve discussed this indicator 2 other times in the last 7 years including in October 2023 and December 2018 at or near the markets low pivot. This indicator is known for its historically unique ability to spot the start of major bull moves by combining sentiment, breadth and momentum, showing not just how many stocks are participating, but also how quickly the shift happens. According to Ryan Detrick, since WW2, this indicator has only triggered 18 times, and the S&P 500 has never been lower 6 or 12 months later. Here’s the data, which we will cover in more detail on this /Fridays Stock Talk:

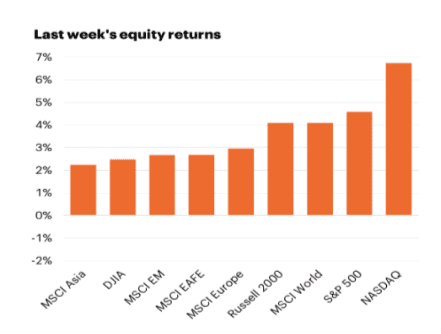

A summary of last week’s returns ex-Gold, from FS Investments shows the tech heavy NASDAQ leading, and Asia lagging. Almost all sectors and countries rose last week.

Bonds prices gained and yields fell over the second half of the week as tariff turmoil slowed. The 10-year yield rose to 4.43% early in the week before closing at 4.24%. Markets are trying to guess the timing of the first rate cut.

Economic Indicators and Earnings Commentary

The Citi Economic Surprise index rose back above zero for the first time in months.

New home sales rose +7.4%, as builders continue to offer incentives to outcompete the existing home market, where sales fell -5.9%. The total home sales were the lowest in 3 years.

Durable goods order surged +9.2% in March, on a rise in aircraft orders designed to front-run tariffs. Initial jobless claims rose 222,000 last week. This week Q1 GDP growth is expected to be around 0% and April nonfarm payrolls are expected to rise 125,000.

On the earnings front, Google released better-than-expected Q1 results but also said its board raised its quarterly dividend by 5% and authorized the repurchase of up to another $70 billion in class A and C shares. The company’s shares rose by about +7% on the week.

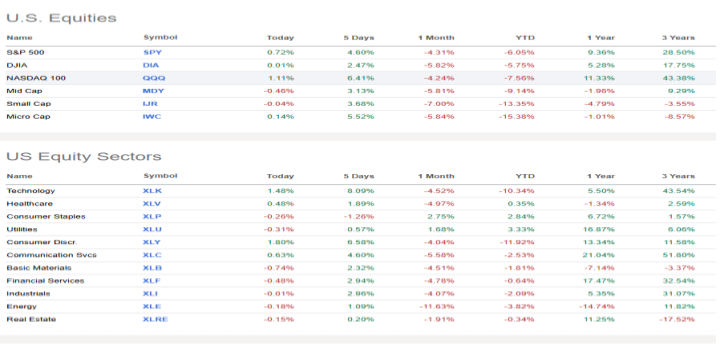

The technology sector had the largest percentage increase last week, climbing +7.9%, followed by a +7.4% gain in consumer discretionary and a +6.4% rise in communication services. Financials and industrials rose by about +3% each while materials added +2%.

ServiceNow (NOW) had the largest weekly gain in the tech sector, jumping +22% as the company posted Q1 earnings per share and revenue above analysts’ mean estimates. The company also forecast Q2 subscription revenue above the Street view at the time. In consumer discretionary, Tesla (TSLA) shares, which were almost -50% off its election high, climbed +18%. The electric vehicle maker’s Q1 adjusted earnings per share and revenue both came in below Street views, but Chief Executive Elon Musk said he will recommit more of his time to the company. Netflix (NFLX) rose +13% as the company’s Q1 results and Q2 guidance both exceeded analysts’ expectations. Consumer staples was the lone sector in the red for the week, dropping -1.4%. Kimberly-Clark (KMB) had the largest percentage drop in consumer staples, falling -7.8%. The company reported Q1 adjusted earnings above the Street view, but its revenue slightly missed analysts’ mean estimate. Pepsi also forecast a weak 2025 on destocking and lower pricing.

This week’s earnings calendar features Visa (V), Coca-Cola (KO), Microsoft (MSFT), Meta Platforms (META), Apple (AAPL), Amazon.com (AMZN), Eli Lilly (LLY), Mastercard (MA), McDonald’s (MCD), Berkshire Hathaway (BRK.A, BRK.B), Exxon Mobil (XOM) and Chevron (CVX).

Commodities and Currencies

Oil price tanked last week as OPEC+ members signaled a willingness to accelerate production increases. U.S. oil rig counts fell sharply over the past two weeks hurting oil services stocks.

Gold finally had a blow off top, hitting $3,500/oz and reversing quickly back toward $3,200/oz. IT still remain +24% higher YTD in dollar terms.

The U.S. dollar looks to have troughed near 100, at peak US Unexceptionalism, down -10% from its December 2024 highs.

1Q25 Earnings season ramps in full force this week including Google. Others on tap per Goldman.

Oak Harvest Weekly Stock Talk

Market Correction or Bear Market: The Low or a Low?

Market Data from Seeking Alpha

Past performance is no guarantee of future results. Indexes are unmanaged and one cannot invest directly in an index. They do not reflect any fees, expenses or sales charges.

The preceding discussion is for informational purposes only. Investing involves risk and no reference to any security listed above should be considered a buy or sell recommendation. Past performance is no guarantee of future results. Advisory services are provided through Oak Harvest Investment Services, LLC, a registered investment adviser.