3rd Quarter in the Books

Overview

The S&P 500 dropped 2.2% in a volatile week and is down about 4% from its September 2nd high, finishing the 3rd quarter roughly flat. This broke a seven-month winning streak for its worst monthly return since March 2020, amid fears of political gridlock leading to a US debt default and supply chain disruptions causing a combination of cost and supply issues for the normally strong consumer led 4th quarter spending. Year-to-date, the S&P 500 is up 16.0%.

After jumping to 1.55% last Wednesday, the 10-year Treasury yield ended the week at 1.48%.

Global equities were almost all lower last week, with China’s (+0.3%) stock market among the few gaining. The Japanese Nikkei (-4.9%) and Nasdaq (-3.2%) were the two worst performers, with rising interest rates weighing heavily on the tech heavy NASDAQ.

Merck Trials

Trial results for Merck’s anti-viral pill to limit the severity of COVID illness were released late in the week and provided a rest from the negative news headline sentiment. This drug could greatly reduce the threat of future virus waves, reducing the strain on the health care system, and eventually moderating supply chain issues.

Shutdown Avoided

The U.S. government averted a shutdown last Friday, but Congress will have to revisit funding before December 3 when the current resolution expires.

Washington D.C remains a mess, between and within both parties. Congress is deadlocked around the $1 trillion infrastructure plan and the Democrats are flailing in their larger $3.5 trillion social infrastructure and climate change package. Senator Joe Manchin of West Virginia provided last week’s twist from moderate Democrats trying to materially downsize the $3.5 trillion, pay for everything, number.

The Fed and QE

QE is still on-going and the Fed’s balance sheet rose at an accelerating pace of 20% last week, the highest rate since April. Last week, the Fed announced that they anticipated slowing the rate of asset purchases relatively soon, perhaps even as soon as November or December of 2021.

Recent revelations of “well-timed,” personal trading by Fed governors has brought harsh comments and attention from Senator Warren onto the Fed, with Warren stating clearly that she wants current Fed Chair Jerome Powell gone. However, Powell is still favored, and Senator Warren has no direct role in the process. Oddsmakers have Powell with a 64% chance of continuing in his role. Oak Harvest has noted that this is a story worth following. The markets dislike uncertainty, and the possibility of Powell being replaced could be a primary risk driver in early 2022.

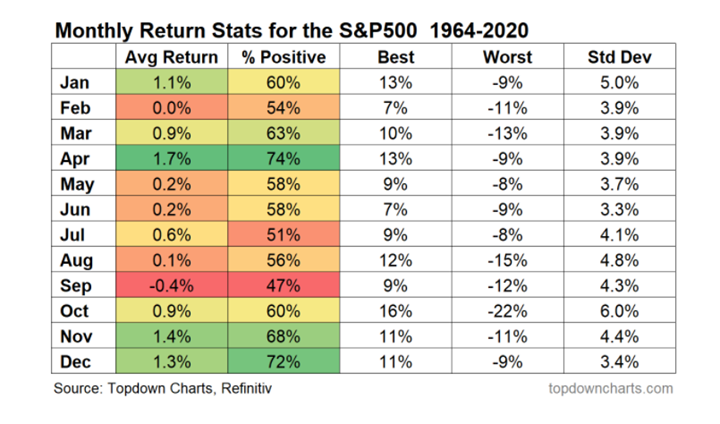

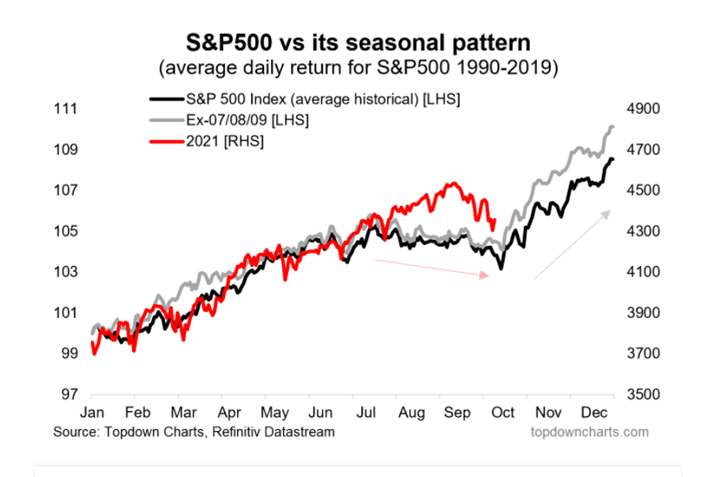

Unprecedented?

Much has been made all year of the unprecedented nature of the stock markets and economy. However, so far, the path of the market has been anything but unprecedented, almost to the point of looking predetermined. We are close to entering what has historically been the strongest time period for both our economy and the markets. The economic surprise indicator we follow is now quickly moving higher and closing in on its first positive reading since July, without any investor fanfare.

Charts of Note

Stock Talk Podcast (Weekly Market News and Opinion from Oak Harvest):

https://oakharvestfg.com/stock-talk-podcast/

The Investor Mindset Podcast (Introduction to Critical Concepts for Investors):

https://oakharvestfg.com/investor-mindset/

Interesting Reading:

https://www.foxnews.com/politics/bidens-pick-comptroller-currency-pro-communism-remarks

https://www.npr.org/2021/10/01/1042209223/why-covid-is-affecting-chinas-power-rations

This content contains general information and express the views of Oak Harvest Investment Services. All data, articles, and information cited are believed to be reliable at the time of creation; however, Oak Harvest does not warrant any information contained herein to be correct, complete, accurate or timely.

Oak Harvest provides links to content produced by other websites that OHFG does not control, and Oak Harvest does not necessarily approve or endorse such content and does not guarantee its accuracy. Nothing in this content constitutes personalized investment advice. Any charts, indicators, or graphs included or referenced in this content have limitations, and no such material is able, in and of itself, to provide a buy or sell recommendation for any security. Strategies and ideas discussed may not be right for you, and views and opinions expressed may change without notice. Strategies and ideas discussed will not apply to all client accounts or portfolios.

Nothing in this content constitutes a recommendation, or an offer or solicitation to buy or sell securities. Oak Harvest makes no assurance as to the accuracy of any forecast or projection made. Not all past forecasts or projections were, nor future forecasts and projections may be, as accurate as any forecasts discussed. Indexes like the S&P 500 are not available for direct investment and your results may differ. Past performance is not indicative of future results. Investing involves the risk of loss.