Significant ATHs; Depressed Press…

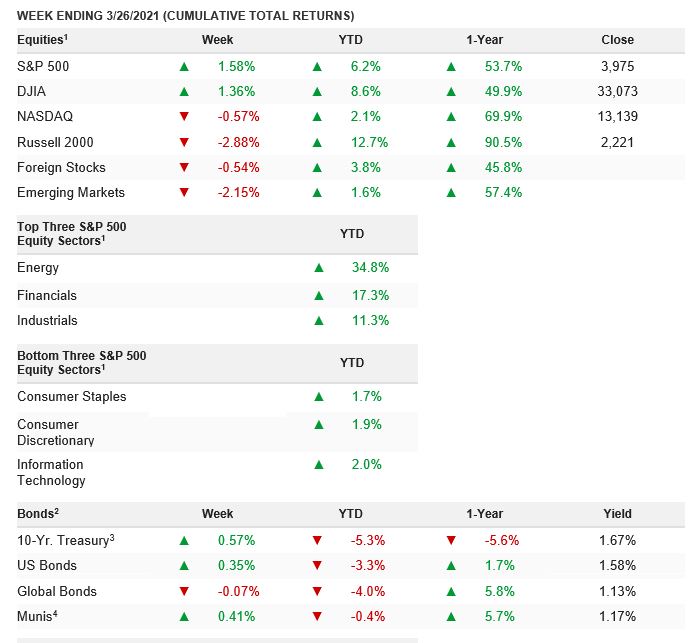

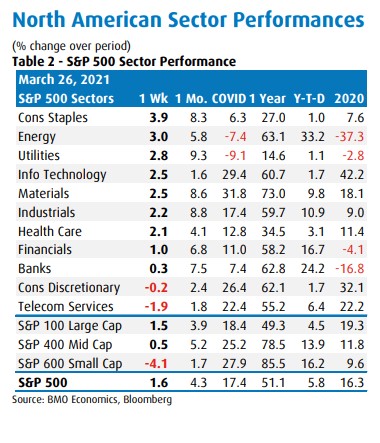

Market Update: Significant. Overall equity markets rose last week, much to the dismay of the financial press amongst a further collapse in both spot market and future month volatility. The S&P 500 rose 1.6%, with more defensive and rate-sensitive leadership, utilities and consumer staples leading the pack as interest rate momentum peaked and longer-term rates have eased. Telecom and consumer discretionary stocks lagged, while banks bounced back from some early losses after the Fed said it will lift dividend and buyback restrictions on those that have sufficient capital.

Real-time economic data — while stronger year over year, due to easy comparables — continues to miss economic forecasts: the Citi Economic Surprise Index retreated from an all-time high of 275 last August 2020, to an elevated 85 late February 2021, to an anemic 24 now.

Last week’s data, while weather affected, was very downbeat, with personal income and spending, new and existing home sales, and housing starts all down in February. Yes, the month was plagued by a combination of nasty weather here in Texas and the Midwest, and fading stimulus flows ahead of the next round of money from Washington, D.C.

Market’s historic rally

Last week marked the anniversary of the pandemic’s equity market bottom — and the rally from those lows has been historic. The significant peak-to-trough 34% plunge in the S&P 500 was not historic in scope, but in speed. The monetary, fiscal and healthcare response by government officials were the reason for the speed with which the market came back off those lows.

After the tech bubble in 2000, it took the S&P 500 more than seven years to recover its losses. After the financial crisis, it took the index more than five years to regain flat. Even the brief 1987 crash took almost two years to make it back to breakeven. This time, the index was pushing through pre-shock levels in just six months. Monetary policy was extraordinarily quick and aggressive; fiscal stimulus was historically aggressive — and the hardest hit areas of the economy typically do not trade in an equity index. Most of the large-caps — particularly technology, early on — benefited as many secular trends were accelerated.

Significant consumer savings

Good things come to those who wait, save and invest. With the ongoing stimulus plans and limited spending options due to Covid shutdowns, today’s consumer savings rate stands at almost 20%! Consumers simply have not had their normal opportunities for consumption. Travel and leisure activity plummeted in 2020 and is only now starting to accelerate. Significant: At a more normal savings rate of 6.0% in the USA, there would be $1.3 trillion of savings — not the current $4.4 trillion.

This means that today consumers have $3.1 trillion more cash in their checking accounts than they usually do. And even more cash is on the way. Following the injection from the latest stimulus checks, the amount of surplus savings is likely to climb to $4.0–5.0 trillion. While the economy is currently slowing as it normally does during mid-year, expect this capital to reaccelerate the economy come late-Q3 and Q4 2021 through Q1 2022.

Resources

Last Fridays Podcast: “Digital Widgets: Bitcoin, NFTs and the Metaverse”

Interesting articles:

- A Brave New Digital World

- How Salesforce became Silicon Valley’s best late-stage tech investor

- Chafing At Xinjiang Rebuke, China Ready To Burn Off Some Fingers

=

Weekly market updates contain general information and express the views of Oak Harvest Investment Services. Oak Harvest believes that all data, articles, and information cited are reliable at the time of creation. However, Oak Harvest does not warrant any information contained herein to be correct, complete, accurate or timely.

Oak Harvest provides links to content produced by other websites that OHFG does not control. Therefore, Oak Harvest does not necessarily approve or endorse such content and does not guarantee its accuracy.

Nothing in this content constitutes personalized investment advice. Additionally, all charts, indicators, or graphs included or referenced in this content have limitations. Therefore, no such material is able, in and of itself, to provide a buy or sell recommendation for any security. Also, strategies and ideas discussed may not be right for you. And views and opinions expressed may change without notice.

Nothing in this content constitutes a recommendation, or an offer or solicitation to buy or sell securities. Also, Oak Harvest makes no assurance as to the accuracy of any forecast or projection made. Not all past forecasts or projections were, nor future forecasts and projections may be, as accurate as those discussed.

Indexes like the S&P 500 are not available for direct investment and your results may differ. Also, past performance is not indicative of future results. Above all, investing involves the risk of loss.