06.29.2020 – Market Update

By Chris Perras.

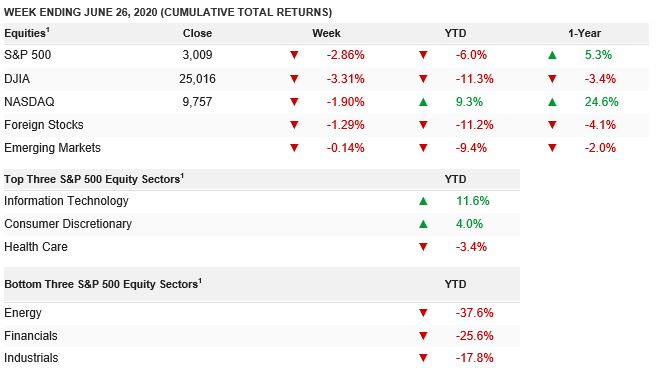

The S&P500 cash index closed the week at 3010, down about -2.9% on the week with all that coming on Friday, which was both option expiration and quarterly index rebalancing. Banks and energy were the biggest drags with the yield curve flattening. Short term traders sold cyclical stock. Equity markets slumped last week on increasing evidence that a second wave of COVID-19 is breaking out across several southern U.S. states. This should not be new news to those following our work. The virus data has been increasing since late May and early June following an increase in Memorial weekend beach and bar gatherings and protest driven groupings up to and through the George Floyd funeral on June 9th.

The domestic economic data flow continued to point to a rapid recovery, with core consumer spending rebounding solidly in May, and durable orders surging 15.8%. Core orders were up for the first time since the start of the year. The Citi economic surprise index reached an all-time high of +170 after reaching an all-time low of -125 in mid-April.

Data overseas continued its impressive rebound as well. China releases its official June manufacturing PMI data tomorrow and it is likely to hold above the 50-mark, signaling expansion. Moreover, the manufacturing PMI will be out on Wednesday and should also point to an expansion in the month.

The network news, almost always late to the true trend, is ignoring the virus data behind the scenes. The states seeing sustained rises in cases are not seeing a proportionate rise in healthcare utilization/hospitalization rate.

Here are several leading headlines from data as provided by FundStrat:

POINT #1: Daily cases surge >45,000 over weekend but ease to 38,231 on Sunday…

POINT #2: Overall Hospitalization and Death trends in USA are improving…

POINT #3: The biggest breakout of new cases is concentrated in 4 states (FLA,CAL,ARIZ,TEX). Following NYC path, the peak is not months away but is only 7-14 days away.

Weekly market updates contain general information and expresses views of Oak Harvest Investment Services. Data, Articles, and information cited are believed to be reliable at the time of creation, but is not guaranteed. Content should not be regarded as personalized investment advice. Views and opinions expressed may change without notice and do not constitute a recommendation, or an offer or solicitation to buy or sell securities. In addition, Oak Harvest makes no assurance as to the accuracy of any forecast made. Past performance is not indicative of future results. Investing involves the risk of loss