Earnings and Buy Backs Forthcoming

The overall S&P500 dropped a bit over -2% during last weeks holiday shortened and lower liquidity pre-Easter 3-day weekend. It sits down around -8.5% year to date. The tech heavy NASDAQ dropped almost -4%. Rising long-term Treasury yields, with the 10-year rate reaching 2.85% last week, which directly create rising real estate mortgage rates, have weighed on cyclical equities the most. Technology, consumer discretionary, and residential real estate-oriented stocks have been hurt the most year to date even though end demand has remained strong. Oil prices bounces last week with domestic WTI oil holding near $107 per barrel and natural gas prices sitting around $7 per million BTU (up 100% YTY).

Financial markets have now basically priced in two 50 basis point interest rate hikes at the Federal Reserves next two meetings. (May 4th). This is while the economic data has been peaking and growth moderating. There are currently more downside risks to growth than upside throughout summer. This is seasonally normal. Current economic slowdown causes include, China Covid shutdowns hurting manufacturing; Russian invasion in Ukraine causing European growth to slow and consumer sentiment to tank overseas; and higher commodity prices squeezing consumer demand and corporate profits domestically.

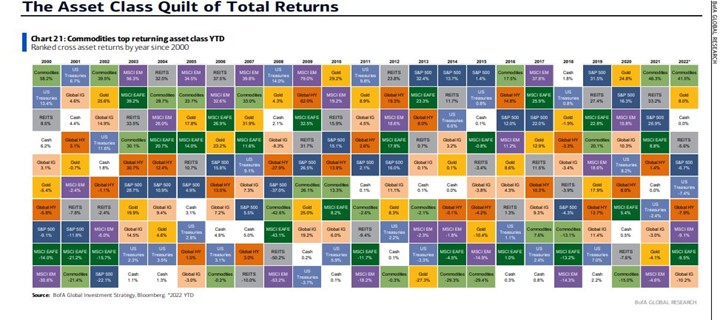

We have attached the Asset Return Quilt, courtesty of Boa, for your review. The only positive returning groups year to date are commodities and gold.

Weekly Stock Talk Podcast: First Quarter 2022 Review

https://www.youtube.com/watch?v=_xQyGKqdd54&list=PLxj0FBH5Bt8twiZx9RvxpW9AydohZ5W3-&index=25

New or Noise: Economic Growth has Peaked-The Bond Market and Yield Curve

https://www.youtube.com/watch?v=EYYsas-FzDI

Oak Harvest YouTube Channel

https://www.youtube.com/channel/UCkLvOm9F5iC01-hHxRmUXpQ

Stock Talk Podcast (Weekly Market News and Opinion from Oak Harvest):

https://oakharvestfg.com/stock-talk-podcast/

The Investor Mindset Podcast (Introduction to Critical Concepts for Investors):

https://oakharvestfg.com/investor-mindset/

This content contains general information and express the views of Oak Harvest Investment Services. All data, articles, and information cited are believed to be reliable at the time of creation; however, Oak Harvest does not warrant any information contained herein to be correct, complete, accurate or timely.

Oak Harvest provides links to content produced by other websites that OHFG does not control, and Oak Harvest does not necessarily approve or endorse such content and does not guarantee its accuracy. Nothing in this content constitutes personalized investment advice. Any charts, indicators, or graphs included or referenced in this content have limitations, and no such material is able, in and of itself, to provide a buy or sell recommendation for any security. Strategies and ideas discussed may not be right for you, and views and opinions expressed may change without notice. Strategies and ideas discussed will not apply to all client accounts or portfolios.

Nothing in this content constitutes a recommendation, or an offer or solicitation to buy or sell securities. Oak Harvest makes no assurance as to the accuracy of any forecast or projection made. Not all past forecasts or projections have been accurate. No current or future forecasts and projections are guaranteed to be accurate. And future forecasts may not be as accurate as any forecasts discussed. Indexes like the S&P 500 are not available for direct investment and your results will differ. Past performance is not indicative of future results. Investing involves the risk of loss.